@trevhesinvests @YodaStockInvest Hold both but $PGY >> zetachain:native . Flawless execution and no crazy SBC

English

seb

20 posts

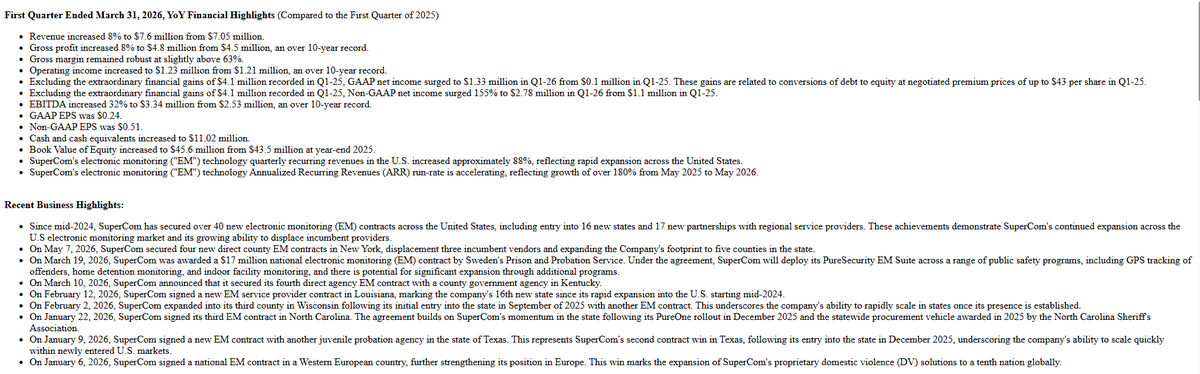

$SPCB Q1'26 earnings are out! Revenue: $7.6mm; +8% YoY Gross Profit: $4.8mm (10yr. record); +8% YoY EBITDA: $3.3mm (10+yr. record); +33% YoY Cash of $11.0mm SPCB's Q1'26 EM quarterly U.S. recurring revenue increased 88% due to the expansion. SPCB's ARR is accelerating, reflecting 180%+ growth from May 2025 to May 2026.

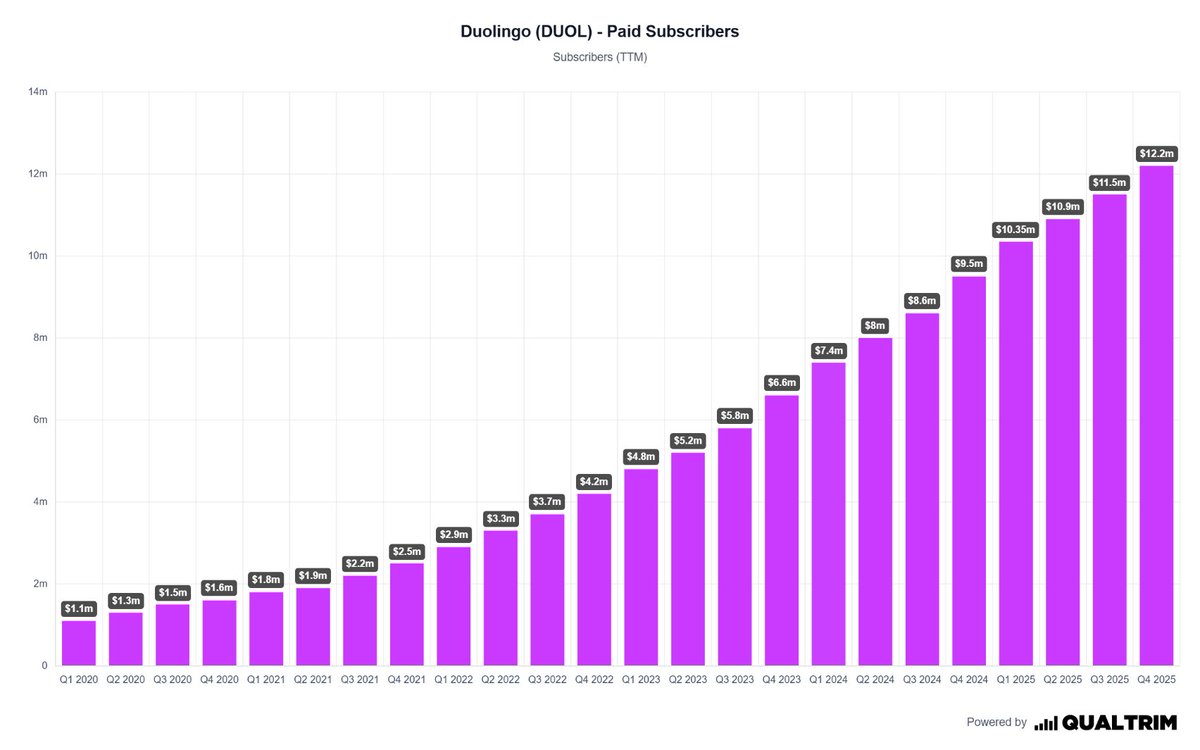

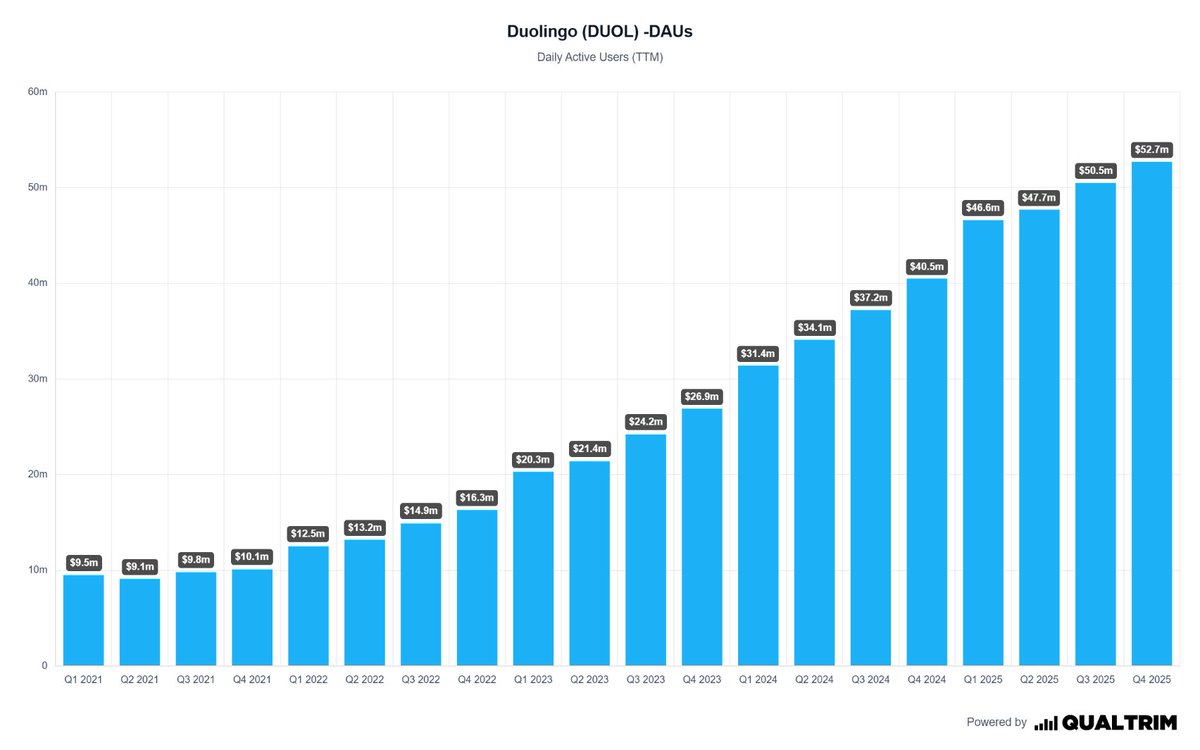

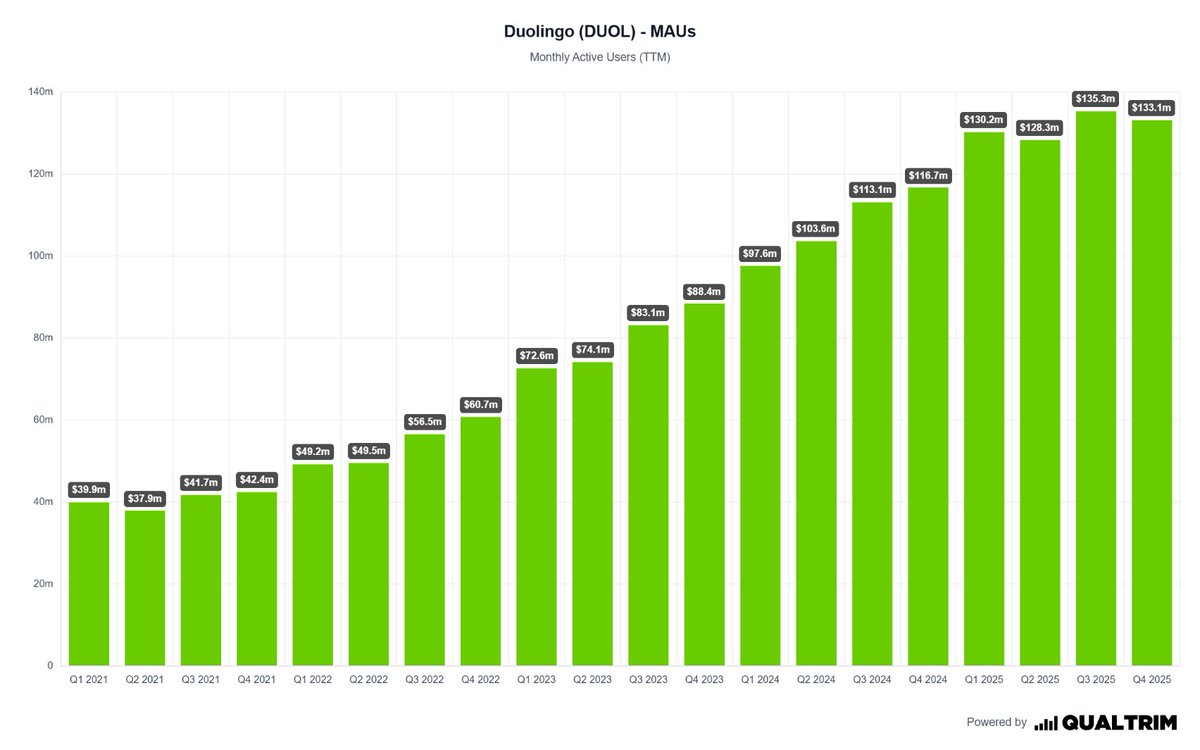

Duolingo Q1 Results Revenue +27% Free Cash Flow +45% Total Bookings +14% Paid Subscribers +21% MAUs +6% DAUs +21% $DUOL: -14.4% after hours

@alc2022 $DUOL is a shit stock. Anyone still saying BUY= Bag Holder.

The next company I’ll be covering is a deeply misunderstood one. CEO has called the current industry environment a “bloodbath". Companies are going bankrupt left and right due to a regulatory change. The stock got sold off with the entire sector… but here’s the twist: This company should actually benefit massively from the change. It has a razor-blade recurring revenue model with extremely lucrative margins. In Q4’25 alone they sold a massive amount of devices, roughly 20% of everything the company has sold in its entire history. This is directly tied to the regulatory shift. Valuation doesn’t screen cheap, but accelerating revenues on already fast growth, combined with economies of scale as they ramp, should drive earnings. I believe the stock is extremely undervalued. Full write-up dropping on my Substack soon. Stay tuned!

1/1 🛡️ SuperCom $SPCB: The SaaS-Transformation Play in Public Safety Tech 🚀 While the market focuses on large-cap tech, a massive turnaround has been completed in the Micro-Cap space. SuperCom has evolved from a hardware provider into a high-margin SaaS powerhouse. Here is the deep dive for 2026: 1. Company Overview SuperCom is a global leader in IoT-based security solutions. After a strategic pivot, the company now dominates the Electronic Monitoring (EM) sector, providing critical tracking infrastructure for justice systems in the US, Europe, and the Middle East. 2. Product Showcase The core of the business is the PureSecurity Suite. This end-to-end platform includes: PureOne: An advanced GPS tracking ankle bracelet with industry-leading battery life. PureTrack: A cloud-based software platform for real-time offender monitoring. Victim Protection: GPS solutions for domestic violence cases, already a national standard in several European countries. 3. Valuation Snapshot (Est. March 2026) Market Cap: ~$38.6 Million Enterprise Value (EV): ~$37.1 Million Net Debt (ex Lease): ~$9.2 Million (Improved significantly via debt-to-equity swaps) P/E Ratio (TTM): ~10.3x EV / EBITDA: ~6.2x (Deep value territory) 4. Earnings Snapshot (FY 2025)2025 was a record-breaking year for SPCB: Revenue: ~$27.4 Million (Driven by 30+ new US contracts) Net Income: ~$6.0 Million (First 9 months of 2025) Gross Margin: ~61% (Up from 45% due to the SaaS shift) Recurring Revenue: SaaS now accounts for over 80% of total EM sales. 5. Peer Group Comparison Compared to industry giants like Axon Enterprise $AXON or $ALRM, SuperCom trades at a massive discount. While Axon commands a P/E of 60x+, SuperCom sits at ~10x, despite showing higher relative profit growth in its niche. It is a prime candidate for an acquisition by a larger player looking to fill a gap in post-custody monitoring. 6. Forecast 2030 Projected EBITDA: $12 Million – $15 Million Target Revenue: $55 Million+ Drivers: Continued expansion in the US (currently in 16 states) and the digital transformation of European probation services. High operating leverage means new contracts fall straight to the bottom line. 7. Opportunities & Risks Opportunities: High barrier to entry (government contracts) -nearly 90% customer retention -massive operating leverage Risks: Micro-cap volatility -geopolitical exposure in Israel -potential for dilution if further expansion capital is needed 8. Final Verdict SuperCom is a rare "Alpha Play" in the security tech sector. It combines the stability of long-term government contracts with the high margins of a SaaS business. At current valuation levels, the market has yet to price in the full extent of its profitability turnaround. Disclaimer: Not financial advice. Mining is high risk. Always do your own DD. #SPCB #SuperCom #SaaS #Investing #Stocks #SmallCap #PublicSafety #ValueInvesting #Nasdaq

I notice people mentioning dilution risks in $SIVE. I've said it before, a dilution less than 5% is enough for $SIVEF to grow into a profitable company. Dilution is a non-factor at these valuations. When I bought at $0.3, the dilution risk was real. Now? Not at all.