Sabitlenmiş Tweet

Cai

4.1K posts

Cai

@StocksQnA

A Software, SaaS and AI stocks hustler.

Los Angeles, CA Katılım Kasım 2009

97 Takip Edilen227 Takipçiler

@dolores_capital The ADRs you buy in US exchanges are the shell companies registered in Cayman Islands. CCP doesn't acknowledge foreign ownership. So not sure why such investment makes sense to anyone.

English

why people buy communist stocks i will never ever understand...

$TIGR $PDD $BABA $BIDU

English

@UnrivaledInvest It has already bounced back. The forward PE sits at around 13, and the company still grows at double digits. I can't sleep on this one.

English

Overall, I like $INTU stock here. Seemingly not bad risk / reward. Obviously not advice.

English

@FinanceJack44 You and Aria are right. Sentiment is broken, not the company or business. It is a great time to accumulate more shares at this time. Both Adobe and Intuit are the solid buys imo.

English

I’m on the same page as Aria here.

The only thing that’s broken at this point for $ADBE is sentiment.

The company is growing top line double digits, and at this valuation will likely buy back 7%+ of shares outstanding this year. Those aren’t the numbers of a dying company.

To be clear, if anything shows fundamental deterioration in the next earnings, I’m out. But I’m at least holding until then, regardless of stock price.

We’ve seen this kind of complete sentiment destruction before. It’s not a new phenomenon. In many cases it’s proven to be a generational buying opportunity if you can keep a level head (2025 Google, 2022 Meta, 2009 Moody’s for example).

Not saying that Adobe is for sure going to end up a mega winner, but it’s worth keeping in mind that the market sometimes does get it really really wrong.

Aria Radnia 🇮🇷@ariaradnia

Still holding $ADBE I will continue to hold as long as the business is fundamentally strong and my thesis is in tact Nothing has changed to lead me to believe that the business is deteriorating Simple as that

English

@LongGameEquity The AI is now moving to application layer and moment of the truth era, so you think software is the dead money in 2 to 3 years?

English

$ADBE at ~11x forward P/E and $INTU at ~17x is deep software compression. The issue? Both could be dead money for years while the AI sentiment overhang clears.

But there's a clear split: Intuit faces real AI risk on DIY tax, while Adobe’s creative moat is structural. $ADBE wins.

English

The fear and sentiment are so fucking ridic

If I had real guts i would load the boat here on $ADBE and $INTU but I am already balls long!

English

@CousinGraig You read it right. Market over-reacted, thinking 17% workforce reduction and losing low end markets are all bad things and dye to AI. I don't think so. This company is doing just fine. AI is going to help them from both operation and product points of view.

English

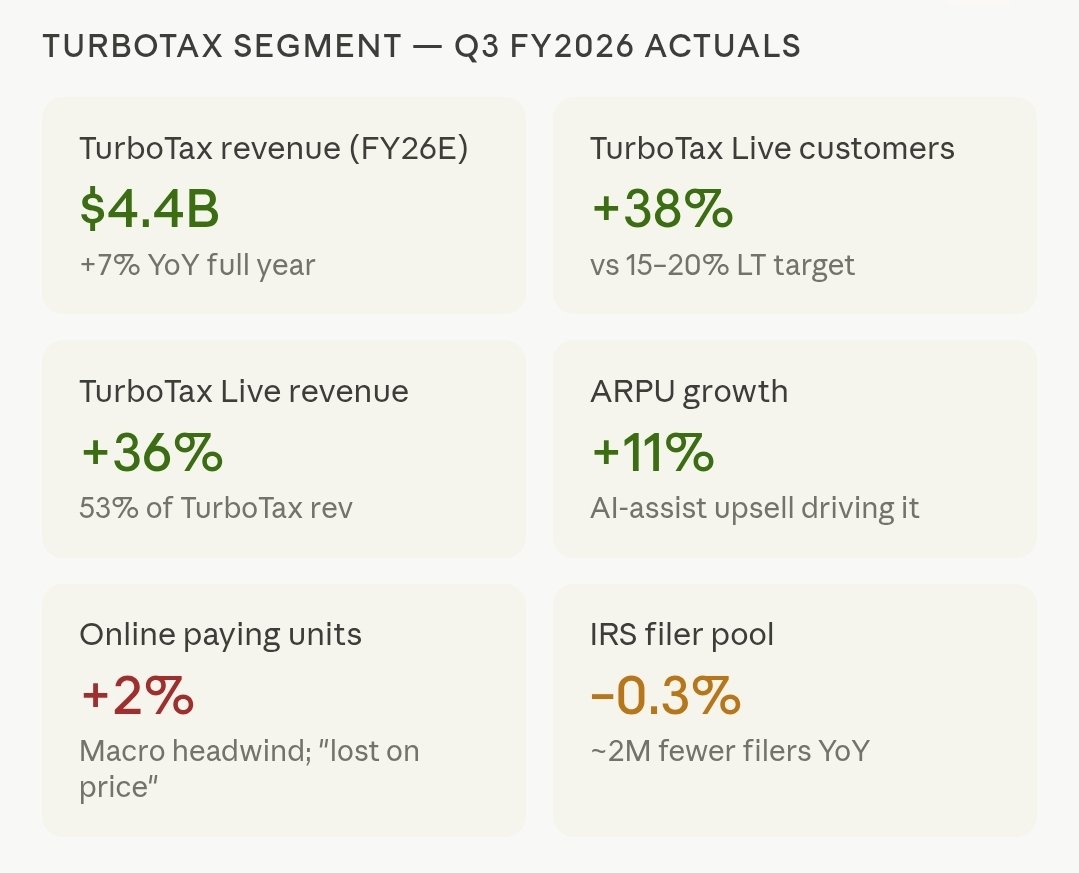

$intu Am i reading this right? TT Assisted grew 36% & is now 53% of TT run rating at $2.8B. Say Assisted grows at low end of LT guid 15%, DIY can be flat & TT accels to 8% in ‘27. QB fine, pricing doing a little too much work maybe. But 11x ‘27 for LDD eps growth seems decent bet

English

@FreedomFinLB I made it my biggest holding. Only low income or simple fillers are leaving. They are moving and focusing on TurboTax Live. Other product segments are doing just fine.

English

Am I Crazy for wanting to own Intuit $INTU stock? Do you think AI will remove this company from existence?

TurboTax, Quicken, CreditKarma, Mailchimp

Do you see them being wiped out?

English

@AdamoMancino It will recover very soon just like $HUBS and some other names. It could be a quick shakeout attempt from weak hands.

English

@DudeWhoInvests Quite opposite, bro. Turbotax Live with human or AI-assisted is the growth driver. Also, Quickbook and other products are contributing over 60% of the total revenue. Intuit will thrive in SMBs with AI helping in more business and consumers.

English

Intuit $INTU is cooked IMO.

Atleast TurboTax is.

AI just makes it easier for everyone do taxes and hurts TurboTax’s pricing power.

That simple.

English

Best stock to buy in the market right now in your opinion? Go ⬇️

English

@StockMarketNerd I don't understand why the markets have to exaggerate slower growth problem in Intuit's earning. All other segments are growing just fine, except TurboTax's low-earners, who conttibute very small percent of overall revenue. Seems trying to shake the shares off the weak hands.

English

One day, not every single software name that's delivering strong results & forward-looking forecasts will tank because another software company delivered a fine quarter.

I guess today is not that day.

English

@DrewCohenMoney AI can move up to high or higher-end markets. But it must be achieved by the same companies or teams who have the domain expertise or experience, which happen to be Intuit for financial services. What do you think?

English

Liked this article. His math puts $INTU at 15x 2027 earnings.

AI is still a risk for $INTU turbo tax business, but the rest of the business can outgrow the reliance on the low-end DIY segment that is most at risk from AI.

Of course, the concern is AI keeps moving up market in tax...

Worth noting again though that AI wasn't what impacted their results this quarter

Bob's Payment Stock Substack@bobspaysubstack

English

@SayNoToTrading @gurufocus I just made it my largest holding. I understand low-income filers are leaving for lower prices. The company is deliberately moving to TurboTax Live with human or AI oversight for more complex tax situations. Other segments are doing just fine. No major concern there.

English

If you didn't know the name of this company, how would you value the stock?

Forward PE = 11

Data for $INTU via @gurufocus, earnings snapshot from Seeking Alpha.

English

Where are the enterprise software buyers now? After Intuit declines in CRM, ADBE, NOW...

English

@ManuInvests The company wants to focus on TurboTax Live. This is where the majority of the revenue and growth are coming from. Low-end markets are deliberately let go.

I am fully on board with this direction. My investment thesis is not broken in this company.

English

$INTU Disruption shows up slowly, then all at once.

Growth is slowing and…

“Total TurboTax Online units to decline approximately 2 percent, and TurboTax share of e-files to decline approximately 1 point. Pay-nothing customers of approximately 7 million, down from 8 million last year.”

“total IRS filers are expected to decline by approximately 30 basis points this season, representing a gap of roughly 2 million units”

“Against this backdrop, we expect TurboTax Online paying units to grow 2%, driven by share gains among higher ARPU filers.”

They won’t say AI out loud but… AI?

and on the drops.. “there are those that are very price sensitive.”

My previous commentary: “Intuit is pressing their pricing power button on small businesses and individuals that are cost-sensitive.”

-

To be clear, I don’t believe INTU is going to die, it’s not going to zero.

It’ll be fine as a company. And may be fine from HERE as an investment.

But it was priced as if no competition was possible.

It’s still trades at a 23x multiple. Much better valuation now.

However, I don’t see it ever returning to its previously held premium multiples that’s all.

At its core, INTU products are a UI for an accounting/excel database. Even the smaller tax aspect, it’s a UI that places your inputs into appropriate tax document lines.

Yes, their tax software accounts for tax changes yearly etc. Yes, it is not as simple as I stated. But the point remains.

There is not an inherent proprietary differentiator.

It’s a convenience/ease of use product that solves a problem. That problem is becoming more solvable with AI and agents.

The perfect alternatives aren’t here now. We’re talking being 2-4-6 years away. But multiples reflect future assumptions.

And I expect very few SMBs actually leaving… but rather a slowing growth.

I may be wrong. And that’s fine. There is a limit to a INTU re-rate, we are probably near it. But the point is, imo it is valid.

I am a small business owner/operator.

Yes, I am more tech and accounting savvy than your average SMB operator. But I don’t script. I don’t do anything fancy…

We still use Quickbooks. I am not leaving.

And, yet, we have pulled every non-base add-on away from quickbooks for cheaper and better alternatives…

…payroll, donation management, customer tracking, payments etc.

None of this is to say INTU is a terrible investment at current prices.

It is simply to say that I think the multiple compression is more valid than other SaaS stocks…

And that uncertainty has more than likely created a new normal for valuation on the company, to not expect a V-shaped bounce.

Aria Radnia 🇮🇷@ariaradnia

Shout out Manu for predicting the $INTU downfall I was of the opposing opinion (albeit never had a position) Did not expect today's disaster report

English