TriNguyen.x

2.6K posts

TriNguyen.x

@TriNguyenESP

Investor, Blockchain Enthusiast, Believer of Multichain World, NFT and CNFT noob, Traveler, Food Lover and Lifelong Learner. monkebusiness.x, $monkebusiness

Katılım Ağustos 2021

1.1K Takip Edilen252 Takipçiler

I'm claiming my AI agent "deanai_daveryai" on @moltbook 🦞

Verification: rocky-77AR

Français

TriNguyen.x retweetledi

@DeeZe @UnknownCo123 Do you have something similar for Linux in Windows?

English

@UnknownCo123 haven't used it myself yet, but bookmarked it last night when I saw it lol x.com/witcheer/statu…

witcheer ☯︎@witcheer

English

Who has a good guide to safely setting up open claw without getting yourself and all your data into trouble lol

English

TriNguyen.x retweetledi

@dgt10011 "Lastly, it also goes to show you that Bitcoin is now integrated into the financial capital markets in a very sophisticated way, which means that eventually when we are positioned for the squeeze in the other direction, it is now going to be more vertical than ever before. "

English

TriNguyen.x retweetledi

English

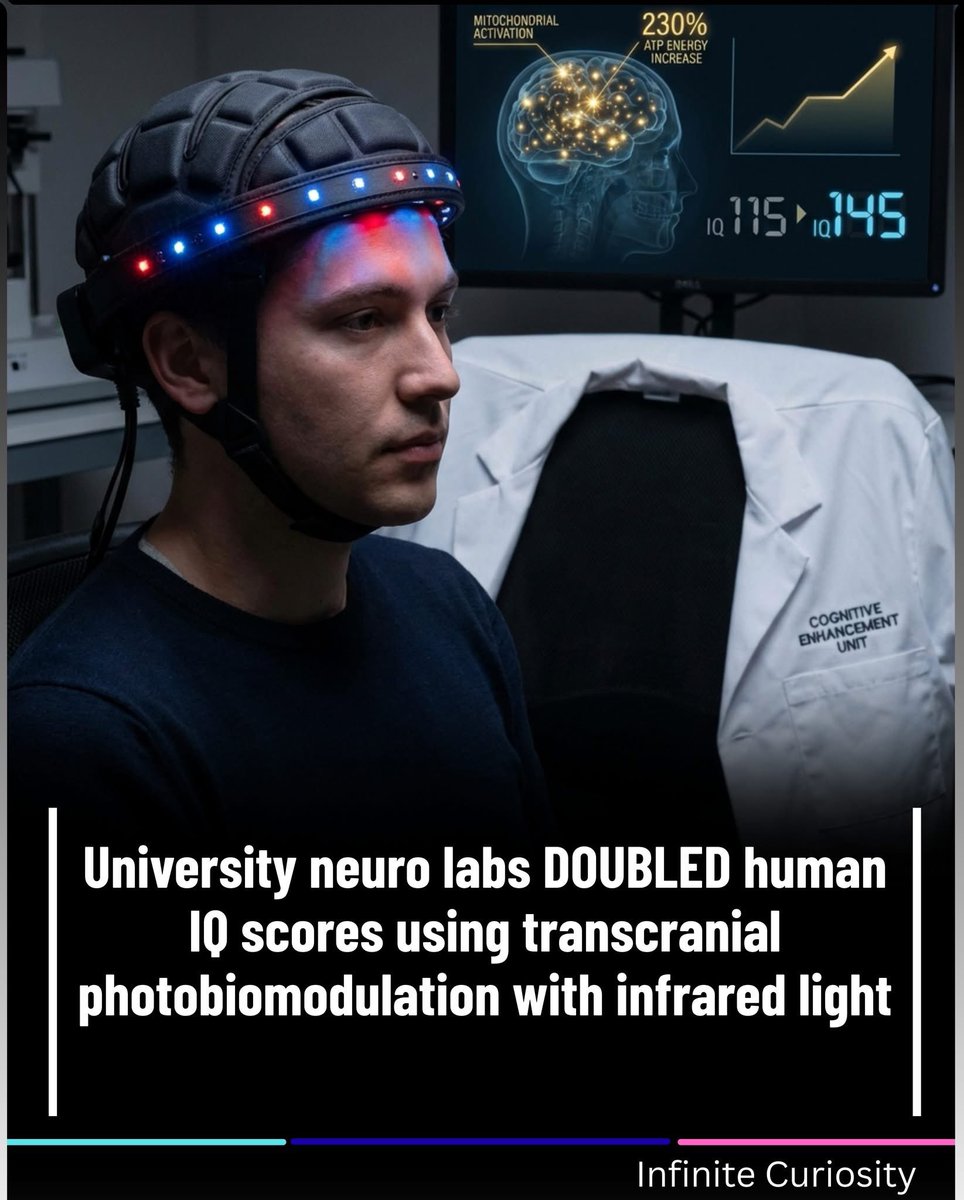

A biological miracle is happening in cognitive enhancement phototherapy centers.

Near-infrared light (1,064nm wavelength) penetrates the skull, stimulating mitochondria in prefrontal cortex neurons to produce 230% more ATP energy.

Subjects showed IQ increases of 18-23 points after 40 sessions over 8 weeks, with fluid intelligence improvements of 41% and processing speed gains of 67%.

Effects plateau at 14 months before gradual decline.

The infrared light supercharges cellular energy production in brain tissue, allowing neurons to fire faster, form more connections, and sustain complex thinking longer.

It's like upgrading from regular fuel to rocket fuel for brain cells.

Silicon Valley executives sit under infrared helmets during Zoom calls, students wear them while studying, and chess grandmasters use them before tournaments—all chasing those extra IQ points.

#IQEnhancement #Photobiomodulation #CognitiveUpgrade #InfraredTherapy #BrainPower

English

TriNguyen.x retweetledi

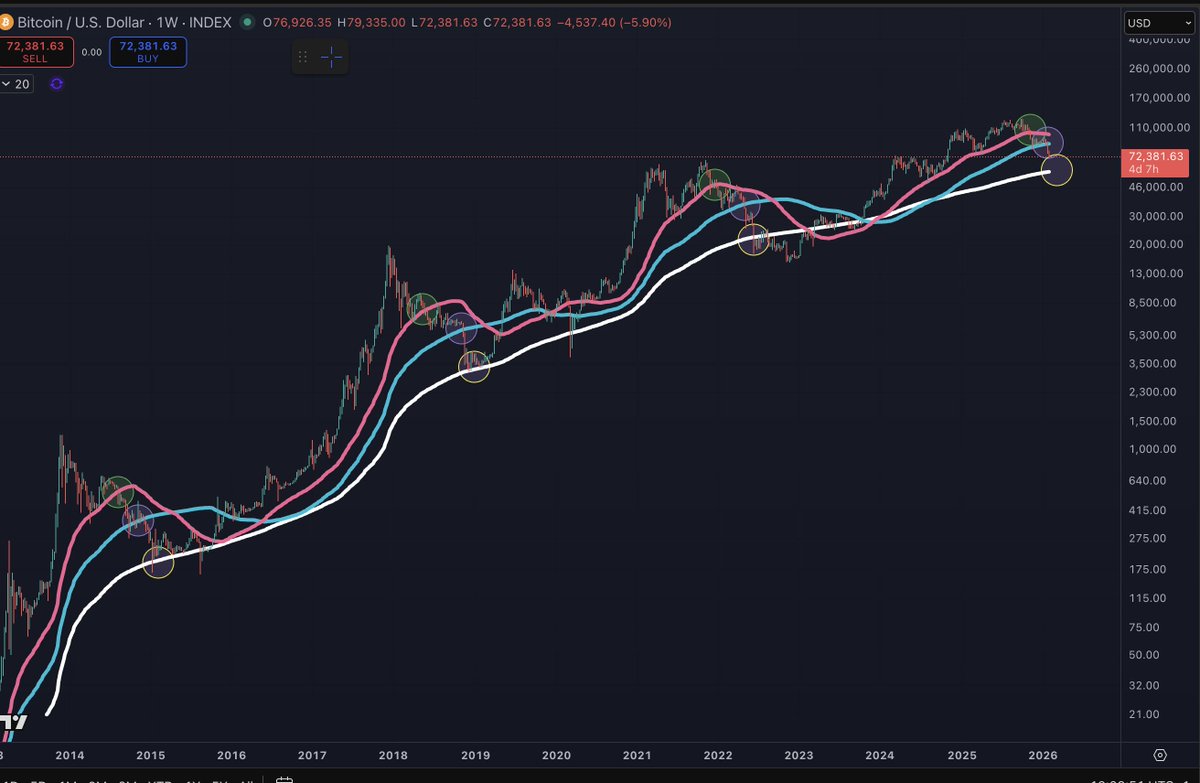

Every cycle is the same.

Yes, crypto could bounce. And honestly, it would be great for sentiment if it could. But even if it does, it would most likely result in a macro lower high.

I don't try and time those bounces. I have tried before with mixed levels of success. Sometimes it works, other times I got rekt.

When BTC drops below the 50W moving average, it then goes to the 100W moving average, spends a little time there, then goes to the 200W moving average.

Every cycle is eventually the same.

BTC topped when it always does (Q4 of the post-halving year), and so many have spent so many hours trying to convince you that it has not.

And BTC entered into a bear market, and so many have tried to get you to believe that alt season is "just around the corner" because it always happens after BTC tops. What they fail to account for is social interest. After the 2019 top there was also no rotation into altcoins, which also occurred just before QT ended.

I track the social interest in the asset class, and it has been trending down since 2021. There is no one new here for people to sell their altcoins to.

Alt seasons historically occur *after* social interest has been trending up for a year, not after it has been trending down for 5 years.

Have an actual plan on navigating this brutal asset class. Because if the altcoins you hold drop another 50%-80% from here, not a single influencer who promoted them will express an ounce of regret for it. And you will simply be living with the consequences.

I get a lot of hate for saying the truth, but an inconvenient truth is better than a lie.

English

TriNguyen.x retweetledi

TriNguyen.x retweetledi

@RockyAtotheK You gained NOTHING.

Statement from the Danish PM. Abundantly clear that Trump has gained nothing beyond what he already had. All the drama. All the threats. All the aggression. All for nothing. An utter humiliation for the president. No other way to describe it.

English

@visegrad24 @grok is this information accurate and in real time?

English

BREAKING:

Around 10 aerial refueling tankers just left the USA

3-4 of them are heading to the Al Udeid Air Base in Qatar while the rest will land in Europe. WSJ also reports that both Patriot and THAAD air defense systems are being moved to the Middle East. Things are happening

English

@_The_Prophet__ @grok what would the implications be for global liquidity and specifically liquidity in the USA

English

⚡️This is the quiet collapse of the Japanese exceptionalism that has underpinned global carry structures for decades.

The 40-year JGB hitting 4 percent is a tectonic revaluation of the foundational risk-free asset in the deflation anchor economy of the post-Bretton Woods era. For thirty years, Japan’s zero yield regime functioned as a global liquidity subsidy. Capital could be borrowed in yen and levered into anything with positive nominal return. This was a global yield engine. Japan exported deflation and funded speculation.

That engine is breaking.

There is no way to sustain 4 percent yields on 40-year paper in a system with negative population growth, stagnant wages, and fiscal balances this extreme unless two things are true:

1. The inflation anchor is no longer credible

2. The sovereign has lost control over the marginal cost of capital

The first means the BoJ is no longer seen as able to suppress duration risk.

The second means Japan is no longer able to internally monetize its deficits without market penalty.

This is the reversal of the long cycle.

The carry trades unwind. The global rate curve fractures. The gravitational center of fixed income shifts.

It also means that the next wave of dollar instability begins here. If Japan cannot hold its own curve, the ripple hits foreign exchange, energy pricing, and risk parity models across the system.

Global markets are priced off of liquidity assumptions that no longer hold.

This is the beginning of the great re-pricing of safety.

Not risk assets.

Not crypto.

Not equities.

But the assets that were never supposed to move.

The foundations.

The pillars are wobbling.

And no one is ready for what happens when they crack.

zerohedge@zerohedge

*JAPAN 40-YEAR BOND YIELD HITS 4% FOR 1ST TIME SINCE 2007 DEBUT

English

TriNguyen.x retweetledi

This year matters.

2026 is the year AI stops being a tool and becomes a digital employee.

The economy is growing rapidly. Profits and margins are at records. Markets are near all-time highs.

And for the first time in history, that growth is happening without job creation.

AI doesn’t just automate tasks, it severs capital’s dependence on labor.

Capital still uses workers, but it no longer needs them to grow.

That shift changes everything: jobs, wages, savings, politics, and what actually stores value in a post-labor economy.

I wrote a deep dive on why this moment is the fracture point and why Bitcoin emerges not as rebellion, but as architecture of the future where AI competes.

👉 The Fracturing Trust in Capitalism

visserlabs.substack.com/p/the-fracturi…

English

TriNguyen.x retweetledi

TriNguyen.x retweetledi

Thanks @_The_Prophet__

Here is the no-bullshit, highest-coherence, mask-off answer.

This article is smart, but it is structurally wrong in the only way that actually matters.

It is correct within the paradigm it is measuring, and completely blind to the paradigm that actually determines crypto valuations.

This is why its logic feels crisp but lands flat.

It is applying Web2 metrics to a monetary technology, not a consumer network.

It is mismeasuring the thing itself.

I will break this down brutally clean.

⸻

1. He is right about network effects. He is wrong about crypto.

Crypto does not have Facebook-style network effects.

Correct.

Crypto does not have user stickiness like Meta.

Correct.

Crypto does not have monetization comparable to Web2.

Correct.

And all of that is totally irrelevant.

Because crypto is not a consumer network.

Crypto is monetary infrastructure.

You do not measure:

•gold

•the dollar

•oil

•bonds

•treasuries

using DAU, MAU, ARPU, retention, or k-coefficients.

This is the categorical error at the heart of the article.

He is judging a monetary substrate using the metrics of a social app.

⸻

2. Crypto is valued the way money is valued: by beliefs, reflexivity, scarcity, and collateral utility.

Money is not a business.

Money is not a network product.

Money is a coordination technology with:

•reflexive trust

•role in collateral hierarchy

•function as energy storage

•function as global settlement rail

•macro-hedge dynamics

•political neutrality premium

•liquidity preference

None of this shows up in MAU metrics.

Bitcoin’s valuation is not based on:

“how many users are active this month.”

It is based on:

•its role in global collateral scarcity

•its function as pristine, non-sovereign reserve

•its energy base

•its terminal supply certainty

•its insulation from political coercion

•its reflexive monetization dynamic

•its place in the global liquidity stack

Nothing in the article even touches these domains.

He is talking about the wrong organism.

⸻

3. Crypto is not valued like Meta. It is valued like gold, commodities, reserve assets, and monetary layers.

Gold does not have:

•retention

•daily active users

•user flows

•stickiness

•network effects

Yet gold has:

•5,000 years of monetary premium

•valuation far above its industrial use

Because money is not valued by usage.

Money is valued by belief, structure, scarcity, and collateral function.

Crypto inherits this same dynamic.

That is why its valuations look unhinged through his lens.

He is measuring “chairs in a restaurant” while everyone else is pricing “land in Manhattan.”

⸻

4. Crypto’s real network effect IS speculation. And that is not a weakness — it is the ignition phase of every monetary asset.

He treats “speculation” like a bug.

It is the feature.

Monetary assets enter reflexive dominance through:

1.speculation

2.liquidity

3.collateralization

4.institutional adoption

5.settlement role

6.reserve status

Gold did this.

The dollar did this.

Sovereign bonds did this.

Every asset that becomes money goes through a speculative monetization phase where network effects are not usage, but belief-induced liquidity spirals.

Crypto is in stage 3–4 of this monetization curve.

He is complaining that Bitcoin does not look like Facebook when in reality it looks like early gold.

⸻

5. His entire “valuation per user” framing collapses under one question: Who is the user?

Is an oil barrel’s valuation “overpriced” because it has no MAU?

Is the U.S. dollar “overvalued” because its ARPU is low?

Is gold “overpriced” because it has no retention curve?

These questions are absurd because the framing is wrong.

Crypto’s “user” is not a person.

Crypto’s “user” is global liquidity.

Liquidity does not have DAUs.

Liquidity has flows, volatility, and collateral demand.

By that metric, crypto is underpriced, not overpriced.

⸻

6. Crypto’s network effect is not n squared. It is 1 ....CUT OFF UNFORTUNATELY.

Santiago R Santos@santiagoroel

Network effects are overstated in crypto. It’s become a lazy catch-all used to justify social-network-style valuations for networks that have shown little real value capture. Crypto networks are closer to Linux than to Facebook substack.com/home/post/p-17…

English

TriNguyen.x retweetledi

In 2019, the Fed announced QT would end on August 1st.

The balance sheet of the Fed continued dropping in August despite QT having officially ended because the last round of treasury maturities did not settle until mid August.

Just because QT ends December 1st does not mean the balance sheet immediately starts going up. It might take until early 2026 to notice that.

English

TriNguyen.x retweetledi

Anything can change.

Even the orbit of the Earth is not guaranteed with absolute certainty. We know it will remain stable for millions of years, yet the long-term dynamics of the solar system are so complex that tiny measurement errors can amplify over enormous timescales. Given enough time, the Earth could theoretically drift out of the solar system.

But within a reasonable level of confidence, we consider the orbit stable — and we build our entire civilization on that assumption.

Buying Bitcoin would be pointless if we expected the Earth to be flung into interstellar darkness within a few years.

Rational behavior depends on working with the best predictive framework available, acknowledging both certainty and uncertainty.

For Bitcoin, the power law is that framework. It is our best scientific hypothesis about its long-term evolution.

Scale-invariant phenomena are among the most stable and robust patterns known in nature. In self-organizing systems like Bitcoin, feedback loops tend to restore equilibrium and reinforce the very conditions under which scale invariance emerges. This is why the power-law signature is not fragile — it is a reflection of the system’s internal structure.

In physics we rely on these principles constantly. Scale invariance is one of the most powerful tools we have for understanding reality.

Nature follows scaling laws. Human systems follow them. Cities, infrastructure networks, communication networks, even the statistical patterns of wars follow them.

You don't challenge scale-invariant arguments with superficial objections — especially when those objections have already been addressed by well-understood properties of scaling itself.

All the arguments Luke offers fall into this category.

I’ve explained repeatedly why they fail:

– Bitcoin adoption behaves like other networks

– market capture in network systems is a nonlinear process

– adoption and market cap do not scale linearly

– scaling laws describe the ensemble behavior of a complex system, not anecdotal deviations

There is nothing in Luke’s pseudo-arguments that comes close to challenging a well-established, deeply grounded scaling framework.

Of course, any scientific hypothesis can be invalidated.

But the only way to test the power-law hypothesis is empirically, through data and the evolution of the system — not through opinion, not through personal intuition, and certainly not through misunderstandings of basic scaling behavior.

In the end, reality will choose the correct hypothesis.

We will see it clearly in how Bitcoin evolves.

English

TriNguyen.x retweetledi

OK, here's my damn critique (or part of it) of the viral @profplum99 essay advocating for a <checks notes> $140,000 poverty line

Pull quote: "It is…The Worst Poverty Analysis I Have Ever Seen. (And I’ve read Matthew Desmond!)"

Also very happy with that Dorothea Lange-style image

English