Sabitlenmiş Tweet

Most investors approach critical minerals the wrong way. They focus on the resource. The returns don't come from the rock.

English

William David

81 posts

@WDChokepoint

Research at the intersection of supply chains, energy, and defense. Writing at The Chokepoint on Substack.

The US government just published a report explaining why its own critical minerals strategy doesn't work. The problem isn't mining. It's: — Prices set below break-even — Subsidies that expire before projects do — Regulations stricter than background radiation — A workforce that doesn't exist yet Most investors haven't read it. They should. williamdavid.substack.com/p/the-governme…

This is my sixth conversation with @GavinSBaker. As always with Gavin, the conversation covers a lot of ground, but we spend the most time on watts and wafers. We discuss: - Why the wafer shortage may prevent an AI bubble - Data centers in space (reframed) - Elon's Terafab and the new chip companies challenging Nvidia - Usage-based pricing - The disaggregation of GPUs - DRAM, frontier tokens, and open source Enjoy! Timestamps: 0:00 Intro 7:55 Anthropic and OpenAI Valuations 12:58 Watts, Wafers, and Infrastructure 14:39 Orbital Compute and Data Centers in Space 22:49 Avoiding the AI Bubble 28:26 Terafab and the Future of US Manufacturing 32:16 Returns to the Frontier 37:23 Continual Learning 42:03 New Chip Companies 48:52 Extending GPU Lifespans and Private Credit 51:22 The Application Layer 57:32 The Token Path and Open-Source Dynamics 1:01:37 Cybersecurity 1:05:46 Diversity Breakdown 1:11:59 Assessing the Big Tech Players in AI 1:19:02 Geopolitics, Personal Safety, and the AI Horizon

Nuclear energy is essential to unleashing American energy dominance. And SMRs are one of the critical sources we need to meet demand. This news by the DOE ensures that America will be able to scale SMR construction faster and more efficiently.

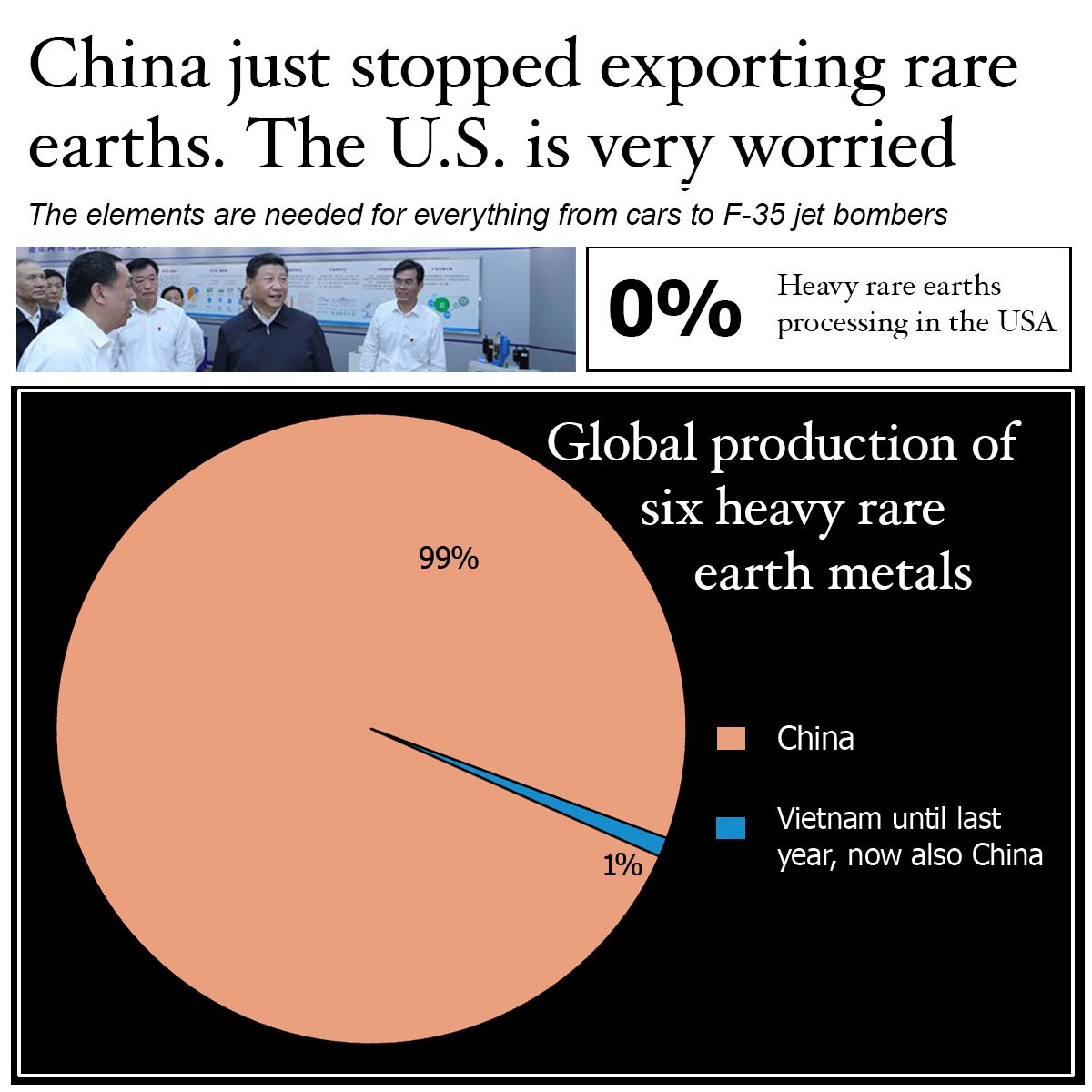

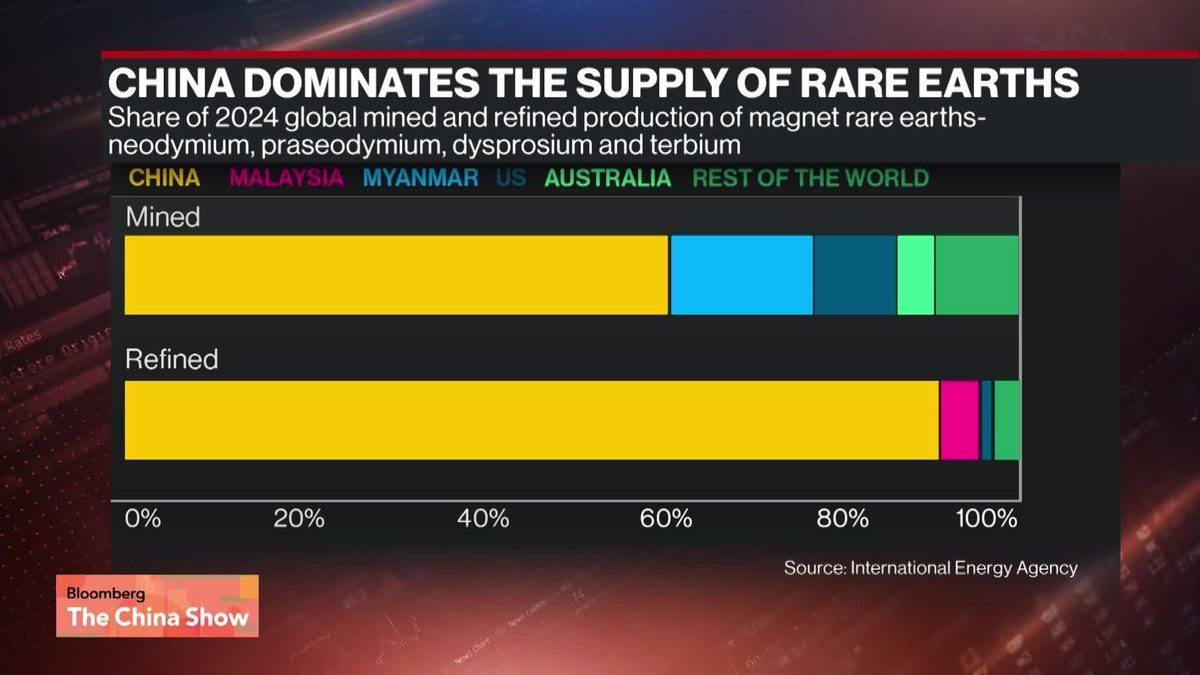

Defense Groups are Panicking About the Chinese Jan 1st 2027 Magnet Ban $MP $USAR $ALOY $AREC Defense companies are pushing Washington to delay a deadline, years in the making and now just months away, banning them from sourcing rare earth magnets from China for the US military. Some defense groups want more time to comply with the prohibition on using Chinese samarium cobalt magnets and neodymium iron boron magnets for defence department contracts from January 1, according to four people familiar with the matter. “Unless significantly more capacity comes online, adhering to the 2027 ban may not be feasible.” ft.com/content/4d6651…

DOD's director of Golden Dome missile defense shield pushes back on CBO's $1.2T program price estimate w a familiar refrain - in short, "they’re not estimating what I’m building." He said the same thing when asked about other cost estimates in March. punchbowl.news/article/defens…