Vivosa Research

1.3K posts

Vivosa Research

@Vivosa_

Arbitrageur, skeptic. Class of 2009. 1000x or bust many times.

Katılım Şubat 2009

755 Takip Edilen194 Takipçiler

@BickerinBrattle How long out are you going as couldn't this take a while as in end '28

English

for the record I started the one put rules them all OTM strategy for all the wealth I thought I could do without in 20 years in August 2025 at around 6200. In Jan 2025 shorted as Trump made it clear he was going for a coup (unitary executive) and was a thief, went long in April 2025 as thought SCOTUS was kicking in. when SCOTUS hid behind "percolation" started short in August 2025. in terms of % of available net worth - it is all my own money now - this is largest loss have experienced in last 40 years. but note that "40 years" FWIW.

I am long OTM puts in WFC as anticipate a near collapse in the US financial structure worse than 2008 and now there isnt a single agency empowered as all were in 2008. and the fiscal will have Trump in impeachment proceedings. so......

English

Vivosa Research retweetledi

Not conforming to early morning types schedules and then wildly outperforming is a top 5 feeling.

English

@HowardSmith_Jr @RMathis77 @BitcoinMagazine @TheBitcoinConf @SteaknShake Not everyone knows things. People turn down raises to save on taxes too. Lol

English

@RMathis77 @BitcoinMagazine @TheBitcoinConf @SteaknShake You know that just means they don’t pay tax on the $1,000,000, it still cost them $1,000,000……

English

JUST IN: Fast food giant Steak 'n Shake announces "when we use bitcoin, we save 50% on processing fees vs a traditional credit card user." 👀

"If every credit card user used bitcoin, we would save roughly $6 million annually. Which is huge" 🙌

English

🚨 WARNING (AGAIN)

DPRK threat actors are still rekting way too many of you via their fake Zoom / fake Teams meets.

They're taking over your Telegrams -> using them to rekt all your friends.

They've stolen over $300m via this method already.

Read this. Stop the cycle. 🙏

English

I started by trying to understand markets. Thirty years later I've ended up somewhere closer to life, the universe and everything. The same four rules keep showing up...

Along the way I've written three frameworks that have shaped how a lot of people see the world.

The Everything Code is what I found when I went looking for what actually drives markets. A debt rollover cycle, managed by liquidity, debasing the currency at roughly 8% a year. That debasement is monetary entropy. Capital routes around it, into whatever can compound faster than the entropy degrades it. Technology and crypto sit at the top of that flow because they are the intelligence layer of the economy. Markets are monetary energy routing toward the highest output of intelligence. The only assets that outperform debasement over extended periods are tech and crypto.

The Exponential Age is the realisation that technology has become the substrate. Compute, networks, energy and intelligence are compounding faster than any institution we built was designed to handle, and the gap between the two is the defining tension of our time.

The Economic Singularity is where this is heading. Somewhere in the next decade the curve of intelligence per unit of energy turns fully exponential, and the rules every economy we know was built on stop applying.

For a long time I thought of these as three separate ideas. Looking at them now, they are three views of the same thing at different altitudes. And underneath all three, the same four rules keep showing up.

Efficiency of Intelligence - The universe rewards whatever does more with less. Every system that survives is better at turning energy into information than the system it replaced. There has never been an exception.

Compression - Intelligence is the act of representing a vast reality in a much smaller form without losing what matters. Brains do it. Theories do it. Prices do it. AI does it. They are not analogous. They are the same operation.

Coherence - Complex systems hold together because their parts synchronise faster than the noise around them. Markets, brains, civilisations, ecosystems. When the synchronisation fails, what looks like collapse is desynchronisation made visible.

Selection - Patterns that copy themselves faster than their rivals dominate the medium they live in. Genes did this in biology. Ideas do it in culture. Memecoins do it in markets. Truth is not part of the selection criteria. Replication is. It always has been.

What the four rules produce, when they operate together, is networks.

The same topology shows up everywhere. The cosmic web. The human brain. Mycelium beneath a forest. The internet. Financial markets. Blockchains. Across fourteen orders of magnitude, the universe keeps building the same shape. That shape is what the four laws look like when you can see them.

The Everything Code is what these four rules look like in markets.

The Exponential Age is what they look like running through technology.

The Economic Singularity is where they are taking us.

Three angles, one picture.

Underneath all of it, energy is the constant. Consciousness is the substrate. The four rules are the dynamics through which one becomes the other.

All of this is one corner of what I call The Universal Code. The same four rules apply to everything else and I mean EVERYTHING... they are universal in the true sense of the word.

English

@RaoulGMI You didn’t mention bananas mate? What about the making up to total crap to sell subscriptions? Where’s that part?

English

@Craigstox @jakebrowatzke With his Elon bucks from our engagement lol

English

@jakebrowatzke Buying? With what money? It's time to get a job.

English

Notably, only one historical instance combined a 2.85%+ SPX rally with a 5point VIX drop that crossed from above 30 to below 30, the same configuration seen yesterday.

That occurred on May 10, 2010.

This historical parallel aligns with my expectation for SPX to retrace toward the 580-600 range during April.

Ben Kizemchuk@BenKizemchuk

SPX rallied 2.9% today. This marks the first time in 90 trading days that SPX finished at least 2.85% above the prior close. Historically, these outsized upside shocks have tended to precede higher volatility rather than sustained momentum. Looking back to 2006, similar occurrences have generally been followed by choppier price action and weaker risk‑adjusted returns over the subsequent one to two weeks. What stands out in the data: 1) Near term returns skew negative. Average performance is negative across every horizon from 1 to 10 days, indicating poor follow through after the initial surge. 2) Weakness tends to deepen with time. Drawdowns are modest early but deteriorate meaningfully after Day 4, with the Days 6-8 window showing the worst combination of win rate and average return. 3) Volatility increases with a lag. The largest downside outcomes do not occur immediately; historical worst‑cases widen from single digit declines early on to roughly ‑20% or more within two weeks. 4) Upside tails are narrow. Strong positive follow through beyond one week is rare and largely driven by a single historical episode. 5) Even at horizons where outcomes are positive roughly 50% of the time, average returns remain firmly negative, implying losses have historically outweighed gains. Bottom line: Large upside shock days have tended to mark inflection points within downtrends rather than new trend accelerations. Price action becomes choppier and risk skews to the downside. History argues for expecting higher volatility and poorer risk-adjusted returns, not a smooth continuation higher.

English

@zerocooltrader @RyanDetrick 250+. That's why all these market backtests also need to be mentally backtested.

English

@RyanDetrick While I find this fascinating, 11 samples is far from statistical significance. Do not you need at least 30?

English

Could the S&P 500 go down 20%?

Anything is possible, but looking at the other 11 bear markets since the S&P 500 became 500 stocks shows that they usually start with a quick drop from ATHs.

In fact, down 5% in only 14.5 days on avg those times.

The recent 5% mild pullback took a very long 35 trading days, which would by far be the most ever should this turn into a bear market.

Shoutout to the OG @StovallCFRA for pointing this out today.

English

$RGTZ, $PLTZ, $SBIT, $TSLQ n'chill market (and collect 50% short interest monthly)

English

What a rug pull in $VCX.

It was a popular way to get exposure to names like Anthropic, Databricks, OpenAI, Anduril & SpaceX but after running 10x in a week and trading around 25x NAV… it was a very obvious short.

English

@JeetenX @amitisinvesting No it’s roughly 25% of the company’s market cap. They invested $100M into Anthropic at a $5B valuation

English

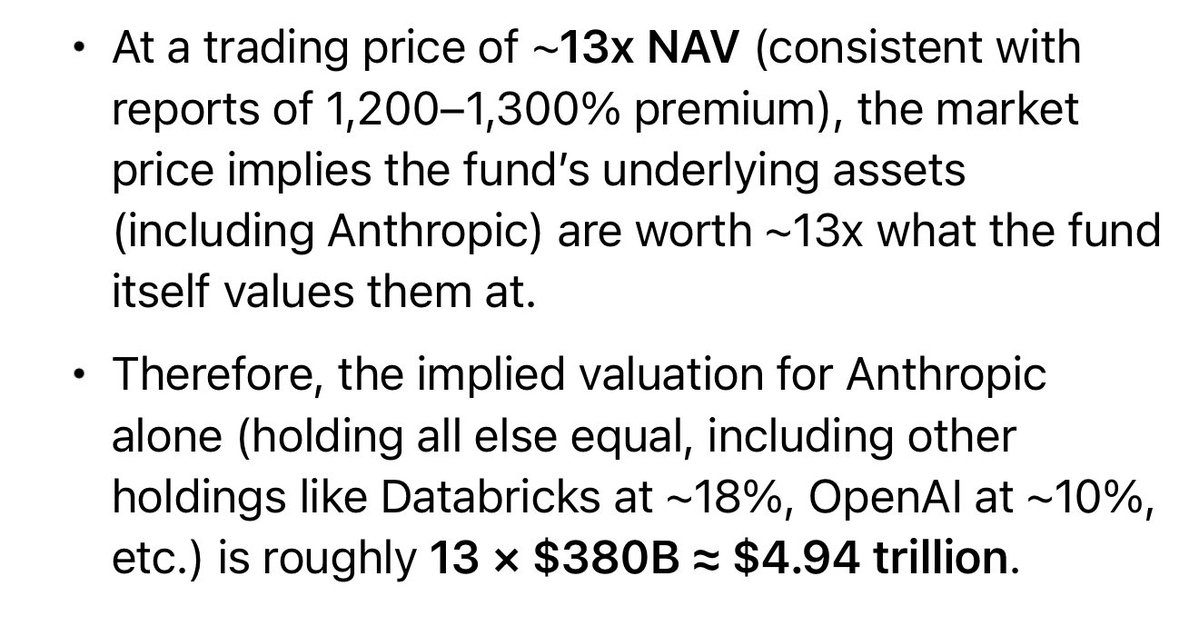

So people are buying this fund $VCX at these levels to buy Anthropic at a $4.94T valuation…the reported secondaries are going for $600B.

I get that people want exposure to these private names but you can buy $AMZN, a real business, and get 15% exposure to Anthropic…

Sam Badawi@Sam_Badawi

$VCX fund that includes 20% of Anthropic, 18% of Databricks, Anduril, and OpenAI is up over 300% in a month. Trading has been halted today! Crazy!

English

Vivosa Research retweetledi

Caleb Hammer reveals his biggest money mistake was buying rental properties instead of investing in the market

“I made decent money, but I would have made so much more money by just being in the market instead of focusing on that. My rental properties back in my home state, I am fully exiting them and just putting the money in the market.”

English

@Pete_Exo @Polymarket Because a person isn't a corporation that has access to the same financial strategies you dipshit. If a poor person loses $2,000 its not the same as a S/C corporation writing off loses.

God you people are retarded.

English

JUST IN: Meta announces they'll be shutting down the Metaverse, after pouring $80,000,000,000.00 into the project.

English

@antoinpreaubert @Polymarket Better than most crypto investments

English

@SystematicPeter Actually systematic requires more screen watching (especially worried for your algod to trip up somehow) than discretionary if you use your brain. Also much lower roi.

English

I’ve been trading for ~30 years.

First half: fully discretionary, living inside futures microstructure. It worked—until algos started exploiting the same patterns and reacting in microseconds. Edge decay was real.

So ~10 years ago I switched to systematic.

Now I run many uncorrelated strategies in parallel without babysitting screens all day. I wouldn’t go back.

My biggest unlock: reusability of know‐how.

When I finish a new system, I plug it into a ready workflow in minutes. It monitors itself; I move my brain to the next big thing.

Here’s the playbook I wish I had from day one:

- Framework (design once → reuse forever)

- Data → clean, feature, label.

- Hypothesis → simple, testable edges (breakouts, momentum, mean reversion).

- Validation → IS/OOS, realistic costs/slippage.

- Risk → position sizing, max heat, portfolio exposure caps.

- Deploy → automated orders, fail‐safes.

- Monitor → health dashboards, kill‐switch rules, mobile app.

- Iterate → new systems slot into the same pipeline.

Principles that compound:

- Many small, independent edges > one “genius” setup.

- Process beats prediction.

- Shipping beats perfecting.

Discretionary taught me markets. Systems gave me scale.

English

@Wolf_Dreams7 What about jogging with stroller? I'm not sure I could function without 20 minutes of sweating most/all days

English

My wife and I have ~40 free hours a week or so where we are not taking care of our one (1) child. Those hours are spent on W2 work / school work errands, chores, etc. We have no time or energy to exercise anymore. Just the 15 minute walk to and from the train station a couple of times a week.

English