Gas in 🇨🇦 $4.55 USD/gal

Gas in 🇺🇸 $3.25 USD/gal

29% cheaper

I can drive across an empty bridge thanks to the elbows up crowd and save $20/tank (even after toll).

@torontoarchive@Satoshi_Stackz@Wealthsimple I had the same page showing the same thing for months. Then I tried opening a credit card account and I got the car within 4 days. Have you tried actually opening a credit card account?

@PantexCap@100xCompounding@KarstResearch I’m pretty sure he explained how you are wrong already. His explanation was clear and concise. I will repeat it: “hahahaha ok bro”

I mean - I’m now being a jerk about it, but like tell me why I’m wrong?

The arguments are lazy and not accurate. I’m wrong about stuff all the time, and I do surface level analysis sometimes and am totally wrong - I love when people correct me cause then I learn. I probably should have been nicer to start, I apologize for that, but just frustrated at the narrative. And I asked to expand and got nothing so I stick to my view until proven otherwise

@Satoshi_Stackz@Wealthsimple Been a loyal client for 6+ years, and im still on waitlist, they only prioritize wealthy or new clients. I guess you fit either one. But congrats to you

@SummerSnowUSA That’s a cup-half-empty mentality. Unless you’re retiring in the next couple years, which then I would understand, a 50% drop for a company you believe is very undervalued is a blessing, regardless if it’s 28% or 100% of your book. It’s just an opportunity to buy more

@SummerSnowUSA@SFarringtonBKC@rogercfr So, again, this is something we should be hoping for; not worrying about.

I would not be worried if the flat screen TV I’ve been eyeballing for the past 3 months drops 50% in price over the next couple months.

I already have a very sizable position and, as we saw during COVID, once an overvalued market starts crashing all correlations go to 1. Selling begets selling. Even companies with improving fundamentals like Abacus can go through 50%+ downturns.

The containership company $DAC dropped 80-90% peak to trough in Q1 2020. Even though the fundamentals improved dramatically. And then it 21x bagged.

And I'm not normally one to time the market, but this is one of the rare exceptions to that rule. Between tech bubble-esque euphoria and consolidation at the top, the passive investing bubble, rumors of issues with private credit, and the very very very real catalyst of Iran, the danger of a severe correction is extremely heightened IMO.

@SummerSnowUSA@SFarringtonBKC@rogercfr Why would that situation worry you? Unless you are returning in a year or two, this scenario is what you should be hoping for

Not saying you're wrong, but blackberry stock price nuked from 2008 to 2011 despite great earnings during that period.

The market forecast period was initially pricing blackberry like it had a network effect / strong moat, in 2011, it was priced as a declining stock (which it was)

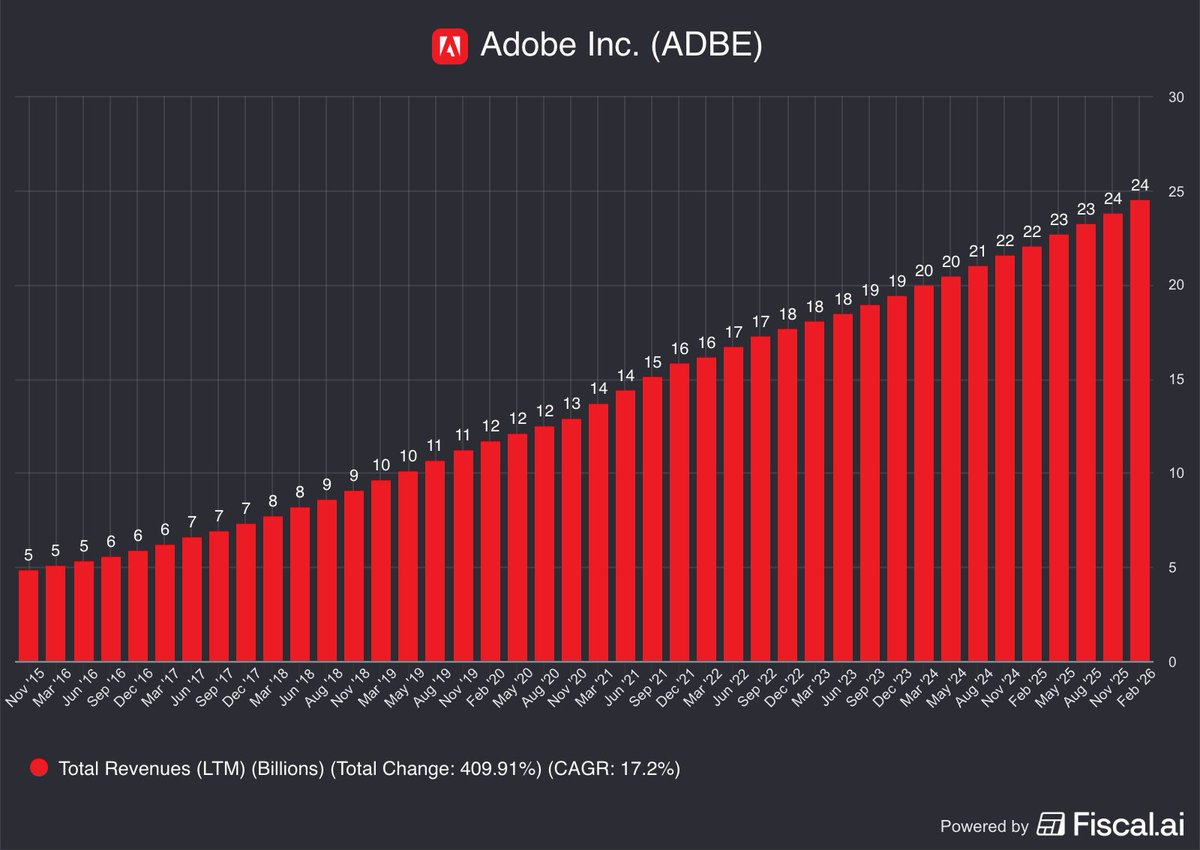

The market dumped $ADBE 6% for beating on revenue, beating on EPS, and reaffirming guidance.

Let me get this straight:

10.8x forward earnings. 12% FCF yield. AI ARR tripling. $22B in remaining performance obligations.

Sell it because the CEO is retiring after 18 years?

I'll take the other side of that trade all day.

The company can continue to grow, thats fine. But even after the massive drawdown in share price, the company is barely trading at fair value today.

I use a GARP approach to valuation to shed some light on how I come to this conclusion. Basically, they have a PEG greater than 1.0 still, making this not super attractive to me. Especially when I have questions about the durability of their future cash flows, which then requires a larger discount on DCF calculations.