Sabitlenmiş Tweet

?

551 posts

?

@SaintMecatti

permanently short USD

United States Katılım Ağustos 2011

300 Takip Edilen270 Takipçiler

@gofallingknife Still in the money, just added decided to add on that dip to 4.74. Snagged some more shares sub $4 today.

Good shit though, you timed that well.

English

Changes to port today:

Sold $aaoi $229, $nuai $5

Bought $te $5.35, $now $87, $intu $375

Increased shares in $mu, $sndk, SK, $mrvl

English

? retweetledi

English

@pdicarlotrader When IREN rips 20% on a deal announcement this is gonna look really dumb.

English

Lots of questions on $IREN.

Still not a buy in our system.

Monthly BX shows buying pressure.

But 33FVB is still red.

That means the odds of rejection here are high.

English

Literally just a taste of what data center discourse during election season will mostly look like

Sean Fitzgerald (Actual Justice Warrior)@IamSean90

Best comment ever on data centers

English

@SaintMecatti 100% buying back $nuai later this week. But wanted to rotate to other stocks that fell pretty hard today.

English

Behind the meter power generation.

$SLNH is one of the most asymmetric AI power plays right now and almost nobody knows that they're well positioned...

The US power grid is breaking under the weight of AI data centers.

PJM, the grid operator covering 67 million people, already said publicly the grid is not fit for purpose.

Permits to connect new data centers are taking years.

Even hyperscalers with unlimited money can't get the power they need on the timeline they need it.

So the smart players are doing the obvious thing...

They're skipping the grid entirely.

Co-locate the data center directly with the power source.

Generate behind the meter.

No interconnect queue, no transmission bottleneck, no waiting in line behind everyone else.

They co-locate green data centers directly with wind, solar, and hydro plants.

They just signed a Siemens MOU for a 2MW pilot specifically to solve GPU power swings in a behind the meter environment.

They own the Briscoe Wind Farm now and just expanded the Blockware partnership to over 17MW.

This is not a story stock.

They have real revenue, real customers, real partnerships, and real infrastructure already producing.

We think Soluna is the highest beta way to play this... I added more and plan to hold until at least earnings... NFA!

Sun Liao@sunxliao

5 names I’m watching closely right now, all riding the same wave IMO... $PENG. Penguin Solutions is the AI factory builder. They take a billion dollars worth of $NVDA GPUs and turn them into a working cluster… they’ve already deployed over 85,000 GPUs for customers like Shell, Sandia, and one of Korea’s largest Blackwell clusters. Just got picked by Deepgram and Dell to architect their voice AI. $SLNH. Soluna is the behind the meter power play. The US grid is breaking under the weight of AI data centers and PJM already said it publicly. Soluna co-locates green data centers directly with wind, solar, and hydro… they just signed a Siemens MOU for a 2MW behind the meter pilot and own the Briscoe Wind Farm. $DGXX. Digi Power X just signed a 10 year deal with Cerebras worth up to $2.5B for a 40MW AI data center in Alabama. Cerebras IPOs on the Nasdaq this Thursday, which puts them in the spotlight as the public proxy. $WYFI. WhiteFiber spun out of $BTBT, IPO’d at $17 in August, and is now sitting near $27. Q3 revenue was up 65% YoY and they just signed an $865M, 10 year colocation deal with Nscale at their NC-1 campus. BTIG just initiated coverage. Same playbook as $CRWV at a fraction of the size. $OUST. Ouster is the lidar pure play and the robotics wave is the next leg of AI nobody is positioned for yet. Every humanoid robot, every autonomous truck, every smart warehouse needs eyes… I added to my SLNH position and plan to hold until earnings... NFA! Common thread on all five… AI infrastructure, real revenue, and the institutions haven’t really shown up yet.

English

@WatcherGuru I don’t who is worse @michaeljburry for this or @WatcherGuru for reporting it like anyone cares.

English

JUST IN: Big Short investor Michael Burry says stock market is "minutes" away from a "bloody" crash.

English

@BLUCBOOMER @SCHDaccumulator What if I told you that I have significantly outperformed the market over many years and also sleep easy?

English

My portfolio is 100% ETFs

It’s so nice not having to worry about individual stocks! 😌

English

@SaintMecatti They both start with the letter N so you may be right

English

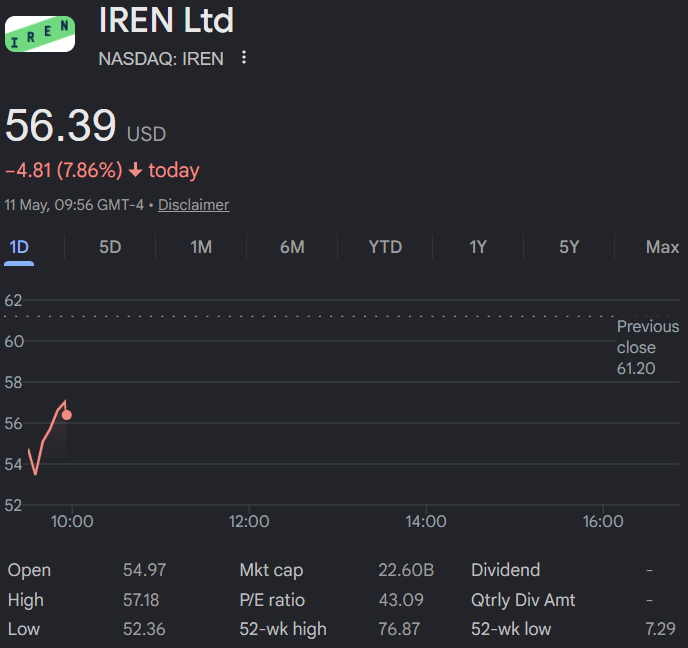

@WavesG51256 @daniel_koss @kevinxu He sold his IREN to go into $HIMS. Kindly never associate him with IREN ever again.

English

🧐

Is the market going risk-off and rotating into quality?

$NBIS $IREN

English

People were panic selling this this morning btw

After $NVDA just partnered with them 😂😂

Weak hands

English

Looks like $IREN shareholders are rotating to $NBIS

$NBIS: 6%🟢

$IREN: -12.30% 🔴

English

If you sold any good long term stocks this morning because of short term headlines or price action, I'm just going to tell you right now that you probably shouldn't attempt to do this for a living. It's not going to be a fruitful career path for you. Stick to something easier.

English

$IREN

"we haven't disclosed the specific amount of GPUs"

1. 🤮 reminds me of $NBIS

2. Setting a terrible precedent here for future deals

3. Making it purposely difficult, to not let analysts properly value your 2027 revenue

4. Increasing the polarized view on @IREN_Ltd by the market

However:

"approximately 60MW of air-cooled Blackwells"

1. You typically don't talk about gross capacity in a deployment like this

2. If it would be gross capacity, the GPU hour rate at IT level would be crazy high (at PUE 1.2, $680m / 50 = 13.6m/MW)

3. At 60MW IT load, and ~14kW draw at DGX server level, we can get to ~4,286 DGX systems with 8 GPUs per.

4. Based on this we can conclude that 60MW of IT load can run approximately 34k DGX B300.

5. 34k DGX B300 at $680m/yr, would represent a GPU hour price of $2.28

Now this is the problem with not disclosing your GPU quantity.

You purposely make your business model look bad, because by approach, you get to a GPU hour price that would imply a payback period of 4 years, where only the last year of the contract is 100% margin.

But of course, we can also take "the glass is half full" approach.

IREN has ordered 50K B300s from Dell.

They have 2 purchase orders for this, 1 between Dell Canada and IE CA Leasing Ltd for 4 phases, and 1 between Dell USA and IE US Hardware 1 Inc (amended from IE US Hardware 4 Inc on April 27, 2026).

The order for Canada is divided in 4 phases, and are going to Mackenzie for 80MW of gross capacity, which happens to be 4 buildings of 20MW.

The order for Childress is divided in 2 phases, and are going to DC35 and DC36, (as depicted in the earnings presentation) and those are 50MW gross.

The purchase price of the order for Childress was $1.2B, and for Canada it was $2.3B

If we go with 50,000 B300s for a total of $3.5B then $1.2 would represent 34.285% of the 50,000 GPUs, or 17,140 B300s rounded down.

For this calculation I will consider that $IREN will deploy 17,140 GPUs in 50MW gross capacity in DC35 and DC36 of block 3 in Childress..

That would imply at 1.2 PUE, IREN can run 17,140 B300s in 41.67MW IT load.

Now by that ratio, they can run 24,680 GPUs in 60MW IT load — a massive difference with 34k units through the Nvidia DGX reference calculation.

If common sense is applied, you can still get to 2 completely different outcomes, that show a difference of more than 9k GPUs.

The GPU hour rate at 24.68k GPUs would be $3.145 per B300, as MASSIVE difference from the earlier calculated $2.28.

Sure, the DGX system may be a factor here. And I'm sure that the reality is somewhere in the middle.

But I personally hate this as an investor, to be unable to calculate profitability on unit economic basis.

After all, contracts are signed on a $/GPU hour basis. Why hide this from your investors?

Not being able to calculate payback periods, unable to calculate ROIC. And most importantly, we cannot properly assess the $NVDA deal on a contract basis.

I really hope the payback period of this contract is not 4 years.

I want the glass to be half full, but by starting to censor the purchases, IREN is taking a step in the wrong direction.

Not a fan of this.

English

? retweetledi

A sure fire way to tell someone has never seriously run money is seeing them snipe at folks who get calls wrong.

Anyone who has been in this business for more than a minute knows as right as you are today, you will no doubt be equally wrong at some point in the future.

English

? retweetledi

See this interview: research1.ml.com/C/?q=HZvB9qMdE….

Will Gray and Charles Nelson walk Kalei Akamine through air permitting as a gating constraint for behind-the-meter power generation in West Texas. The headline: PSD (Prevention of Significant Deterioration) permits are running ~18 months with no real guarantee, versus ~90 days under Title V — so timeline-sensitive projects (e.g., a gigawatt build by Q4 '26) can be killed by permitting alone, even if equipment is ready.

Their workaround at Coppers Hawk (their first site, named after a West Texas hawk) is a "power islands" / microgrid architecture — spreading generation across sites roughly a mile or more apart so TCEQ doesn't aggregate them as a single major source. Will and Charlie both caveat this heavily: aggregation determinations are subjective at TCEQ, depend on ownership structure and end user, and you can't just assume distance buys you a different permit class. They flagged that this is industry-wide, not site-specific, and that Trump's "Executive Order Speed" hasn't produced PSD guidance yet.

Beyond air, Will points to zoning and entitlements as the next layer — and credits Ector County Commissioners and Judge Fawcett for being workable, noting county-jurisdiction sites are meaningfully easier than building inside city limits.

--------------

Being in attainment is one of the quieter reasons TCDC's permitting math works at all. Here's where Ector County's status saves NUAI real time, money, and design flexibility:

No emission offsets to hunt for. This is the biggest one in dollar terms. In ozone non-attainment, every ton of NOx or VOC the facility emits has to be matched (at 1.15:1 to 1.5:1 ratios depending on severity) by buying or banking reductions from existing sources. In tight non-attainment markets like Houston or DFW, offsets can run $20K–$80K per ton and sometimes simply aren't available at scale. For 450+ MW of behind-the-meter gas generation, NOx emissions alone could require hundreds of tons of offsets. In Ector County, that line item is zero.

BACT instead of LAER. Texas Critical Data Centers gets to argue for Best Available Control Technology, which explicitly weighs cost-effectiveness and energy/economic impacts. In non-attainment, LAER (Lowest Achievable Emission Rate) applies — and LAER cannot consider cost. Whatever's been achieved in practice anywhere becomes the floor. For gas turbines and reciprocating engines, this is the difference between "SCR + good combustion controls" and "the most aggressive emission rate ever permitted on similar equipment, regardless of what it costs to install or operate."

Higher major source thresholds. In attainment, you're a major PSD source at 100 tpy (for listed categories that include fossil-fuel-fired steam electric >250 MMBtu/hr) or 250 tpy otherwise. In serious/severe/extreme ozone non-attainment, those drop to 50/25/10 tpy. The power-island microgrid strategy Will and Charlie described works much better under attainment thresholds — even if TCEQ does aggregate two islands, the combined number has more headroom before tripping major NSR.

No statewide compliance certification. NNSR requires the applicant to certify all its other Texas major sources are in compliance. Not required here.

The aggregation argument is more forgiving. In attainment, the conversation with TCEQ is essentially "are these one source or several?" In non-attainment, even if you win the aggregation argument, smaller individual sources still may hit lower thresholds — so the workaround buys less. In Ector, the workaround buys more.

Faster, cleaner public process. PSD is still the 18-month process Will mentioned — attainment doesn't eliminate that. But the public participation stage is meaningfully less hostile when the area is in attainment. Non-attainment permits attract more scrutiny from EPA Region 6, environmental groups (especially in HGB and DFW), and the agency itself, because every new ton has to be reconciled with the SIP.

English