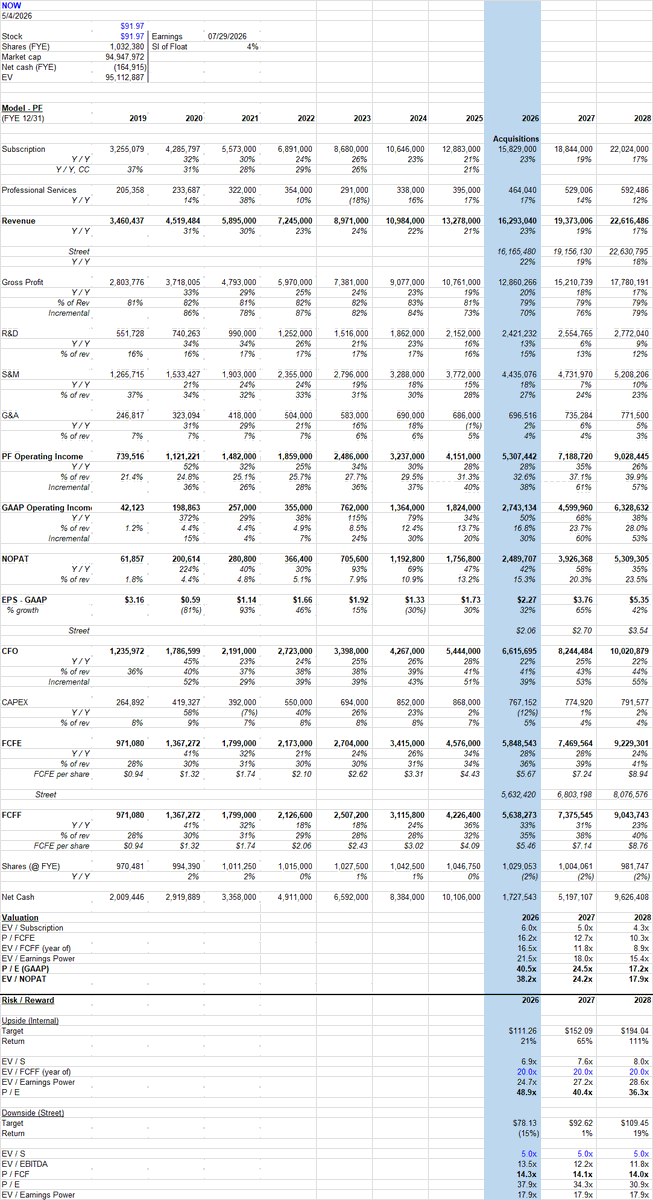

@TechFundies Company is guiding to ~11% GAAP margin this year. You are modeling 16.8%? What am I/the market missing? I see lower SBC and amortization adding 8-10% by 28/29, so low 20s GAAP margin vs you at 28%. Seems optimistic?

English

Abhinav Shah

895 posts

@abshah101

Founder & Portfolio Manager

Dusted off $MKTX after ignoring it since '19. Not sure what to make of current set-up. The thesis that liquidity begets liquidity & corp bond market is too fragmented to have multiple players is clearly broken. I never expected $TW to gain this level of market share.

Happy Friday: Crazy Chart Disney vs Netflix market cap past 6 years Both ~ $160 billion today $DIS $NFLX * Disney acquired Fox assets March 2019)

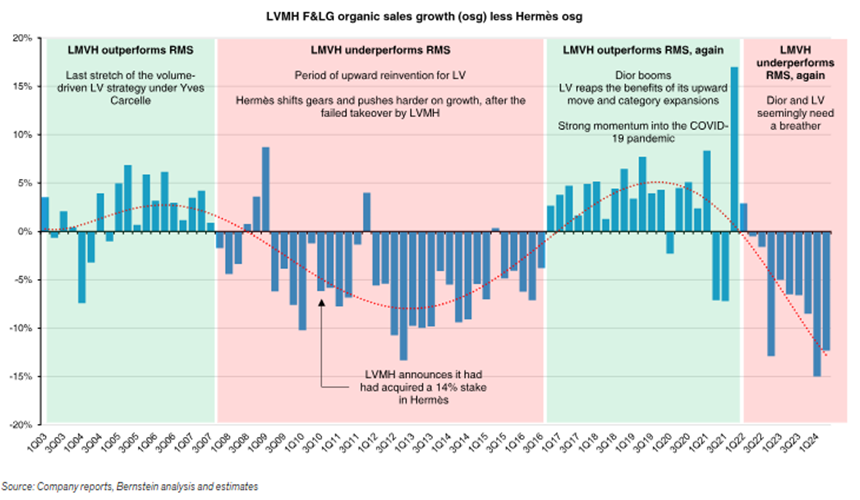

Estee continued blow-up vs $LRLCY & $LVMUY strength = under-exposure to fragrance + greater reliance to China tourist flows. Mostly one-off, especially as even $EL acknowledges in 'challenging' Q beauty growing strongly. But can't fault investor patience wearing thin.