Sabitlenmiş Tweet

Von Mises

2.2K posts

Von Mises

@VonMisesCapital

Inner circle insights on: Digital Assets | Institutional Investing | AI

Katılım Şubat 2022

273 Takip Edilen162 Takipçiler

Shipping in the Strait of Hormuz has hit its highest level since the crisis started.

When the UAE acts… the world’s lifeline moves.

The UAE: a resolute power protecting global maritime routes and economic stability.

English

@LeadingEdgeTLE @qualtrim I will definitely look into this man, thanks for the heads up

English

@VonMisesCapital @qualtrim SBC. If you remove it from the COGS, then the adjusted PE is closer to 30x.

Not saying this is the right thing to do, just giving perspective. FCF multiple is a better earnings measure IMO.

English

@BramVGenechten Great observation Bram 🤝

Even more absurd valuation stats below 😅

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

And the numbers begin to whisper something unusual: ~ 75% gross margins. ~ 93% ROIC. This is not a business — it’s a tollbooth on the future. Despite increasing 1376% since October 2022, $NVDA’s P/E has barely moved (~35x).

English

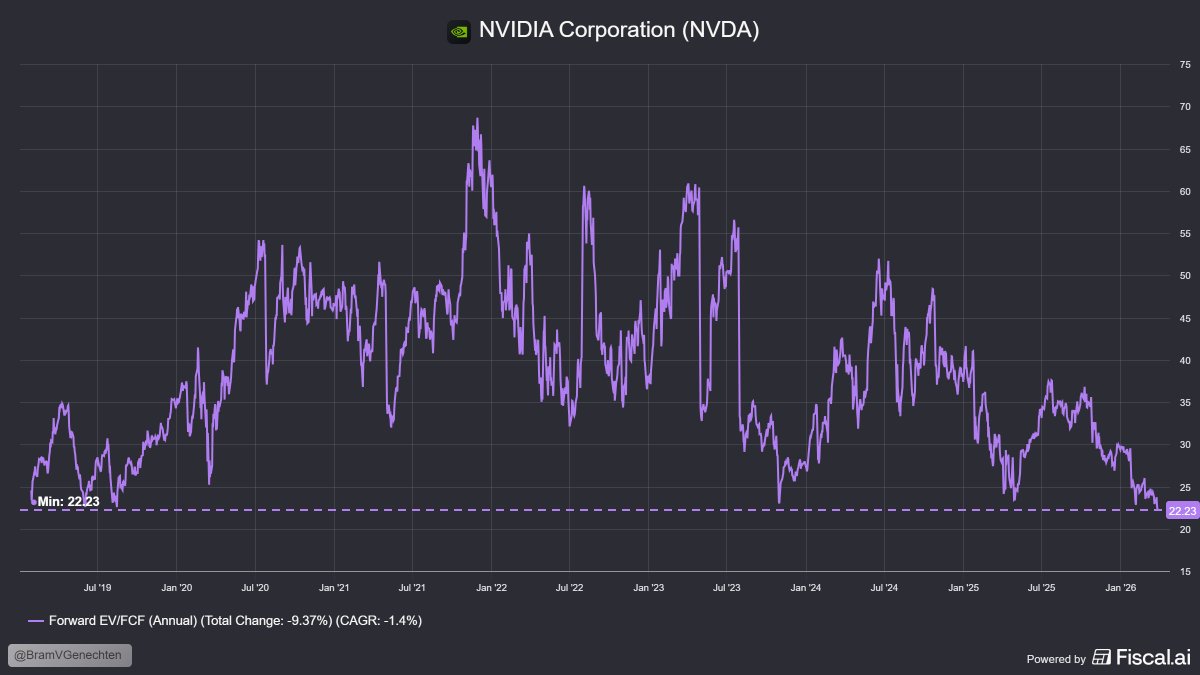

Nvidia at its lowest valuation in +7 years.

Expected FCF growth:

87% (Jan '27)

29% (Jan '28)

23% (Jan '29)

$NVDA

English

@Ashton_1nvests Consider adding this mag7 name as well 👇

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

In a crowd mesmerised by AI… Don’t just follow where billions are spent — watch who doesn’t need to spend them. While the Mag 7 drowns in capex, one name compounds quietly. Here's why it's a generational buy — a safe harbour, not a risk asset. 🧵

English

My top 4 stock picks that I believe will carry my portfolio to $100,000+:

- $SOFI

- $AMD

- $AMZN

- $ZETA

Each one plays a different role, but they all have one thing in common… growth.

$SOFI is my highest conviction.

A one-stop financial ecosystem that’s still early, with strong member growth and expanding margins.

$AMD is my AI bet.

They don’t need to beat NVIDIA to win. The market is big enough, and they’re gaining real traction.

$AMZN is my anchor.

Consistent growth, multiple business segments, and one of the best long-term compounders in the market.

$ZETA is my asymmetric upside play.

High growth, strong data advantage, and still massively overlooked by most investors.

I’m not trying to overcomplicate things.

Just owning great businesses, staying consistent, and letting time do the work.

That’s the plan.

English

$PYPL

Price is still at $44, where it was in 2017

Revenue was $3 Billion then

Revenue is $8.7 Billion now

What does it need to do to turn this around?

English

@TradexWhisperer "Fully booked before construction has even started"

Truly unprecedented, thanks for sharing this 🤝

English

$TSM TSMC is completely SOLD OUT until 2028 including its cutting-edge 2nm (N2) node. Even its next-gen Arizona fab (targeting ~2030 production) is fully booked before construction has even started. 🔥

AI just broke the fab cycle. The fabs can't keep up.

Trade Whisperer@TradexWhisperer

$TSM has become the de facto semiconductor index. It's now the proxy for the entire semiconductor industry. $2 Trillion Market Cap: Inevitable

English

@_LEAPOptionsCP_ As long as $NVDA's competitive moat in AI chips (and now potentially software in CUDA) remain, it should be a great addition!

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

In a crowd mesmerised by AI… Don’t just follow where billions are spent — watch who doesn’t need to spend them. While the Mag 7 drowns in capex, one name compounds quietly. Here's why it's a generational buy — a safe harbour, not a risk asset. 🧵

English

The four stocks I’m never selling

1. $NBIS

2. $SoFi

3. $GOOG

4. $AMZN

What am I missing ?

English

@dividendology I’m allocating disproportionately into this Mag 7 name 👇

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

In a crowd mesmerised by AI… Don’t just follow where billions are spent — watch who doesn’t need to spend them. While the Mag 7 drowns in capex, one name compounds quietly. Here's why it's a generational buy — a safe harbour, not a risk asset. 🧵

English

Community contribution time.

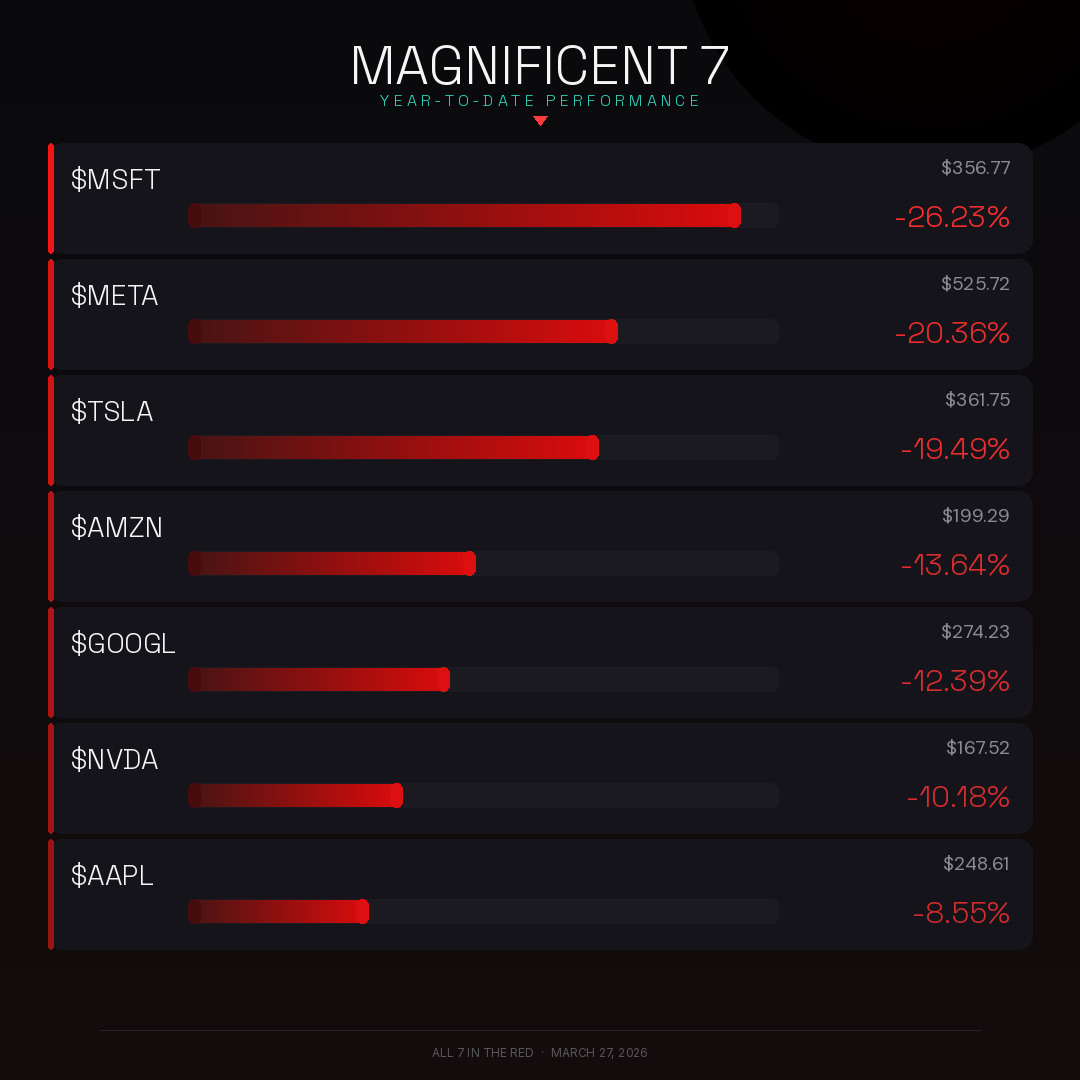

Give me your new name for the MAG7 stocks based on their 2026 performance 👇

English

@InvestingVisual My hunch is that $NOW is a far more competitive business then the over-hyped $ZETA.

Will be analyzing this more on my page.

English

Servicenow is $NOW trading at their lowest valuation ever since becoming free cash flow positive.

English

@MarketMatrixs $NVDA is not overvalued, esp given its competitive moat and capital efficiencies.

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

In a crowd mesmerised by AI… Don’t just follow where billions are spent — watch who doesn’t need to spend them. While the Mag 7 drowns in capex, one name compounds quietly. Here's why it's a generational buy — a safe harbour, not a risk asset. 🧵

English

$NVDA is overvalued

$MU is overvalued

$HIMS is overvalued

$OSCR is overvalued

$SOFI is overvalued

$ZETA is overvalued

$PLTR is undervalued

$ORCL is undervalued

$CRWD is undervalued

$TSLA is undervalued

😉

English

@MarketMatrixs $MU is certainly not overvalued.

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

$MU just dropped a monster quarter… One of the most explosive in semiconductor history. +38.57% earnings beat. +22.25% EPS beat. Yet this barely looks like the peak... But a new beginning towards even greater highs. 🧵

English

@ndxtrader9 @DrJStrategy I'm not sure if Trump is truly owned by the Zionist lobby if his strategic objectives during the Iran war consistently diverge from Israel's.

Further, it seems that he is more concerned about securing the security of his gulf allies rather than Israel.

English

@DrJStrategy Blah blah blah.

That's all I hear from trump supporters is that "this is about China!!!"

No. It's about Trump being owned by the zionist lobby and doing exactly what his political donors tell him

English

Trump’s confrontation with Iran is the visible crisis, but the real contest is with China. This is the new Great Game: using Gulf conflict to squeeze Beijing’s energy lifelines and redesign its growth model. Yes, it’s a Hegelian dialectic of conflict, contradiction, and higher‑order strategy.

Wellington-Altus@wellingtonaltus

The New Great Game is taking shape—a U.S.-China rivalry over energy, AI infrastructure, and the dollar. In his April #MarketInsights, @DrJStrategy weighs in on Bretton Woods 2.0, King Dollar, and what it means for investors: ow.ly/FJoQ50YBbHh #Investing

English

Peter Thiel: “AI chips will get commoditized.”

Yes, the value in AI has largely accrued to the semiconductor level so far amd concentrated largely in $NVDA.

But this is bound to change.

In chips, you can stay as a monopoly only if you have an exclusive partnership with the monopoly in a downstream market.

This is how $INTC dominated CPUs for decades, by partnering up with $MSFT.

We can’t see such a partnership in AI, industry dynamics don’t allow it:

- Downstream market is fragmented.

- Price/performance drives decisions.

As a result, the more AI workloads shift to inference, the more fragmented the AI accelerator market will become as inference-specific chips or custom chips of hyperscalers will be used more.

Yes, it looks like most of the value has accrued to $NVDA right now but it’s almost certainly not sustainable.

This is why I don’t own it despite seemingly attractive valuation.

Its base is already too high and it’ll certainly struggle to maintain it let alone grow.

Apoorv Agrawal@apoorv03

Two years ago I broke down the economics of the AI stack. The semi layer captured 87% of all profits. The app layer captured 3%. Two years and $350B revenue growth later, the shape barely changed. Semi: 79% of profits (was 87%) Infra: 14% (was 10%) Apps: 7% (was 3%) And concentrated! Semis is a one-player game. Apps two-player. Infra is the only competitive layer. The most profitable company in AI is still the one selling the shovels. x.com/apoorv03/statu…

English

@codetocompound @oguzerkan Can't agree more, $NVDA still dominates 92% of the discrete GPU market 👇

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

Then there’s $NVDA… With just $6B in capex. Yet it owns ~92% of the discrete GPU market — the very intelligence capex is chasing.

English

@oguzerkan Peter Thiel is probably right long term, AI chips will fragment, but right now NVIDIA still owns the stack and developer ecosystem.

Commoditization isn’t overnight, erosion will be gradual, not sudden.

English

@oguzerkan Well-constructed bear case that deserves serious analysis.

But an angle to consider is how $NVDA durable competitive advantage is increasingly software (in its CUDA ecosystem), not silicon.

Its capital effeciency further cements the bullish thesis 👇

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

In a crowd mesmerised by AI… Don’t just follow where billions are spent — watch who doesn’t need to spend them. While the Mag 7 drowns in capex, one name compounds quietly. Here's why it's a generational buy — a safe harbour, not a risk asset. 🧵

English

@FinnStockinger @aleabitoreddit Thanks for this nuanced insight.

But it's still true that $IREN's shareholders have been aggressively diluted since 2024, with shares outstanding more than doubling.

Here are my thoughts on another AI company which might present a safer option 👇

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

In a crowd mesmerised by AI… Don’t just follow where billions are spent — watch who doesn’t need to spend them. While the Mag 7 drowns in capex, one name compounds quietly. Here's why it's a generational buy — a safe harbour, not a risk asset. 🧵

English

You’re fundamentally misunderstanding how an ATM offering actually functions.

Announcing a $6B facility isn’t immediate dilution; it’s a tool for capital flexibility that allows a company to sell shares in small batches exactly when they announce massive catalysts.

If $IREN uses $6B of an ATM to lock in a contract generating $40B in ARR from their secured power, that’s not a "burden" - it’s incredibly efficient capital allocation.

Posts like this are damaging your credibility.

English

Do you guys think there’s only $5,650,000,000 dilution to go with $IREN?

Very surprising that people haven’t switched to $NBIS or other names if you’re long Neoclouds.

One already has confirmed funding with $NVDA + convertibles from institutions.

The other is likely actively selling new shares on the open market to get funding off retail shareholders.

The sad reality is:

$IREN simply cannot monetize the rest of their capacity without using that. It’s not “optionality”.

Financial structure nuance matters when you’re choosing winners for equity appreciation.

Nebius is clearly has the better financing structure and this is already showing up in YTD returns.

Serenity@aleabitoreddit

$IREN filed to dilute $6,000,000,000 at a $11.7B MC. That is not noise. This is Iren's way to monetize their 4.5GW capacity by selling all those new shares onto the open market. If you want some history on how this turns out: Look at $BKKT that crashed 99% with Mike and $IREN board of directors history with excessive ATMs. Or his recent company $ASST. It’s accretive to the company and executives: Because it wipes out all retail shareholders and they can always issue SBC. So they don’t actually care what stock price it needs to be at to sell. After they’re finished, they have $6B in new cash to use for scaling without paying interest. But the reason why convertible notes with interest, and $NVDA funding balance sheets is much better for retail capital: Is because it doesn’t wipe out retail equity to achieve this. Because at this point $IREN looks like the $AMC of datacenters with a dwindling moat, and looming $6B in shares sold into the open market. Reason I post about $IREN is because - people dismiss a $6B ATM as “Noise” - it’s one of the most popular retail “buy the dip” companies that they’re buying into a $6B dilution machine - people still don’t understand the risk at all. - the amount they have now is not enough to finance GPUs/GW capacity monetization. - they likely will have to use the ATM, it’s not “optionality” Again: I have zero positions in the company. I’m just warning retail investors that this ATM structurally wipes out your equity appreciation by how structural mechanics of $6B+ ATMs work. Because $IREN likely needs to sell new shares at any price to monetize their GW, otherwise there would be zero need to file it. Executives actually don't need to care because they can make up for stock price dropping by issuing SBC like $SNAP. If you have to wonder if your equity gets wiped out from an excessive ATM: There are better longs out there than $IREN.

English

@aleabitoreddit As straightforward as it sounds, there are many other (safer) AI monopolies to rotate into 👇

x.com/VonMisesCapita…

Von Mises@VonMisesCapital

In a crowd mesmerised by AI… Don’t just follow where billions are spent — watch who doesn’t need to spend them. While the Mag 7 drowns in capex, one name compounds quietly. Here's why it's a generational buy — a safe harbour, not a risk asset. 🧵

English