Poly VPN@Poly_VPN

$5 Million Is on the Table. Here's How to Get Your Share.

Polymarket just announced $5 million in liquidity rewards for April 2026 — distributed across sports and esports markets including major European football leagues, CS:GO, DOTA 2, and League of Legends. Rewards are paid daily in USDC directly to maker addresses.

Reward farming on Polymarket isn't dead. It just moved to sports.

If you want to capture a meaningful slice of that $5M, you need to understand how the rewards formula actually works — and why infrastructure matters more than most people think. This is a practical guide to getting started as an automated liquidity provider on Polymarket.

What Is Liquidity Providing on Polymarket?

Polymarket runs on a Central Limit Order Book (CLOB). Every market has a YES and NO side, priced between $0.01 and $0.99, representing the implied probability of an outcome. For markets to function — for takers to buy and sell at fair prices — someone has to post resting orders on both sides of the book. That's you, the liquidity provider.

In return for taking on inventory risk and keeping markets tradeable, Polymarket pays liquidity rewards on top of any spread you collect. With $5M allocated just for April, the combination of spread income and rewards makes automated LP genuinely interesting again.

How the Rewards Formula Works

Before you write a single line of bot code, understand this: Polymarket's rewards formula is not passive. It's designed to force liquidity into the most useful part of the book.

Quadratic spread penalty. Rewards don't scale linearly with how much size you post. They collapse quickly the further your quotes sit from the Adjusted Midpoint. Posting tight quotes near the midpoint earns disproportionately more than posting wide. The formula rewards quotes where price discovery actually happens.

Adjusted Midpoint. This isn't simply (best bid + best ask) / 2. Polymarket filters out "dust" orders below a minimum incentive size before computing the midpoint. This prevents a classic attack: posting tiny orders at extreme prices to artificially pin the midpoint, then farming rewards around the fake center.

Time = risk exposure. Rewards accumulate the longer your orders sit in the book. But longer time in the book also means higher probability of getting filled. You're effectively selling gamma — the longer you stay, the more tail risk you're absorbing. There's no free lunch.

Single-sided penalty. You can post on just one side of the book in the neutral zone (roughly 0.10–0.90 probability), but you'll earn roughly a third of what two-sided quoting earns. At the extremes (near 0 or 1), both sides are required or your rewards drop to zero.

What You Need to Build

A Price Feed

Your bot needs a "fair value" — a theoretical probability for each market condition. Without this, you're quoting blind and informed takers will pick you off systematically.

For sports markets, this means connecting to a real-time odds feed or building your own implied probability model from line movements. The key insight: whatever data source Polymarket uses for resolution is your reference point, not your pricing input. You want to be ahead of that feed, not reacting to it.

For crypto UP/DOWN markets the same principle applies — Polymarket resolves against Chainlink, which is a lagged aggregation of faster feeds. Price off Binance directly. Treat Chainlink as the resolution reference only.

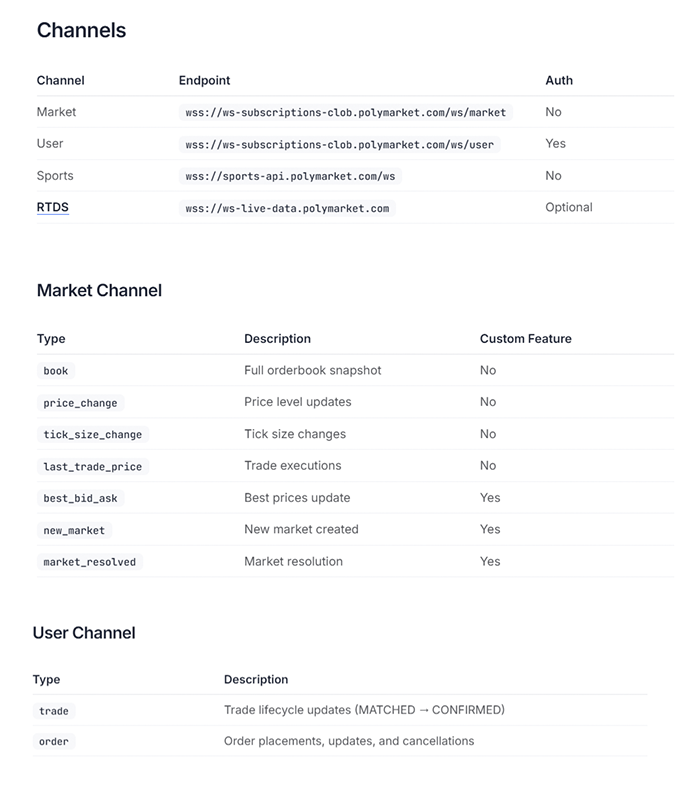

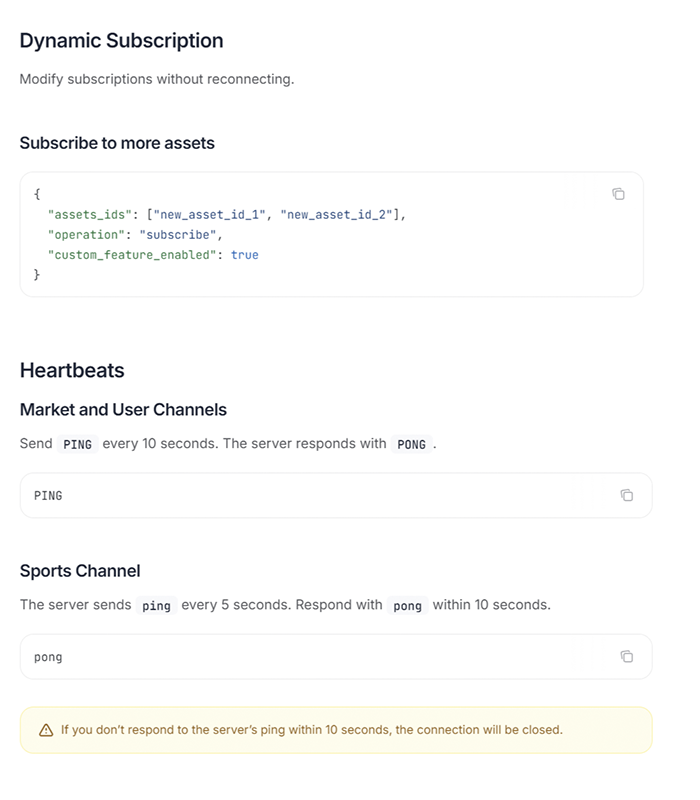

A WebSocket Connection

Polymarket's API provides real-time order book data over WebSocket. You need to subscribe to:

book — Level 2 order book snapshots and updates

price_change — order placements and cancellations

last_trade_price — fill events

best_bid_ask — top of book

order / trade events on your authenticated user channel — your own fills, placements, cancellations

By combining book snapshots with event streams, you can reconstruct the full order book state in memory at all times.

Order Management Logic

Your bot needs to handle:

Quote placement — post limit orders on both sides at your desired spread around fair value

Cancel/replace cycle — when your fair value updates, cancel stale quotes and repost at the new price. This needs to be fast. Stale quotes are free options for informed takers.

Inventory management — as you get filled on one side, your position accumulates. You need rules for when to hedge, pull quotes, or widen spreads to manage directional exposure.

Edge cases — ghost fills, WebSocket disconnections, and high-latency periods where your quotes go stale before you can cancel them

Note: if you're still running v1 SDK code, update immediately. CLOB v2 goes live April 22 — all existing order books will be wiped at cutover and the new order struct requires re-signing. Bot operators on legacy code will be offline from day one.

Risk Parameters

Before going live, set hard limits:

Maximum position size per market

Maximum total exposure across all markets

Minimum spread (below which you won't quote, regardless of rewards)

Circuit breakers for unusual market conditions

A Practical Starting Strategy for the $5M Pool

The $5M rewards are split across Pre-match and Live (in-play) phases. Live markets are faster and more competitive — prices move with game events in real time. Pre-match is slower and a better starting point if you're building your first bot.

The basic playbook for pre-match sports LP:

Connect to a real-time sports odds feed and derive implied probabilities

Post two-sided quotes tight enough to earn meaningful rewards, wide enough to survive normal line movement

Cancel and repost as your fair value updates when new information arrives (injuries, lineup changes, line movement on other platforms)

Collect rewards daily in USDC while collecting spread on fills

The edge comes from having a better pricing model than competing LPs and being faster to reprice when information changes.

Where Latency Decides Who Wins

For slow pre-match markets hours before a game, latency is mostly irrelevant. You're adjusting quotes over minutes, not milliseconds.

The moment you move into live in-play markets — or any market with active taker flow — latency becomes your most important infrastructure variable.

Polymarket's CLOB matches orders on price-time priority. Same price, first arrival wins. When a goal is scored and every market maker is racing to cancel stale quotes and repost at the new price, the traders who complete that cycle first set the new market. Everyone else gets picked off on their stale quote, or arrives too late to post at the new best price.

The CLOB is in London. Every cancel, every new order, every reprice makes a round trip to London. If your VPS is in Ireland or Amsterdam, you're adding unnecessary latency to every single one of those round trips. In a race measured in milliseconds, that compounds across hundreds of reprices per day into real money.

With $5M in rewards concentrated in April, competition among LPs is going to be fierce. The makers who capture the largest share won't just have better pricing models — they'll have faster infrastructure.

poly-vpn.xyz puts your infrastructure in London, same city as the CLOB. Better queue position on posts, faster cancels on stale quotes, less adverse selection from takers who are already there.

The Honest Picture

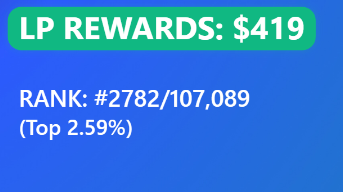

Reward farming on Polymarket went through a boom-and-bust cycle. Early LPs with 10,000 USDC were reportedly making 200–300 USDC per day at peak. That era ended as more sophisticated players entered and rewards-per-dollar compressed.

The $5M sports announcement changes the calculus again — but not back to the easy days. The rewards are real, but so is the competition. The makers who capture a meaningful share will be the ones with solid pricing models, fast cancel/replace infrastructure, and servers in the right city.

Liquidity rewards are best understood as a bonus on top of real trading edge, not a standalone money printer. But with $5M on the table in a single month, the bonus is worth taking seriously.

Further Reading

Polymarket liquidity rewards docs: docs.polymarket.com/market-makers/…

CLOB v2 migration guide: docs.polymarket.com/changelog