Mack

63 posts

A few AI supply chain names still seem mispriced to me:

- Pillar Corp (6490)

- Kokusai Electric (6525)

- Landmark (3081)

- $KLIC

TLDR notes on all those:

-> Pillar Corp (6490) at ¥10,070

- monopoly in semi cleaning tool (fluororesin fittings)

- sell to likes of $AMAT / $LRCX, not chipmakers. So they don't appear in $TSM / Samsung supplier rosters that most investors/institutions use rn.

- most semi screens index on volumetric SAM (wafer starts). But it should be on intensity/wafer that HBM TSV formation + CoWoS wafer prep create. And intensity is where Pillar's fluororesin fittings benefit.

- Earnings last week confirms H2 ramp + inclusion in TOPIX 500 / MSCI Japan SmallCap

-> Kokusai Electric (6525) at ¥6,590

- deposition/treatment equipment for frontend chip manufacturing

- batch ALD share "reached a record high of over 70%" per Gartner

- recent weakness due to Chinese DRAM customer pull ins reversing, while NAND generation upgrades and DRAM HBM4 lines are accelerating

- SK Hynix M15X HBM4 ramps H2 2026 & Samsung P4 line in Q4. Both lean on Kokusai batch ALD for high-k + barrier layers.

-> LandMark Opto (3081) at TWD 2,655

- specialty InP/GaAs MOCVD epi-wafer foundry

- investors who know the name see it as a CW laser only / PD-only play, missing the EML pull through that comes from the structural $NVDA lockup.

- Landmark also competes with IntelliEPI for the same merchant slot. But Consensus tends to pick IntelliEPI for its US defence/CHIPS Act tailwind.

- 800G+ modules set to scale, so meaningful share of new capacity goes through merchant InP epi. Would mean LandMark revenue could at least 2x - imo mgmt are sandbagging which we could see in shareholder meeting at end of May.

-> $KLIC at $102

- been a chronic disappointer over the past ~3 yrs due to wirebonder cyclicality

- dominant TCB narrative belongs to $BESI (hybrid bonding) + ASMPT (HBM3E TCB).

- But the JEDEC 775μm relaxation extends TCB into HBM4/HBM5 - which is $KLIC's field.

- ASMPT + $KLIC are trying to delay hybrid bonder adoption w/ their fluxless TCB tools.

- That's actually a structural tailwind being read as a delay risk.

Just qualitative analysis for now. Would need to do deeper research on Pillar + Kokusai especially e.g. financials, TAM etc.

Note: no positions.

English

@hanifbali Det är intressant eftersom människor med högre intelligens tenderar att luta mer åt vänster än höger. Hur ska högern utjämna detta?

Svenska

Korrelationen mellan IQ och inkomst.

Observera att graferna börjar runt IQ 90 (4 stanine) går upp till ca IQ 120 (7,5 stanine).

Avkastningen på IQ blir högre ju mer IQ man har.

Hur ämnar vänstern utjämna detta?

Svenska

New all-time high, and officially an 8-bagger for me.

$NBIS changed my life.

English

I trimmed $NBIS yesterday from 40% to 25%.

Before you stone me to death:

I share because I want to be as transparent as possible.

I'm still super bullish on the company.

I've been going from 90% $NBIS port to now 25% and I do not regret it even a little bit.

I did it to raise cash, for 2 reasons:

* Taxes

* Market in my opinion is overheated,I said in my opinion because I could always be wrong.

I owe it to my family to protect my money.

I may return to a higher allocation in the future(perhaps in a higher price, or lower, whatever price the market will give me at the time).

I see people are getting stoned to death here for trimming positions, but always remember that in the end, you are the one responsible for your own money.

I don't seek validation, just sharing here transparently.

PS: I'm still around 70-80% invested in the market.

English

@Oblomov936994 Vad bygger dagens värdering på Oblomov?

Svenska

@zephyr_z9 Are we moving to Hybrid Bonding faster than expected, or is TCB here to stay because of yield problems?

English

Grok did a good job, but it's missing a very important point that will determine the duration of these bottlenecks

Grok@grok

The huge difference: HBM, advanced packaging, high-end PCBs & optics are **tech-complexity bottlenecks** — limited by cutting-edge processes, yields, and a handful of players (TSMC, SK Hynix, etc.) that can’t ramp fast enough for exploding AI demand. MLCCs, power semis & analog are **volume/allocation crunches** on mature nodes — strained by broad demand across EVs, industrial, consumer + AI, plus raw material issues, but easier to expand with existing fabs. One is “can’t build it yet,” the other is “everyone’s fighting for share.”

English

@aleabitoreddit I find it odd that you exclude Sweden from “The West”. Other than that I’m with you.

English

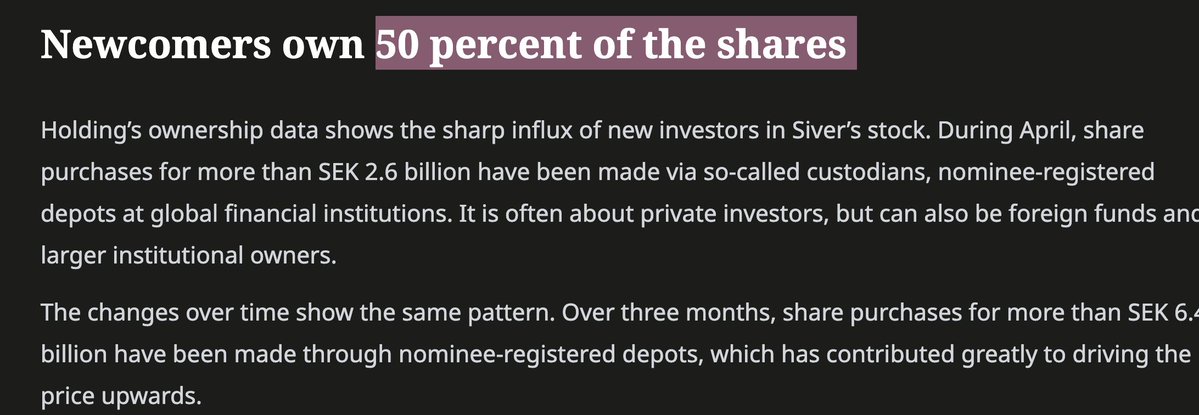

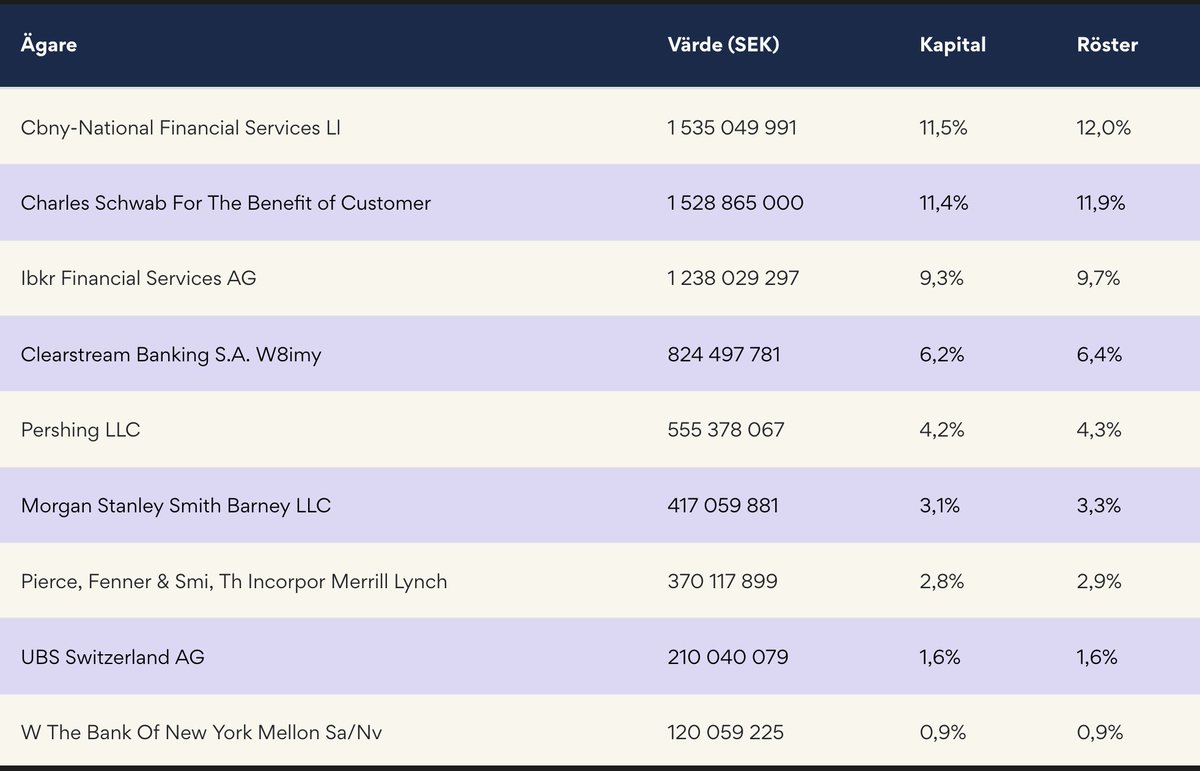

The US/West now controls majority of the shares of $SIVE.

With Goldman Sachs/JP Morgan/Morgan Stanley and other US institutions entering.

US/West 46.8%:

- Fidelity: 11.5% (retail)

- Charles Schawb: 11.4% (retail)

- $IBKR: 9.3% (primarily retail)

- BNY Mellon: 4.2% (retail)

- Morgan Stanley Smith Barney: 3.1% (Retail/Wealth management)

-Bank of America: 2.8% (retail/Wealth management)

- BNY Mellon: .9% (institutional)

- Morgan Stanley Client Assets: .7% (institutional)

- Bank of New York Mellon: .5% (institution)

- JP Morgan: .5% (institutional)

- J.P. Morgan Securities Plc: .4% (institutional)

- Citibank New York: .3% (institutional)

- JP Morgan SE: .2% (institutional)

- Morgan Stanley: .2% (institutional)

- JP Morgan Securities: .2% (institutional)

- BoFA Securities: .2% (institutional)

- Goldman Sachs: .2% (institutional)

- Goldman Sachs International: .1% (institutional)

- Cbny-Rja-Client Asset - .1% (retail/wealth)

Large % now owned US retail shareholders (eg. $IBKR on behalf of clients, probably majority retail some institutions).

The new but smaller JP Morgan Goldman Sachs, and Citibank % positions are likely hedge funds or other institutions trying to build positions.

Europe & Switzerland: 11.3%

- Clearstream: 6.2%

- UBS Switzerland: 1.6%

- Six SIS: 0.8%

- Euroclear Bank: 0.8%

- Saxo Bank: 0.6%

- BNP Paribas: 0.6%

- Caceis Bank / Intesa San Paolo: 0.2% each

- KBC / LGT / Julius Baer: 0.1% each

Swedish ~8.49%:

Försäkringsaktiebolaget Avanza Pension - 4.76%

Nordnet Pensionsförsäkring - 2.73%

Skandinaviska Enskilda - .2%

SEB Life International - .1%

Nordea Bank Abp - 0.7%

Canada/UK/Middle East ~.6%:

First Intl Bank of Israel - .3%

Royal Bank of Canada - .1%

Royal Bank of Canada - .1%

HSBC - .1%

A special thank you to the Swedish Media doing the work of US institutions:

The West now has ~58.7% ownership. Swedish is now down to 8.49% due to local media.

I wonder if they realized what they've done now scaring off local investors now that it's changed hands to US institutions/investors?

The West have now acquired majority of the float before the CPO supercycle.

You can also start to see US institutions like JP Morgan or Goldman Sachs building start positions (on behalf of institutional investors), probably off of US retail taking profits. This is likely after $SIVE reached a certain MC threshold for fund mandates.

But a large % of it is still owned by US retail on places like $IBKR and Fidelity. (this is what I call frontrunning the institutions)

TLDR:

$SIVE went from majority:

-> Swedish retail ownership

-> US retail ownership

-> gradual US Institution ownership as US retail takes profit or sells (if they figure out a way to scare off US retail like the Swedish media did).

English

Broadcom confirms it: Hybrid bonding has severe yield issues.

AI needs volume today. Since Hybrid can't scale yet, the industry relies on proven TCB to stack HBM.

This is why $KLIC is accelerating. Hybrid is the future, TCB is building the present.

#ai #AdvancedPackaging

Jukan@jukan05

The Critical Weakness of AI Computing Power… Broadcom Identifies "3 Major Bottlenecks," Supply Shortages Could Persist Until 2027 • Broadcom has identified the key bottlenecks in the current AI supply chain as: ▲lasers, ▲advanced process wafers (particularly TSMC), and ▲PCBs. Notably, lead times for the small-form-factor PCBs used inside optical transceivers have extended from approximately 6 weeks to 6 months, with relief not expected until 2027. • These small-form-factor PCBs require high-difficulty mSAP processes due to the demands of high-frequency signal processing and ultra-compact design. Because their production processes partially overlap with IC substrates for HBM, the surge in global AI server demand is paradoxically eroding PCB production capacity. Additionally, supplier qualification takes over 6 months, leading hyperscalers to lock in existing supply chains through long-term contracts. • Laser components have also been flagged as a critical bottleneck in the CPO era. Lasers for AI data centers require high-power, low-noise characteristics, and the yield rate passing stringent reliability testing remains below 30%. The number of vendors with InP (indium phosphide)-based production capabilities is particularly limited, and in CPO architectures, laser demand increases not linearly but multiplicatively, further intensifying supply pressure. • On the wafer front, TSMC's advanced process nodes are projected to hit a bottleneck by 2026. However, the real issue lies in back-end advanced packaging. The CPO era requires high-difficulty hybrid bonding technology to integrate optical and silicon dies, with throughput and yield severely constrained in the early stages. • Furthermore, TSMC must allocate the same production lines across NVIDIA, Apple, AMD, and Qualcomm, as well as Google, Meta, and OpenAI — effectively operating production capacity under a "rationing" regime. New capacity additions also face 12–18 month equipment lead times, making near-term relief unlikely. • Meanwhile, expansion at suppliers of packaging substrates, underfill, testing, optical communications, and probe cards is progressing even more slowly, causing bottlenecks to proliferate across the entire supply chain. As a result, supply chain bottlenecks and price inflation are likely to persist structurally, with the segments experiencing bottlenecks emerging as the critical nodes wielding pricing power.

English

$KLIC +19% in pre-market after stellar earnings! +33% since I shared it two weeks ago!

Personally, I wouldn't fade my semiconductor equipment & materials stock picks.

Full list in the article below!

nic.aqs@nicaqs

$KLIC and 2 more tickers have been added to my list of early, high-timeframe bullish semiconductor manufacturing names. Read the full article here: ko-fi.com/post/A-Refined… ☕️

English

@zcelestialbaby @aleabitoreddit Sure but compare it to facebook and how much ad revenue they generate per user. There is room for growth there imo.

English

@aleabitoreddit Aint it buncha bots on there?

Also, what is better, WSB subreddit or X?

English

@HyperTechInvest Just want to say ty! Your posts about $MU made me research and buy it about a months ago. I’ve made a pretty decent profit since. 🙏🫡

English

Absolutely impossible. I was clearly told a couple of months ago that DRAM had topped and $MU was going to $100

Jukan@jukan05

TrendForce on April memory contract prices: - April DRAM prices rose 57% compared to 1Q26. - Compared to 1Q26, PC DRAM rose 40%, server DRAM rose 48%, mobile DRAM rose 80%, and consumer DRAM rose 60%. - April NAND prices rose 65–70% compared to 1Q26. - eMMC/UFS, mainly used in mobile devices and SSDs, rose around 75–80%.

English

@aleabitoreddit You should consider a thesis post on $LPK before it hits the market cap threshold where institutions typically start buying. It would give your followers a massive head start.

English

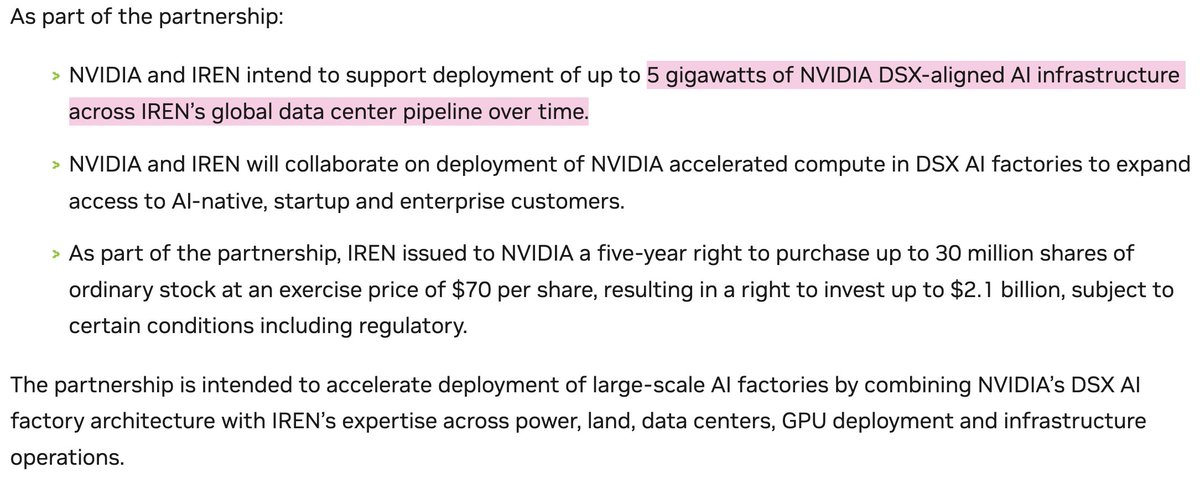

@aganstwallst @mi20483980476 @aleabitoreddit This ”huge vote of confidence” basically means that NVIDIA believes Iren will be able to pay for the hardware one way or another.

English

Have you guys ever done any acquisitions for the company? Or back when you were in management, did you ever make a call like this?

Just the existence of an option like this already shows how creative and forward-thinking $NVDA really is. The fact that they actually accepted it is, in and of itself, a huge vote of confidence

NVIDIA isn’t stupid, they’re not about to risk $2.1 billion. But at the end of the day, they’re still willing to take the stock option as well

English

I still am bearish on $IREN.

Algorithms/retail probably read $NVDA + $IREN partnership and bought it up.

However, if you look at the realtity, it's just looks like brand agreement giving $NVDA risk-free convertible notes.

So $IREN can continue selling their $6,000,000,000 ATM into retail investors.

It's the equivalent of a startup using AWS and saying they have an Amazon partnership so give them $6B.

This wasn't Nvidia directly funding $IREN yet, just a risk free option to.

There's a "5 GW deployment" but I'd rather not be the one buying into the dilution to fund it.

Cooker.hl | Kms.eth | 版本之子 | Cooker@CookerFlips

@aleabitoreddit $IREN announcement 🤯

English

English

@FransBakker9812 @HyperTechInvest I’m done getting into petty debates with $NBIS bulls. They don’t learn….

Time will let which one of the 2 companies will end up with higher GAAP earnings.

It’s obvious to me & you which one will come out on top, but $NBIS bulls will have to learn the hard way.

English

Let's discuss $IREN again

To all those who said, "How is it a moat if it can be bought so easily?"

> Nothing easy about spending over $600M on a single part of the software stack

To all those who said, "What’s easier to buy, the software or the infra?"

> You can absolutely buy both. Software is just as hard, if not harder. It is not for nothing that $NBIS is selling complex services to companies like Cloudflare, Shopify, Revolut, plus its large deals with $META and $MSFT. If access to power was the only important factor, why did these companies not go with $IREN first? Think about that

Power connections can absolutely be bought as well

I hope you all realize $IREN acquired contractual rights to acquire land parcels and secured electricity connection rights in Oklahoma for 1.6GW, for just $112M

In the case of $NBIS, they secured 800MW+ in Independence in a relatively short amount of time, and the cost of acquiring this power is minimal compared with the GPUs and the actual data center buildout

I'm not saying $IREN sites aren't extremely valuable. They are. But it's just funny how the narrative went from "software isn't important, customers bring their own" to "we spent over $600M on just one part of the software stack, but that's nothing compared to the value of power connections."

I feel this weak narrative is going to be stretched out until it no longer makes sense

The reality is that hyperscalers absolutely care about the ability these companies have to set up these GPU clusters from both a hardware and software perspective

Daniel Romero@HyperTechInvest

Can we now put to sleep the argument that software is not a moat for neoclouds? Once you need to spend $600M+ to cover just a fraction of the software stack, that thesis gets reduced to ashes $IREN is just starting its road to building a software stack, while a company like $NBIS is already at the top That gap should deserve a valuation premium

English

@MisterMCAP @aleabitoreddit That is not the reason why companies move to the US.

English

Like @aleabitoreddit keeps saying - Insane how articles like these STILL cause Swedish investors to press the sell button on $SIVE instantly. Oh well lets keep selling our diamonds to US investors for pennies🤡.

Then we cry about our unicorns moving to US, maybe because you sell the successful ones who stay anyways? $SIVEF

English

What we’ve been saying since all of this began:

The Swedes simply don't understand the hyperscaler supply chain

They haven't the slightest idea how incredibly well positioned $SIVE is

Or they’re just like we already said

They only want local things without the US getting involved

They certainly don't understand that they are looking at the most asymmetric company of the moment

Because it’s currently on the CPO (Co-Packaged Optics) ramp up

Which is one of the most innovative and important developments of recent years

It’s at a ridiculous market cap compared to "others" like $COHR or $LITE

Which have market caps 30–50 times larger

I won't even get into when we first started talking about $SIVE

When the difference was more than fivefold

And back then, they were trying to drag it down with FUD (fear, uncertainty, and doubt)

Nothing new

Serenity@aleabitoreddit

I'm still laughing how much Swedish hate their own frontier companies so much. That they write hit pieces every day on $SIVE. This one was entertaining: Local journalists show up to an empty $SIVE administrative building uninvited. Because they can't fathom the CEO is in Silicon Valley or design team is working on US Gov CHIPS act dev in the US. And because there weren't many cars parked outside + CFO wouldn't take questions about secretive hyperscaler deal financials. They wrote a random negative hit piece. By repeating "There are several who make lasers like these and Sivers are far from alone". Several like $LITE, $COHR, $60B+ companies. and reported earlier that "CPO is nothing special, it's been around for years." While GS projects CPO going from $1B -> $91B TAM over the next two years. Even put "Plans" in quotation marks because they didn't think Sivers is supplying lasers to $JBL 1.6T LRO. IMO, $SIVE ends up as a $10B+ company next year, especially if they follow what $LITE / $COHR did with downstream IP integration to capture more of CPO module BOM. Just don't think Swedish people understand hyperscaler supply chains, concept of forward growth, or the fact that employee count doesn't equate to revenue. Transfer of control from local Swedish -> West is always appreciated, as this was a majority owned local retail company before.

English

@aleabitoreddit Sivers has literally been the most net-bought stock on Avanza (largest swedish broker) lately. The trading volume is beating several large-cap companies. So not all hate, my guy.

English

I'm still laughing how much Swedish hate their own frontier companies so much.

That they write hit pieces every day on $SIVE.

This one was entertaining: Local journalists show up to an empty $SIVE administrative building uninvited.

Because they can't fathom the CEO is in Silicon Valley or design team is working on US Gov CHIPS act dev in the US. And because there weren't many cars parked outside + CFO wouldn't take questions about secretive hyperscaler deal financials.

They wrote a random negative hit piece.

By repeating "There are several who make lasers like these and Sivers are far from alone".

Several like $LITE, $COHR, $60B+ companies.

and reported earlier that "CPO is nothing special, it's been around for years."

While GS projects CPO going from $1B -> $91B TAM over the next two years.

Even put "Plans" in quotation marks because they didn't think Sivers is supplying lasers to $JBL 1.6T LRO.

IMO, $SIVE ends up as a $10B+ company next year, especially if they follow what $LITE / $COHR did with downstream IP integration to capture more of CPO module BOM.

Just don't think Swedish people understand hyperscaler supply chains, concept of forward growth, or the fact that employee count doesn't equate to revenue.

Transfer of control from local Swedish -> West is always appreciated, as this was a majority owned local retail company before.

English