ftangftang 🌍 retweetledi

ftangftang 🌍

3.7K posts

ftangftang 🌍

@buzzardstubble

pale blue dot #BTC #web3 #TAP $XTP #KR1 #COIN

Katılım Mart 2014

389 Takip Edilen226 Takipçiler

ftangftang 🌍 retweetledi

ftangftang 🌍 retweetledi

New month, new quarter = busy time for funds investing new money.

New tax year, new ISAs = busy time for retail investors allocating new money

#TAP is a clearly an opportunity in the oversold crypto equity sector @Tap_Fintech $XTP #TAP

English

ftangftang 🌍 retweetledi

@TapGlobalPlc Great to see such strong and consistent progress from @Tap_Fintech / $xtp 🔥

Stable revenues combined with strategic partnerships and user growth are exactly what builds long-term value 💎

Looking forward to seeing the next milestones 🚀

keep up the great work 💪

English

ftangftang 🌍 retweetledi

.@TapGlobalPlc reports H1 2026 results: revenue stable at £1.7m, user growth to 398k, but profitability impacted by higher costs. Strategic partnerships, new B2B offerings, and XTP token acquisition support long-term growth. #TAP @Tennyson_Secs @Vigo_Consulting

English

ftangftang 🌍 retweetledi

Tap kicked off H1 to Dec with stable revenues & solid progress.

Strategic partnerships, growing users & enhanced corporate services are building a strong foundation for growth 📈🪙

🔗shorturl.at/KgTTC

#FinTech #Crypto #DigitalAssets

English

ftangftang 🌍 retweetledi

ftangftang 🌍 retweetledi

English

ftangftang 🌍 retweetledi

If you're still using multiple apps for different currencies, it's time to switch.

Tap unifies everything:

• 70+ currencies supported

• Lightning-fast transfers

• Growing at record speed in 2025-2026

Business or personal — Tap scales with you.

Try it today → @Tap_Fintech

English

ftangftang 🌍 retweetledi

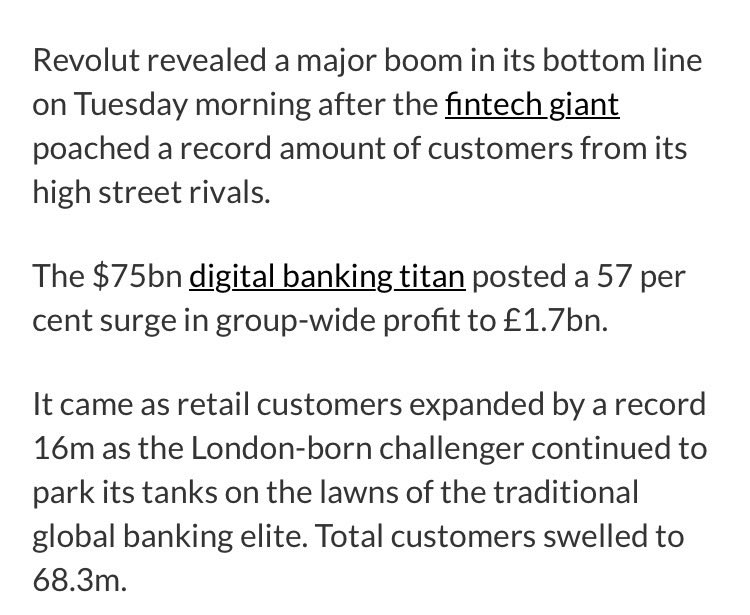

Amazing figures from Revolut demonstrate the massive opportunity offered by UK listed #TAP and its native token $XTP @Tap_Fintech

English

ftangftang 🌍 retweetledi

ftangftang 🌍 retweetledi

This is what our planet looks like from a distance of 1.5 billion kilometers.

The Cassini spacecraft captured Earth as a pale blue dot beneath Saturn's rings.

English

ftangftang 🌍 retweetledi

Some exciting things to happen on the headquarters 😉 not a bad moment to hop on the bandwagon 📈 $xtp @Tap_Fintech #WEEX #CryptoRecovery

TheComprador@TComprador

A new dawn at $XTP 📈

English

ftangftang 🌍 retweetledi

One word in the latest @UKOpenBanking analysis stood out for us: “everyday”.

It’s a framing we’ve always liked. Open banking works best when it becomes part of normal life rather than something unusual or disruptive.

shorturl.at/53O3T

#OpenBanking #OpenEcosystem #Fintech

English

#Tap Global shares on the move 📈

@Tap_Fintech $xtp

Zaks Traders Cafe@ZaksTradersCafe

Tap Global (TAP): The lock-in appears to be working... #TAP

English

#Tap Global company 'lock in' could allow the shares to finally break 3p, and give long suffering shareholders the kind of valuation on their company that they deserve.🙏

@Tap_Fintech $xtp

Zaks Traders Cafe@ZaksTradersCafe

The Week In Small Caps: March 14 Zak Mir looks at the affect of Iran on the major markets, as well as highlighting small caps such as Stack BTC, Zenith Energy, Pantheon Resources, and 88 Energy - Zaks Traders Cafe zakstraderscafe.com/the-week-in-sm… #FTSE100 #Gold #WTI #STAK #TAP #88E #PANR #ZEN #CTAI

English

#Tap Global . hybrid app with EU IBAN, UK account details, Visa cards, and built-in exchange for crypto-fiat swaps

@Tap_Fintech $xtp

Nick Research@Nick_Researcher

➥ What if i tell you millions of users will use crypto cards globally ICYMI, Neobank platforms blend traditional fintech with Web3 features, all built on top of STABLECOINS: • hold crypto + fiat in one account • spend via Visa/Mastercard cards • earn DeFi yields • convert instantly between fiat and stablecoins In practice, they look like Web3 banks, but with very different architectures Right now the landscape is roughly split into 3 models: [1] Hybrid fintech platforms = Fiat + crypto accounts, usually custodial or semi-custodial [2] Web3-native neobanks = Self-custody wallets with on-chain settlement [3] Exchange-backed cards = Direct spending from trading accounts At the product level, several trends are emerging: • stronger self-custody emphasis • cashback in crypto or stablecoins • low or zero FX fees • Solana-native cards for fast/cheap payments • direct integration with DeFi yield strategies Several platforms are already scaling fast The ones I see mentioned most often right now include: • @Revolut → hybrid super-app with 65M+ users, crypto + multi-currency spending • @wirexapp → one of the earliest crypto card pioneers since 2015 • @KASTxyz → Solana-focused card with direct stablecoin spending & strong rewards • @AviciMoney → self-custodial Solana neobank growing quickly in card volume • @RedotPay → millions of users & billions in card spend • @gnosispay → programmable Visa cards built on Safe smart accounts • @ether_fi Cash → spend directly from DeFi yield strategies • @MetaMask Card → wallet-native Mastercard for stablecoin spending • @Bybit_Official Card → exchange-backed crypto debit card • @UR_global → borderless multi-currency app with debit card, full global banking rails, and crypto-fiat bridging on Mantle • @zothdotio → Privacy-First Stablecoin Neobank for the Global South & the Agentic Economy • @Tap_Fintech → hybrid app with EU IBAN, UK account details, Visa cards, and built-in exchange for crypto-fiat swaps • @Fiat24Official → Swiss-regulated wallet-linked IBAN and debit card for tokenized fiat on Arbitrum • @Nexo → lending-focused platform with credit/debit cards, up to 15% yields & 0% APR borrowing against crypto holdings • @ready_co → USDC-native Mastercard debit card with up to 10% initial cashback, focusing on direct stablecoin spending without conversions • @holyheld → self-custodial debit card w personal IBAN, up to 1% cashback & integration for onchain to fiat flows • @BleapApp → Revolut-inspired hybrid neobank with low-fee crypto cards, stablecoin savings & global spending options • @itstuyo → full self-custody debit card for cash balances, with virtual/physical options & plans for broader stablecoin integration • @superformxyz → user-owned stablecoin neobank with SuperVaults for yields, swaps & self-custodial spending • @On_Veera → onchain mobile neobank with prepaid Visa cards, 4-10% yields on RWAs/crypto & borrowing via on-chain credit scores • @vPay_Global → AI-driven Web3 omnibank with offshore USD accounts, SWIFT/SEPA & Visa cards linked to DeFi yields When I zoom out, the bigger pattern becomes clear - Stablecoins are building the monetary layer - Crypto neobanks are building the distribution layer And historically, whoever controls distribution usually captures the most value in payment networks For more context, check on the stablecoins repport bellow ↓↓↓

English

ftangftang 🌍 retweetledi