Sabitlenmiş Tweet

🧵Proof that Peter Lynch was (and possibly still is in his private investing these days) the greatest investor ever -

images.aqr.com/-/media/AQR/Do…

People seem to have forgotten about Lynch in comparison to Buffett.

/1

English

OutspokenGeek

1.6K posts

@OutspokenGeek

Just an outspoken geek, with a side interest in finance, investing and semiconductors. Not advice.

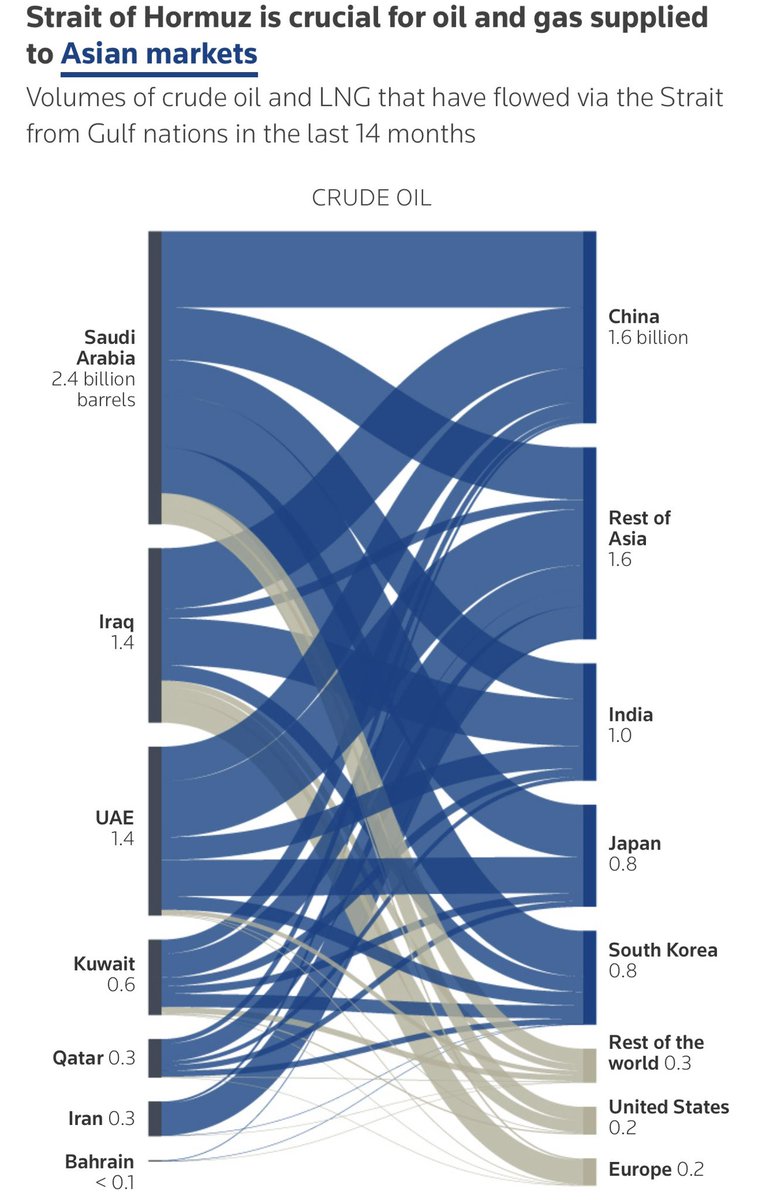

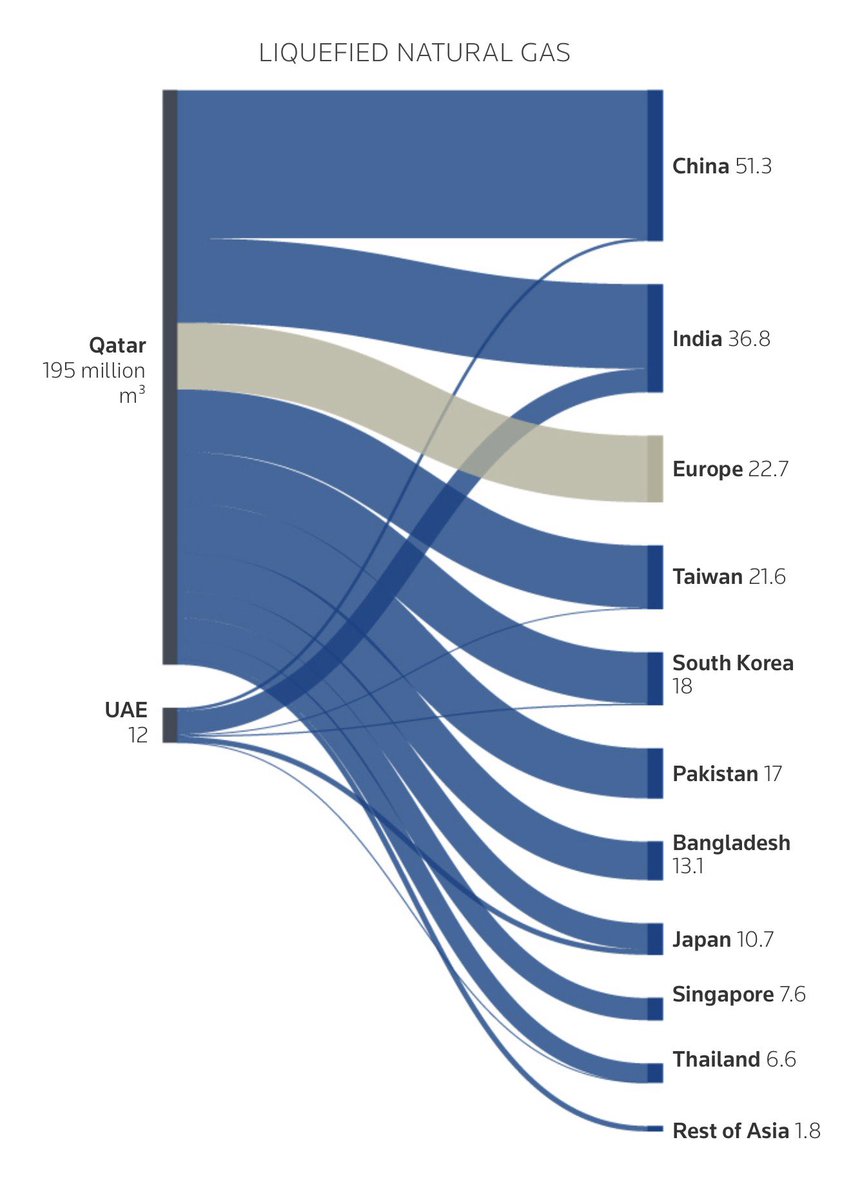

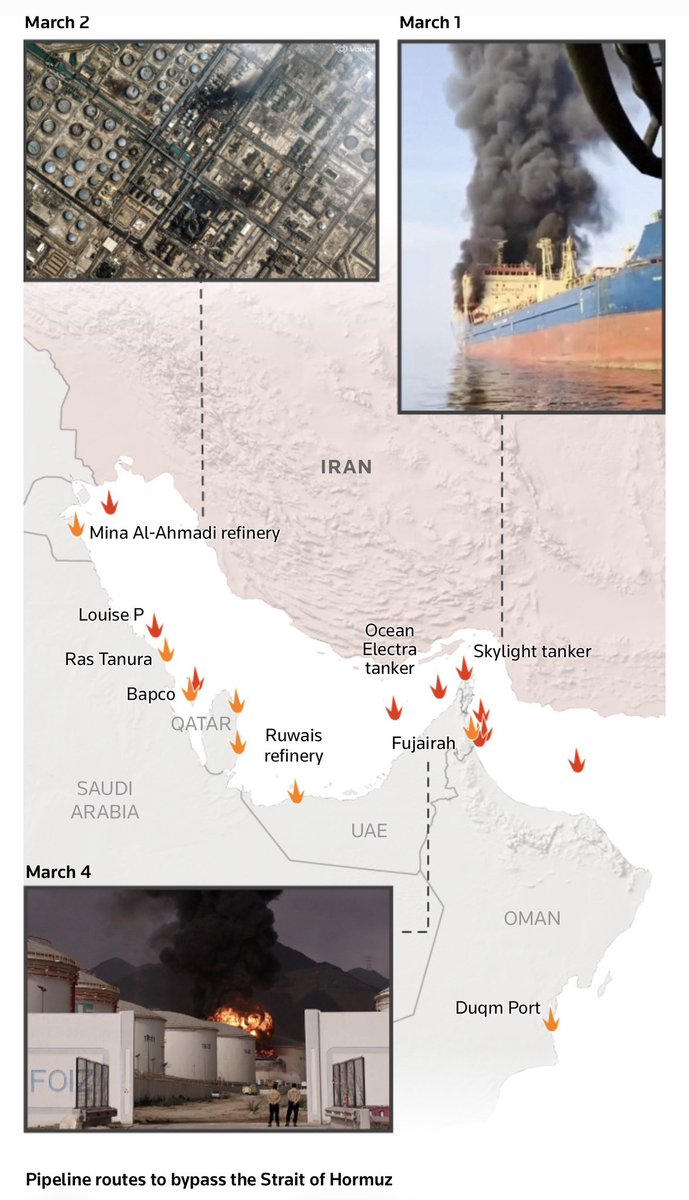

Iran’s attack on Qatar has damaged facilities that produce about 17% of its liquefied natural gas export capacity and repairs will take three to five years, QatarEnergy CEO said according to a Reuters report bloomberg.com/news/articles/…

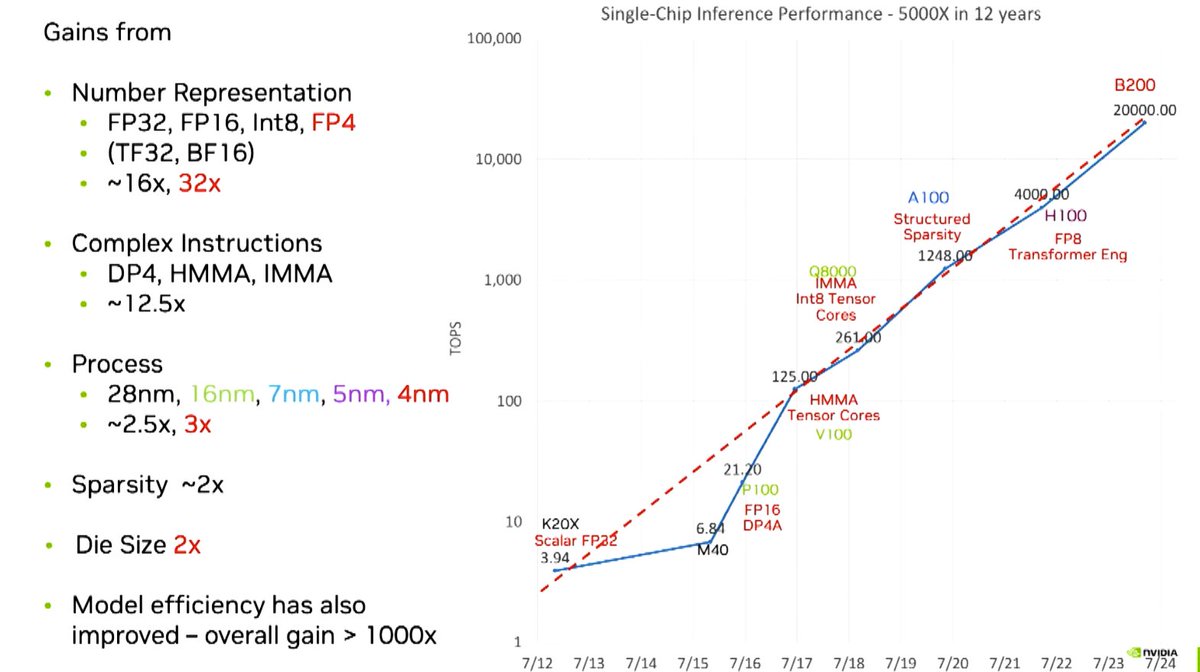

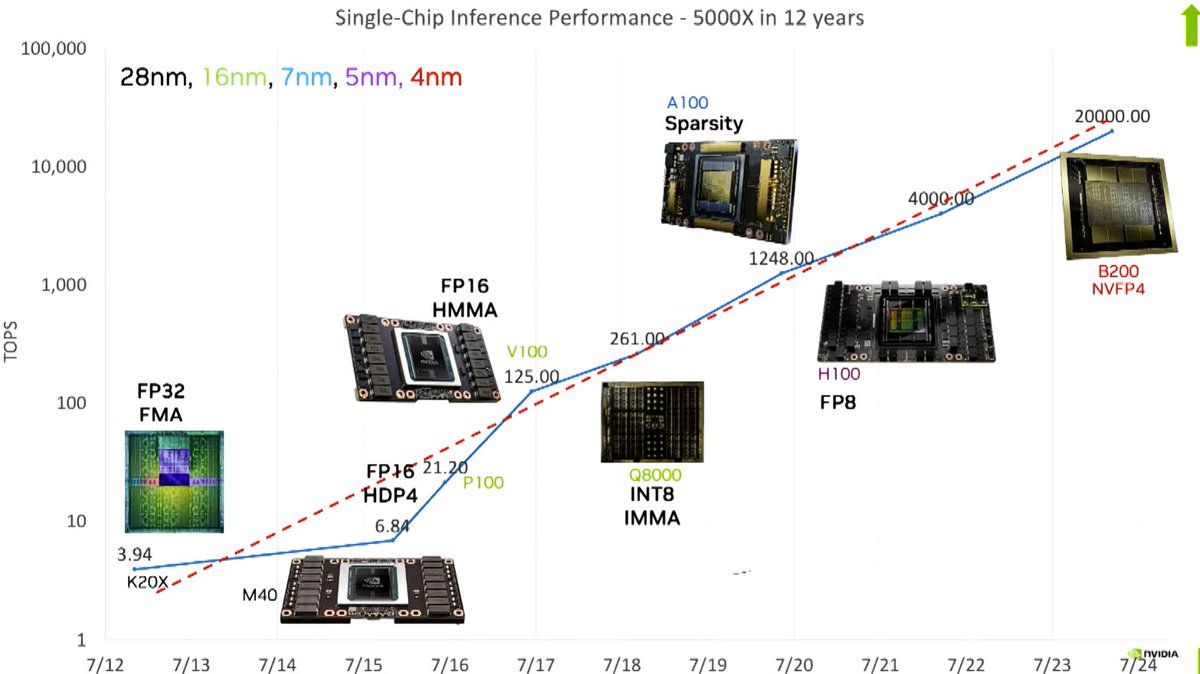

"Of the 1000x perf improvement in ML ops in the past 10 years only about 2.5x came from process technology [Moore's Law]" (Paraphrasing) — Bill Dally youtube.com/watch?v=kLiwvn… Let's see, the $NVDA stock has only gone up a few hundred times in the past 10 years. Seems fair?

@OnlyCFO I learned to think of history as a guiding principle; it works wonderfully on a macro level and abysmally at a micro level.

I can't quite bring myself to sell everything as I still want to see what happens. Who knows maybe Lip Bu Tan comes back as CEO? I mean one can dream! But don't forget this is the same board that let things get this bad. I don't have much confidence in them at this point. /2