Stan

167 posts

给大家说个恐怖的故事,大家都觉得光学很猛对吧 来看一下市值: $LITE 780亿美金 $COHR 792亿美金 $aaoi 163亿美金 $GLW 1792 亿美金 这些加起来3527 亿美金,都比不上 $MU 的一半市值,然后全在说光学是泡沫……… $SNDK 一家都2千亿市值……… 所以说, 光学真的很早………太早期了

The 25 year old who turned $225 million into $5.5 billion in 12 months is quietly building a position in a stock almost NOBODY is talking about. Leopold Aschenbrenner is the former OpenAI researcher who launched Situational Awareness LP in September 2024. His fund returned 47% after fees in the first half of 2025. His thesis is simple: AI will be the largest infrastructure buildout in human history, and the market has not priced it in. In his most recent 13F he kept adding to one specific name quarter after quarter. Hut 8. He increased his position by 43% in Q4 2025 alone. This is one of his most asymmetric setups right now. Hut 8 has quietly locked in two of the largest AI infrastructure contracts in the country. A 15 year, $7 billion lease at its Louisiana campus with Anthropic as the end customer and Google as the financial backstop. A second 15 year, $9.8 billion lease just announced this week at its Texas campus with an investment grade tenant. Combined base term contracts: $16.8 billion. If all renewal options are exercised: over $42 billion. The entire market cap of Hut 8 today is a fraction of that. The company also holds over 16,000 Bitcoin and a $200 million credit facility at a fixed 7% rate. That’s rare optionality on the side. When he discloses his new trades, we will share them here. Turn on notifications so you don’t miss our alert, this is VERY important. If you don’t follow us, you might regret it.

Goldman just put a number on the AI buildout: $7.6T from 2026-2031. They explicitly flag optics as the next “buy out the store” chokepoint after memory. The numbers behind the thesis: +Compute alone is $5.1T of the $7.6T total +Annual AI capex grows from $765B in 2026 to $1.6T in 2031 +Data center cost per MW jumped from $10M (cloud era) to $15-20M (AI era) +A single $50K accelerator depreciates $10K/yr but goes economically obsolete faster than the schedule +NVIDIA’s GB300 NVL72 packs 72 processors per rack, linked by hundreds of thousands of km of cabling In the repot they state: similar episodes of intense, short-term pricing pressure are likely to recur across other critical components such as interconnect, optics, storage, and packaging.” Meaning the same dynamic that just sent memory parabolic is queued up across the entire physical layer of AI infrastructure. The “AI factory of the future” data center will pack 576 GPUs per rack at 500+ kW, requiring liquid-only cooling and millions of GPUs deployed at the >1 GW scale. None of that scales without optics. Memory just ran (still going). Photonics is just warming up. Full disclosure: Goldman is confirming what’s been playing since the late last year. A lot is already priced in. The alpha is front-running institutions, not reading their reports. But $7.6T over 6 years doesn’t get fully priced in 6 months. Plenty of runaway left.

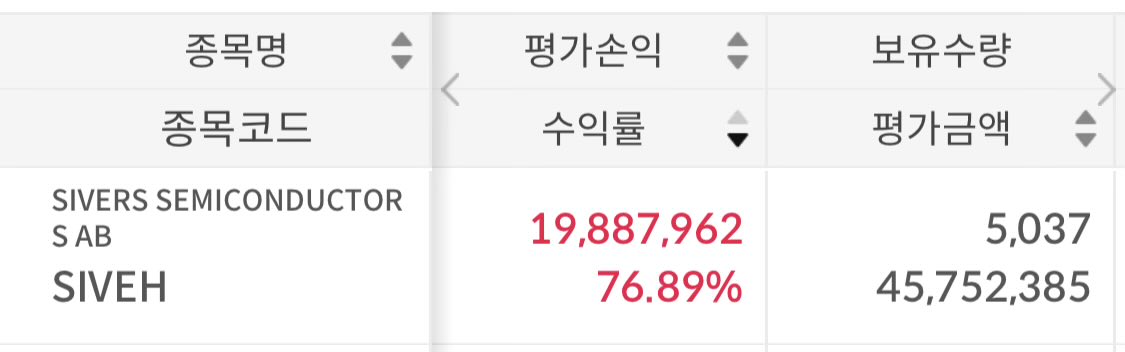

Great find. Basically from old investor deck + fundraising amounts: Looks like Celestial has been direct customers of $SIVE. So: $MRVL is likely buying lasers direct from $SIVE now instead of through Poet (which bought Sivers lasers to package them). Since Celestial is designed around Sivers lasers originally. Marvell probably prepared to vertically integrate away packaging IP + assembly for higher margins anyway. Going direct to $MRVL is very bullish for $SIVE.

Literally just having a delusional golden retriever mindset measurably changes outcomes and physiology. Sleep badly? Convince yourself you're well rested. Stressful day? Convince yourself it's fuel. Failed? Convince yourself it's useful data.

$POET said Marvell canceled all purchase orders tied to Celestial AI, including initial production orders first disclosed in 2023. The cancellation was tied to alleged confidentiality breaches, while POET said it is still serving other customers, including a separate $5M order.