Sabitlenmiş Tweet

This is an important one.

What the past can teach us about today, and why this is important to understand for the AI buildout.

open.substack.com/pub/notesonthe…

English

Notes on the Noise

7K posts

@NotesontheNoise

Markets, life and other things I pretend to understand.

Inside the Rack: 1️⃣ High-Bandwidth Memory (HBM): GPUs need fuel. Micron $MU is gaining share with a more power-efficient design. 2️⃣ Liquid Cooling: 1000W+ GPUs make this a necessity, not an option. Vertiv $VRT is a leader here with deep $NVDA ties

$MU ABSOLUTELY CRUSHED THEIR EARNINGS • Revenue $23.9B vs Est. $19.5B • EPS $12.20 vs Est. $8.73 • Net Income $14.0B vs Est. $10.5B • Gross Margin 74% vs Est. 69% Q3 Guide • Revenue $33.5B vs Est. $23.3B • EPS $19.15 vs Est. $10.77 • Gross Margin 81% vs Est. 71%

Inside the Rack: 1️⃣ High-Bandwidth Memory (HBM): GPUs need fuel. Micron $MU is gaining share with a more power-efficient design. 2️⃣ Liquid Cooling: 1000W+ GPUs make this a necessity, not an option. Vertiv $VRT is a leader here with deep $NVDA ties

The #crypto bull market's here. @coinbase is in the $SPY It's NOT just an exchange anymore, and it might be one of the most compelling plays out there. Time for a thread🧵👇 $COIN $BTC #ETH

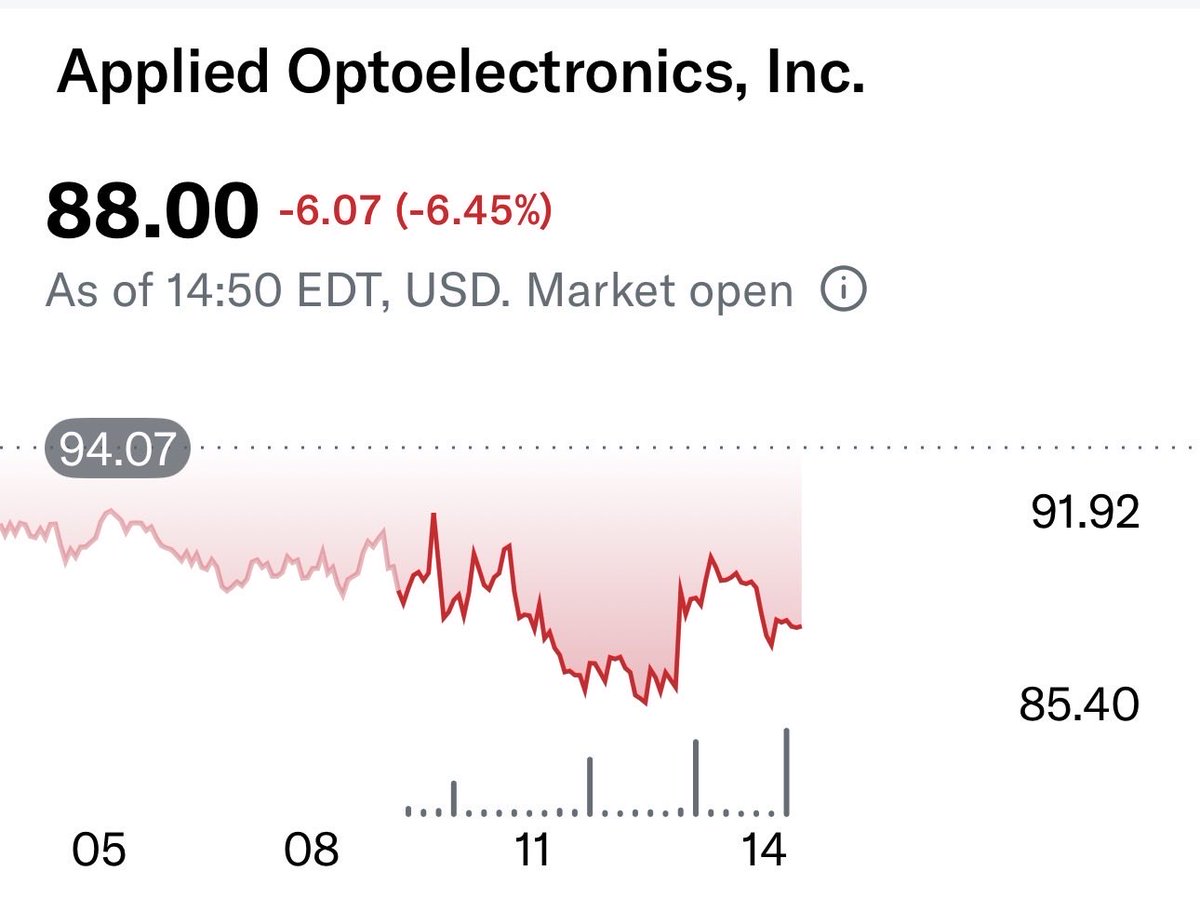

$AAOI didn’t drop because the story broke it dropped because too many things hit at once at the top. After a +200% run in the past 6m, you had the ATM expansion, insider selling, firmware uncertainty and still no profitability until 2027. That’s enough to shake weak hands. But none of that changes the core: AI optics demand is real, hyperscaler orders are real, and capacity is the bottleneck. This isn’t a broken thesis. It’s a reset after excess + execution checkpoint.