Yuri

983 posts

@mbrown_co Great counterpoint!

But I want to note that introspection and talk therapy are two separate things. Introspection is critical and talk therapy is one form of introspection.

I've done 20,000 hours of introspection but zero in therapy.

English

The past week was a masterclass on how bad ideas spread.

It started with one bad take by someone who is world-class in their domain and out of their depth on the subject at hand.

The now mega-viral clip of Marc Andreessen saying he's not introspective starts the way all bad ideas do: with a kernel of truth.

Yes, talk therapy can be a circle jerk.

But the same can be true of exercise.

Let me show you what I mean:

The American College of Sports Medicine, the gold standard in exercise science, recommends a minimum of 20 minutes of vigorous activity three times a week.

That's not going to get anyone far fast.

But anyone who is decently fit knows that. If you've been to a gym, you know that's baseline advice for the sedentary to start somewhere.

Same with talk therapy. People who have never been to therapy think it's just lying around wallowing in your problems. And in some cases, it might be.

But almost no serious practitioner is doing vanilla "talk therapy" at this point. More modern methods like CBT, EMDR, IFS, and somatic experiencing are all way more effective.

It turns out, we've gotten better in the last hundred years.

And when Andreessen called introspection a 'guilt-based whammy manufactured in Vienna in the 1910s,' well, so was exercise. Just like therapy, it didn't exist in the 19th century.

But this is more than just a bad take.

It's potentially harmful.

First, it could keep someone who desperately needs it from seeking help.

But more insidiously, it validates every founder who is running from their underlying wounds, trying desperately to achieve their way to enoughness.

It's permission from someone who is running to give others permission to keep running. To keep grinding away in the name of greatness.

And then, suddenly, everyone has a take. This is how bad ideas spread. One person with a massive platform says something wrong with confidence, and an entire ecosystem of influencers repeats it because alignment with the highest-status take in the room is easier than forming an original thought.

Which brings us to the bandwagon take: "Talk therapy is a waste of time."

Is this from experience? Because I don't know a single person who sought out a vetted, qualified therapist, engaged honestly with the process, and came away saying it was a complete waste of time.

More likely, this is a blanket dismissal of an idea of what therapy is, rather than an experiential critique. Which makes it a strawman.

It's an intellectually lazy way to borrow credibility by taking cheap shots at a caricaturized version of something that the person has never actually done.

And then, in perhaps the most damning moment of the whole cringeworthy clip, the appeal to authority by claiming that the great men of history didn't need introspection.

But who exactly are we considering to be a "great man?"

J. Paul Getty? Steve Jobs? Elon?

You want to build a dynasty at the price of those closest to you?

Be my guest. This is the recipe.

I'll never have as much money as Andreessen.

But I'm wealthy in the ways that actually matter.

I've healed myself. I've excavated my psyche. I've challenged every inherited belief and chosen my own values.

There was a time when this might have resonated with me, too.

Before I took the first step.

Before I dared to look behind the curtain as to why I was white-knuckling my way through life, and it still wasn't enough.

But I've always been a truth seeker.

And when the cracks started to show, the whole scaffolding came crashing down.

And as a result, I have my own hot take:

Being introspective is the single most important quality to a life well lived.

Codie Sanchez@Codie_Sanchez

I'm pretty convinced talk therapy is a complete waste of time.

English

@NikLentz @BobEUnlimited You can stake your money if you like the odds. Or smdy else can, thats makes them somewhat efficient

English

@BobEUnlimited Do you think prediction markets actually predict anything? That would surprise me.

Personally, I think these betting odds have no real statistical value, but I’d be interested in how you think about it.

English

Are Markets Underpricing Conflict Tail Risk?

If the conflict extends to the summer, the global economy will face sharply higher oil prices. Financial market pricing remains pretty sanguine even as prediction markets show 40% odds we get there.

bobeunlimited.substack.com/p/are-markets-…

English

@AgustinLebron3 Obviously a commonality amongst traders that VCs are clueless about betting (cf blog.moontower.ai/the-arbitrage-…). Despite this we haven't seen ex-traders segue into VC and crush, at least not at the frequency the above attitude might imply. Just not enough crossover in core competencies?

English

VCs and investors really need to understand public financial markets, trading, etc a *lot* better than they do.

Having done "Quant Trading 101" for a few tier 1 VC partners over the years, including one recently, I've gotten decent at finding the holes in their understanding.

English

I often think about the technical limitations that game designers of the 80s had to work with - both in terms of software and hardware.

The game that stands at the very top is Elite.

Think about this for a second: The core game code on the BBC Micro version occupied roughly 22 KB of memory. Now think about what Braben and Bell turned that into: a universe with eight galaxies, each containing 256 star systems (for a total of 2,048 planets/systems). Each system featured unique details: government type, economy, technology level, population, commodity prices, and even descriptive text (e.g., a planet known for "carnivorous arts graduates" or similar quirky combinations).

If you still need a bit more help to contextualize that, try this: Elite was smaller than many modern text files or desktop icons, yet it contained (and let you freely explore) a multi-galaxy-spanning universe that felt vast and limitless.

Oh, and by the way, the game also rendered 3D wireframe ships, stations, and planets in real time on a 2 MHz 6502 processor.

This is no slight on today’s game designers. They work with what they have, and that's okay. But when you think about the worlds that some programmers created with the tools they were given, it sometimes breaks my brain trying to understand how they did it.

Elite is a true masterpiece on so many levels. I played the C64 version back in the day, and even 40+ years later it still feels like one of the most incredible programming wonders ever.

English

@Richard_Casey Why would Iran attack Europe if they are not in war? Russia has more rockets and nukes and is much closer to Europe

English

Thursday: 'Not our war' Europe says no to Trump

Saturday: 'Not our war' Spain(ex-Catalonia), Portugal and Ireland say no to Trump

English

@MrMojoRisinX Very good note. Implementing it requires a lot of experience and work

English

I don't really see a lot on FinX offering advice or even a discussion of hedging, portfolio construction and risk management approaches. However, I do see a lot of renting single name idea conviction, and then hating on anyone who disagrees with pushback or looking at the idea through a different lens re factors, how does it fit into a portfolio, etc. Then the pile-on begins...and one losing idea out of fifty gets quoted like it defines the whole body of work. Nobody really asks about that position and how it is sized or fits into someone's portfolio or what the mandate is... Nobody really asks about trade structures and/or about the hedge. Let's dig in...

Hedge the Damn Book. Or At Least Your Most Convicted Positions.

People love to say they don't need to hedge.

"The valuation is too compelling." "I'm a long-term investor." "Tail hedges never work." "I will just buy more."

Fine. Keep telling yourself that while you watch six months of alpha evaporate in three weeks because you were too proud, or too lazy, to protect the book or a large sector concentration.

Here's what nobody tells you: hedging isn't one thing. It's a toolkit. And most people have only ever picked up one tool, and they aren't even really consistent in its use.

The hedge book budget. Start here:

Before anything else, you need a philosophy. Mine is simple: I start every year already down. Whatever the hedge book costs me — call it 1.25-1.5% of NAV (lotta variables to consider here to come up with this figure range re net/gross/'n'/bull-bear beta/etc). I'm not trying to predict when the correction comes with this approach, but I am buying the right to not care when it does. [Let me know in the comments, how you hedge or have questions on how to think about establishing a hedge book budget for your portfolio.]

That budget gets deployed across structures depending on where vol is. Down 5/20 put spreads when skew is rich and I can finance cheaply. Down 10% outright puts when I just want clean delta. Down 30% puts sitting on the shelf quietly when vol is at the floor and the market is pricing perfection.

And here's the discipline part: I'm not married to any single strike or expiry. I'm looking at the vol surface. Is there skew I can exploit? Can I do a 1x2 put spread and get the structure for near zero? Can I collar a concentrated position and use the premium to buy something else? The market tells you where the cheap protection is. You just have to look. [I have a tool for this that I have used, and make tweaks to for 20+ years.]

The other piece: which index actually correlates to your book? Running a small cap value book and hedging with SPY doesn't make a lot of sense... Know your beta. IWM, QQQ, or even sector ETFs might actually move when your book moves.

Portfolio-level hedges: the game theory of net exposure:

If you're running 150-200% gross with 30-40% net long, your hedge book has a job to do. It's not just protecting downside, you are managing the delta of your portfolio dynamically. As the book rallies and gross goes higher, you need to consider a systematic way to adjust as well as some improv. [Separately, if you manage a fund structure and/or have rebalancing, this is an additional consideration.]

Think about this through the lens of scenarios, and unless you have a track record to back it up, I would tone down the predictions. What does my book do if SPY goes down 10% in a straight line over two weeks? What does it do if vol spikes 30% overnight from some exogenous shock nobody saw coming? What if software sells off 15% and small cap industrials rip?

These are stress tests that are pretty easy to simulate. (I run 6 scenarios that are particular to how I manage dough, but I think 4 core simulations should work for most people with an error factor embedded). Net/net, your hedge book needs to absorb some of that damage before it hits the P&L.

Position-level: risk of loss hedges (I don't think I have ever seen this really discussed outside of my feed on Twit)

This is where I see in lights, ego kills people, and you know who you are...well, candidly, you prob don't!

"The risk/reward is down 2 to make 15. I don't need to hedge it."

So the entire market — every sell-side analyst, every long/short fund, every quant model — has mispriced this thing, and you figured it out. Got it. With a snapshot multiple and a management team you've met a few times and IR guy who calls you back the same day.

The way I see it is this: If the upside is that good, buying a down 15% put (this is just an example) on the position costs you almost nothing relative to the expected gain. The most frustrating losses in investing aren't being wrong — they're being right and not being able to hold it because the drawdown got there first or the best the stock could manage over the event path is to recover that downdraft or a bit more, but it never met the up 15 from your investment starting point...now you are extending your duration, thesis has drifted, but you have conviction!

Risk of fraud hedges. The smart money already knows this. (Again, I have never seen this discussed on FinX):

Next time you see a social media account screaming about unusual options flow — 40% OTM puts on MSFT with 5 months to expiry, 50k VIX calls for next month, 100k end-of-year calls on TSLA that are 40% out of the money — stop thinking informed buyer.

Those are center book risk-of-fraud hedges at multi-manager platforms.

When every pod manager in the building is leaning into the same trade, nobody's calling a meeting to discuss the overlapping stock position. The center book just goes out and buys 40,000 contracts of a down 30% put on the crowded long at 25 cents a piece. The "unusual options activity" content creators are selling you a story. Well, the actual story is risk management at the institutional level.

The dirty long basket. Simple, underused, effective:

Some of the cleanest hedging I've seen isn't in derivatives at all. A portfolio manager who identifies the same factors across a dirty basket of highly shorted names — high short interest, similar sector exposures, same macro sensitivities — and runs that basket long against their alpha shorts is doing something most people overlook.

The logic is simple: your alpha shorts are idiosyncratic and hard to hedge individually. The dirty long basket gives you exposure to names that will rip if the market squeezes or rotates, which is exactly when your short book is most at risk. You're not trying to make money on the basket. You're buying yourself time and absorbing the pain that would otherwise force you out of your best short ideas at the worst possible moment.

You can do it in common stock. You can do it in options. Rank-order your universe and consider whether a dirty long basket gives your short book the room it needs to work. I like to use this opportunistically from time to time (like during summer months, where I don't like to have a lot of single name shorts.

Position blocks and the 13F (see Inside the Mind of Mojo):

A lot of institutional books aren't running singles. They're running position bundles, which entails a long position, sector peer short(s), factor neutralizer(s), maybe a correlated derivative. The goal isn't to make money on every leg. The goal is to isolate the alpha from the noise. I call this teasing out the alpha.

Sector books do this constantly. They rank their universe, run factor exposure reports, and surgically neuter the parts they don't want so the only thing left is the stock-specific edge. If you're reading 13Fs and wondering why a manager has a weird combination of longs and shorts in adjacent spaces, that's usually what's happening. The hedge is embedded in the structure.

When funds neuter the entire block via long fulcrum, short the sector, short the factors, et al, the goal is for the position to look on paper (risk mgmt. tear daily tear sheet) like a boxed trade. Long XYZ, short XYZ equivalent. Essentially flat to the market on paper, while the actual expression is the gap between the long and the hedge package.

This is exactly how some of the more reputable activist firms operate, particularly the ones who create their own catalyst inside a defined duration pressure cooker. Market observers see the 13F, watch the stock pop 15% on the disclosure, watch it give it all back, and declare the trade a failure. This framing misses the entire structure. What did the sector comps do over the same period? If the long went up 15% and the shorts barely moved, the manager just added to their shorts after the pop, resetting the box at a better level, now net neutral or even slightly short the sector and layering options on the fulcrum to remove a meaningful chunk of the remaining downside, locking in a sizable gain. The gross P&L on the long looks flat to the outside world, but the actual net P&L on the structure is a different conversation entirely.

Many sophisticated funds go further and use factor tools like Barra to identify and manage specific risk dimensions re momentum, beta, size, short interest, liquidity, growth, yield, management quality. Others work with their prime broker to construct custom baskets that hedge a specific bundle of exposures more precisely than any off-the-shelf ETF can. The custom basket is 'more' surgical but carries its own basis risk. Where you land depends on how much of your gross you can dedicate to the hedge and how much precision the book actually requires.

Prime brokers also offer synthetic structures worth understanding and knowing they exist even if you never use them. These include knock-in/knock-out puts and calls triggered by conditions being met, and conditional parlay structures where the payoff depends on an order of operations. These go in and out of favor, but when sized correctly they can insulate a significant amount of negative gamma in ways that vanilla options can't or at least come up short...

The broader toolkit:

The tools exist for every situation. A few worth naming that don't fit neatly into the categories above:

Volatility as an asset class. Long VIX calls or UVXY as a pure convexity play when vol is cheap. A separate trade from directional index puts, and often a better one when the risk is a sudden spike rather than a grind lower. I am not really a fan of these after spending time with market makers who print money trading this asset class.

Rate hedges. If the book has meaningful exposure to rate-sensitive longs such as utilities, REITs, long duration growth then perhaps treasury futures deserve a look. Rising rates have a way of repricing entire sleeves of a portfolio simultaneously.

FX forwards and options. Hedge your FX, otherwise you are adding another bet to the trade.

Capital structure hedges. Long the convert, short the equity. Or CDS (have written about this before at Inside Mojo) when investment grade spreads are at multi-year tights and the convexity is better than what SPY puts offer. Credit often moves before equity does in stress scenarios, which means you're getting paid before the stock goes down.

Calendar spreads and ratio structures (I have mentioned these trade structures many many times). Cost-reduction mechanics that apply across most of the above. If a structure is too expensive outright, there's usually a way to finance it. If you read my tweets, you know that I love using calendar spreads around defined event paths to get involved in a situation, where when I do this right I come out long equity vs long puts, then I have real built in protection on something the world think is so idiosyncratic a hedge isn't needed.

The toolkit is large. Saying no hedge fits the situation is almost never true (even in appraisal cases, hedges work!). Usually what's missing is the willingness to look and go deeper.

There is no "right way." But there is a starting point.

I know funds that have managed billions for two decades and have never run a meaningful single-name short book. Their edge is finding great businesses and sizing them correctly and risk managing them re if something changes, they hit the eject button (they only buy on the way down if numbers step function still improving and DO NOT ANCHOR TO VALUATION). An alpha short book of single names/themes would just introduce noise to their process and approach. Their hedging is structural, systematic, and for most long-biased equity funds, it's the right answer.

Here are some different approaches / blends that are worth reviewing:

The sector-ETF approach:

The portfolio is organized by sector. Each sector PM or senior analyst has a conviction level, hot or cold, overweight or underweight relative to the index. That conviction maps directly to a net long target for that sleeve, and the hedge instrument is a sector ETF. This approach does require a single PM/risk manager to make some difficult decisions on behalf of the sector PM/sr analyst, re he is going to have to reduce your names from time to time despite your conviction...for the analyst I would learn to not take this personally, and perhaps when you run your own firm one day, you will find what works for you...

Tech is 30% of the S&P and you're running 40% long tech. That's a real overweight. You hedge down to 50% net long using QQQ, IGV, or SMH — whichever actually correlates to the names you own. If a sector is underweighted relative to the benchmark, you might run it near 100% net long because the beta is low enough to live with.

The result: every sector has a net long target that reflects conviction, managed dynamically with index instruments. No single-name short risk bleeding into the long thesis. No analyst ego wrapped up in a short that's moving against them.

This model works at $500mn and it works at $5bn. It matches what most long-biased funds actually tell their LPs they do.

There's a version of this where the CIO reads the macro regime and rotates between ETF hedges and single-name shorts depending on whether correlation or dispersion is the dominant environment. And there's the full single-name short book, pod-style, where analysts rank their entire universe and the shorts come from the bottom of the list, with net exposure calibrated by hit rate, tenure, and slugging percentage — and the central hedge book charged to every PM whether they want it or not, because whoever's name is on the door is responsible for what happens when everything blows up at once. Both are real models. Both have produced long track records. If there's interest in either, drop a comment and I can probably add more color.

One important caveat on scale:

The sector-ETF framework assumes you have enough AUM that return optimization and risk management are the primary objectives. Sub-scale changes the math entirely.

If you're running a smaller fund without a large anchor investor or family office cornerstone giving you runway, the priority isn't risk-adjusted returns. It's marketability. You need returns high enough to get into the conversation with allocators who have minimum AUM thresholds and track record requirements, and you need to get there before you run out of time.

Unless you have a prior track record of short selling that genuinely adds to P&L rather than drags on it, don't force the short book. Have some book-level hedges in place, but lean on risk of loss disciplines on your largest positions — defined stops, position-level risk parameters that save you from yourself — and flex your cash position as a first line of defense. Sometimes the best hedge is just not being fully invested when the conviction isn't there.

Focus hard on N. A concentrated book in your highest-conviction names, sized right, is what generates the return profile that puts you on the map. Over-hedging a sub-scale fund is a slow way to die. And all of this still has to reflect the mandate — which should be an honest expression of what you've actually proven you can do, not what sounds good in an LP deck.

It's all a game. The rules just depend on where you are in the lifecycle.

Before the hedge book: the mandate

None of this works if it doesn't match what you told your investors you do.

The hedging conversation is always downstream of a more important one: what is this fund actually trying to do? What's the investable universe? Where does the edge come from on the long side, and does it transfer to the short side? The funds that drift from their stated process — that say systematic sector hedging and then start freelancing with single-name shorts because the CIO has a feeling — those are the ones getting difficult questions from allocators. Build the hedge book to match the mandate, not the other way around.

Let's discuss and name the excuses:

"Valuation is my hedge." A cheap stock can get cheaper, stay cheap for years, or get cheaper right before it gets taken out at a premium you never got to enjoy because you stopped out first (or perhaps you should have a stop for a portion of the position so you don't bleed).

"The risk/reward is so good I don't need a hedge." The r/r might look exactly right on paper, but if earnings revisions aren't improving, aren't inflecting, aren't showing any rate of change that justifies the multiple you're anchoring to, then the r/r is probably off. Let's just get this out there...variant view is one of the most over-used term in investing. A cheap multiple on deteriorating numbers is just a value trap with better slide deck language. Unless you have a path to buy the entire company, a board seat to drive the change yourself, or an activist position with real leverage over the outcome, you are a passenger. Don't be stubborn!

"The event path is too idiosyncratic to hedge." This is almost always said by the same person who then wants to size the position up very large. If it's too complex to hedge then (just my opinion) it's too complex to concentrate. If you're concentrating, at least explore finding the hedge and then size it. There is always a trade structure to consider: a put spread, a collar, a correlated proxy, a partial synthetic from your prime broker. The tools are all there.

Two of those excuses are laziness. One is ego. None of them are good enough when you're managing other people's money.

Hedge the position. Hedge the book. Or size it like you know you can't.

Haters...I will be waiting for you in the comments! Let's go!

English

@Geo_papic @Malone_Wealth Equities are an expected NPV of the long-term cash- flows so compare to Dec29 and longer curve

English

@Malone_Wealth I like this take. I want to believe it.

Another way to think about it, however, is that the Brent is trading on supply risk, whereas the underlying equities are also having to consider recession risk due to supply risk to crude.

English

Oil is up 55% in three weeks. Chevron $CVX is up 8% and Exxon $XOM is up 4.7% in the same time. Do you know why? Almost no institutions and large buyers are buying in. Which could set up for the biggest commodity rug-pull in history for all of the Mom and Pop investors being convinced by media to buy into this.

English

@dampedspring Did they use ultrasound to break it or smth? Wonder whats the SotA in US for it?

English

I have the misfortune of being in the midst of passing a kidney stone. It is way less painful than reading #fintwit talk about Iran tho.

English

@tleilax___ You can add to your bench relatively quickly, esp from low base

English

My quant benches 140 kg (fit german dude). I bench 95 kg (little old me).

Rules are rules, we need to make more PnL this year than we collectively can bench.

English

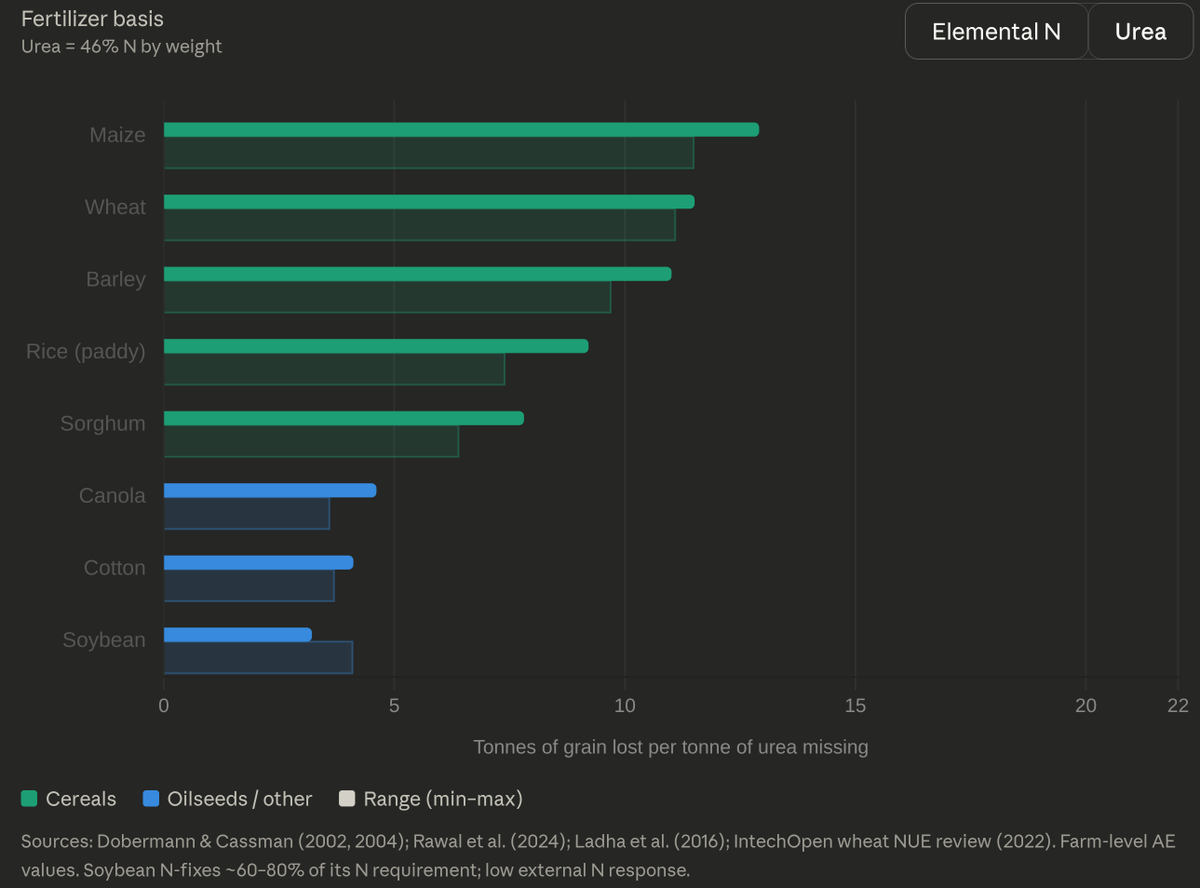

Losing 7 to 9 millions tonnes of grain production per tonne of nitrogen fertilizer missing.

unusual_whales@unusual_whales

China has restricted fertiliser exports, per Reuters

English

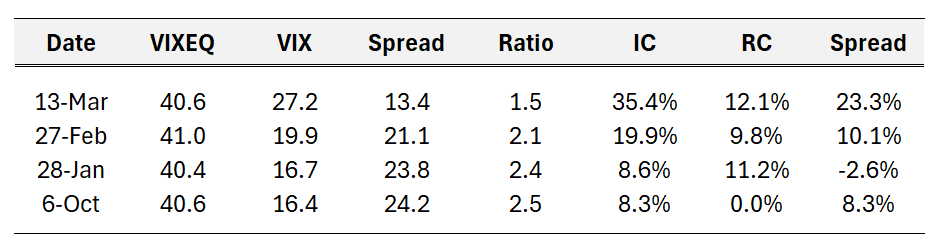

This is a fascinating time to study market prices. The table below shows the "single stock VIX" (VIXEQ) at Friday's close and 3 other times when it was at roughly the same level. The spread and ratio of the VIXEQ to the VIX are very related to the level of implied correlation.

Implied correlation is the single risk factor I've spent the most time on over the past two years. Just like implied vol, implied correlation is driven by carry. That is, its spread to realized. When realized vol goes down, so does implied vol. That's because the economics of the hedge portfolio for an option deteriorate when realized vol falls.

Implied correlation also falls when realized correlation falls. The last several years the SPX has experienced realized dispersion (low correlation) to an extent nearly unimaginable just a few years earlier. The dampening of vol at the index level has been wonderful, but potentially leading investors to underestimate how much risk there was in the index. I've argued that never seen before levels of realized correlation have been a risk hiding in plain sight.

What we see now is a repricing of the relationship between single stock vol and index vol. The numbers below tell the story. The VIX is 10(!) points higher for the same level of single stock vol. If you had the dispersion trade on (and depending how you had it structured), that could be a pretty significant neg mark to market.

Here's what's worth appreciating. The final column is realized correlation. It's up, but not by a great deal. Essentially, the market has simply bid up index vol relative to SS vol because it's willing to pay more for future correlation. That's the spread in the last two columns - the CMP "Co-movement Premium".

Again, to recap, the market has moved the VIX up by 10 without moving single stock vol at all. It's demand for index vol driven by a bid for correlation. If you are in the trade where you are effectively short correlation and you are watching the world of risk unfold, risk management is job#1 and that's about reducing sizing and seeing where the market will ultimately reprice to.

What makes the repricing thus far so worthy of thinking about is that it has not been driven by a surge in realized correlation (ala the Tariff Tantrum of 2025). It's all risk premium and specifically correlation risk premium.

English

@mihaljevic @wmthomson22 Why not play the storage? Sell front buy backs, profit

English

@wmthomson22 The bar for "emergency" has been moving steadily lower. We used to save these tools for real crises.

English

Are we in an “emergency” situation that warrants releasing more than 182 million barrels of oil? Are we really there yet? I think the world needs to adjust the line we drew for when massive coordinated government intervention in the global economy is warranted.

English

@dampedspring @BobEUnlimited My point that at the time most of the ppl knew about subprime but thought it was too small to matter. Only after LEH wasn't saved we had most of the damage and seniors tranches/credit etc puked. Me thinks policymakers still scarred from that time and response will be different

English

@YuriWerewolf @BobEUnlimited It is similar. It is tiny but same

English

The current oil shock is at least 10x more important to the economy than all the possible losses in private credit.

Thanks for coming to my TED talk.

English

@dampedspring @BobEUnlimited What if it is similar to subprime? Depends on policy response as always

English

@runews Was training wrestling . Didn’t see…. Was there any specific news ?

English

good miners eat oil and create gold

so this makes sense

Correlation Economics@GoldForecast

Gold is flat on the month and gold miners are trading like gold is down 20%. 🤨

English

@PeterBerezinBCA Such an obvious decision. What do they think? Thats the whole point of storage

English

This was a bad decision. The oil curve is in massive backwardation. They should sell oil into the spot market at the high price and then contract to buy it back at much lower prices later this year.

Javier Blas@JavierBlas

BREAKING: G-7 nations decide against releasing SPR for now G-7 agreed to continue monitoring energy markets Japan says IEA recommended G7 to release SPR

English