Christoffer Fryd

97 posts

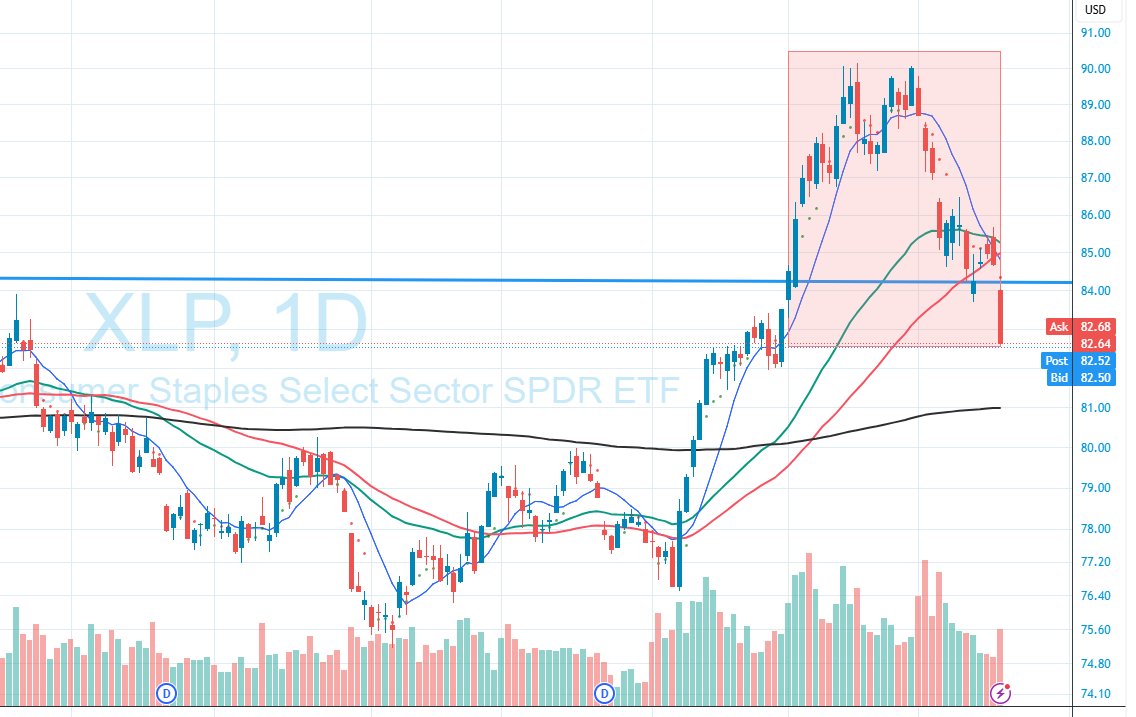

This is why you don't chase into defensives if you think the overall market has risk...

When the selling picks up, they are unlikely to buck the trend.

$XLP $XLV

English

EUROPEAN UNION: WE NEED AN EXIT FROM THE WAR WITH IRAN, NOT ITS ESCALATION

English

@oguzerkan Tom Lee: 'Small correction, then 10x rally the next 3 years.'

English

What happens to the global economy if China invades Taiwan while the Strait of Hormuz is still closed?

unusual_whales@unusual_whales

Taiwan reports large-scale Chinese military aircraft presence near island, per POLITICO

English

FINANCIAL STOCKS ARE OFF TO THEIR WORST START TO A YEAR SINCE THE COVID PANDEMIC, WITH INVESTORS EXPECTING MORE PAIN AHEAD AS WORRIES OVER EVERYTHING FROM PRIVATE CREDIT TO THE IRAN WAR ROIL THE TROUBLED SECTOR.

English

Trump going from Venezuela to Iran is basically like me trading.

Venezuela? Perfect setup, worked but I sized too small.

Next trade? I am euphoric, I go 10x size on a shitty setup: Iran. It goes wrong. But I am trapped, keep adding size and blame the market for being wrong.

English

@PronkDaniel Sure, but at what multiples are those assets valued?

English

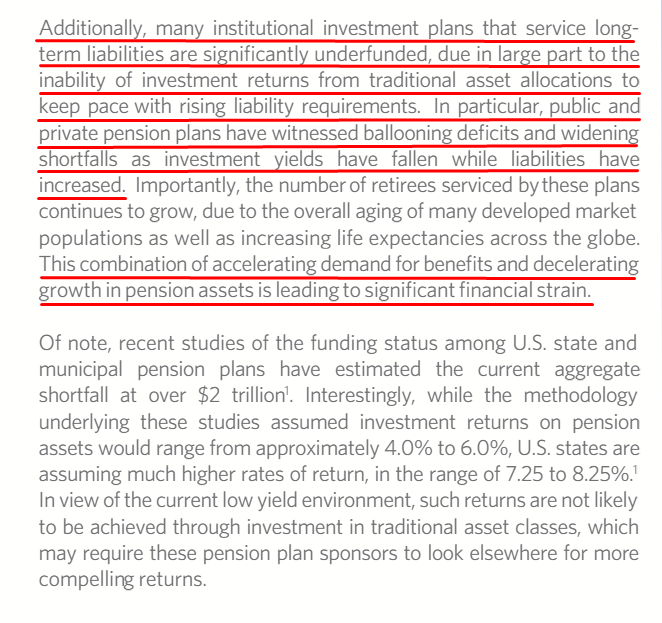

In 2013, $BN wrote an article "Real Assets, The New Essential."

In it, it discussed the issue of retirement insurance and pensions not having enough assets to cover the growing liabilities (retirement income).

They then entered the industry to offer an alternative.

English

The most overlooked trade in the market right now:

Fertilizer stocks.

Why:

→ Food is non-negotiable

→ Supply is fragile

→ Few equities exist for exposure

→ Billions in capital chasing the theme

Fert stocks can make silver juniors blush.

English

@crux_capital_ All this can change quickly if oil continues to rise (we are witness the largest supply shock in recorded history, 17x larger than Russia/Ukraine), inflation spikes and earnings are weak.

English

🚨What would crush the optical supercycle?

$LITE $COHR $AAOI $CIEN $AXTI

As investors we must consider this reality.

In my opinion, it would be a slow down in Hyperscaler spend

So let's get a pulse check on what this looks like...

Right now, instead of a slowdown, we are seeing violent upward revisions.

$CIEN CEO Gary Smith noted that in just the last few weeks, the four largest global hyperscalers outlined a "step function increase in their 2026 CapEx to more than 600 billionin aggregate".

$NVDA CFO Colette Kress confirmed this massive expansion, pointing out that expectations for the top five cloud providers are now approaching $700 billion.

$MRVL had a wild revision. Back in September, they guided for $9.5 billion in revenue. In December, they raised it to $10 billion. On their latest call, they raised it again, noting they now expect revenue "approaching $11 billion," with CEO Matt Murphy bluntly stating they expect $15 billion next year which is roughly $2 billion higher than the outlook they provided in their December earnings call.

Marvell specifically noted their optical interconnect business is now expected to grow "more than 50% year-over-year".

Now let's take a step back...

Why are hyperscalers spending almost three-quarters of a trillion dollars?

One major reason that we have been seeing a ton on X is the inflection in Agentic AI. AI agents are now autonomously solving problems, writing code, and generating tokens. As Jensen Huang explained, "In this new world of AI, compute is revenues. Without compute, there's no way to generate tokens... compute equals revenues".

Every hyperscaler understands that failing to build compute directly caps their top-line growth.

When these hyperscalers get nervous about this spending, we will see hesitation in the supply chain.

Instead, what we are seeing today is unprecedented buying across the board:

$MRVL CEO Matt Murphy stated they are seeing "very strong demand across our entire Data Center portfolio, with bookings accelerating at a record pace". He added that customers are "signaling robust demand not only for this year but for the next several years".

$CIEN Called Q1 demand "unprecedented," with backlog surging by $2 billion in a single quarter to $7 billion. Management noted, "nearly all new orders we are taking now will be for fulfillment in fiscal 2027".

$COHR CEO reported a data center book-to-bill ratio that "exceeded 4x". He added that most of their calendar 2026 is already booked out and 2027 is filling up very quickly.

$LITE confirmed they are completely sold out of critical Indium Phosphide lasers, with capacity "spoken for in these LTAs... that run through the balance of calendar 2027".

And if you need ultimate proof that the spending isn't slowing down, look at NVIDIA's own actions.

Recognizing this massive bottleneck in the optical supply chain, NVIDIA just made a $2 billion investment and a multi-billion dollar purchase commitment directly into Lumentum to fund a new laser fab. By doing this, NVIDIA is effectively locking up "a significant amount of the world's capacity of indium phosphide".

A hyperscaler CapEx slowdown would absolutely hurt this trade.

But right now, the data tells the exact opposite story. Hyperscalers are engaged in a nearly $700 billion arms race.

The optical supply chain isn't worried about a demand slowdown. They are frantically trying to figure out how to manufacture enough lasers, switches, and DSPs to satisfy an industry that is already booked solid well into 2027.

Will keep an eye on this as the thesis plays out

Gaetano@crux_capital_

Bullish Optics $LITE $COHR $GLW $AAOI $CIEN etc.

English

@ZeeContrarian1 - Iran has 3k+ mines & A2/AD drone swarms.

- Actuaries set insurance, not politicians (Red Sea proved this).

- Hormuz moves 20M bpd. Max US SPR drawdown is 4.4M bpd. You can’t fill a 20M barrel hole with a 4.4M hose.

English

CONDITIONS, NOT OPINIONS

When oil was trading at 59, I told you to load it. Not because of an opinion but because the conditions were obvious. I analyze conditions, not narratives. As you can see, that call was very right.

Today the same process points the other way.

All the pundits who never told you to buy oil at 58 are now screaming that oil is going to 140 and that the world is ending. They trade opinions. I watch conditions.

Let’s name the conditions.

Iran is running out of missiles. Today they fired one missile at Israel.

Iran has no production capacity to sustain a long conflict.

Iran has no navy capable of blockading the Strait of Hormuz.

Iran has no mines in the Gulf.

Right now the only real thing Iran can still do is fire drones at ships to damage them and scare traffic away. We already saw drones hit tankers and ports in the region. But this kind of harassment can only go on for so long before it’s neutralized or shipping resumes under protection.

The problem with ships crossing the strait right now isn’t even Iran. It’s insurance. Because of the chaos, insurers stepped back and ships hesitate to cross. That will be solved.

All the major powers in the world are united around one objective: keep the Strait of Hormuz open.

High oil hurts almost every advanced nation on earth. It damages growth, inflation, and stability. The world’s richest and most powerful countries want lower energy prices.

Iran is running out of options very fast. Their only real hope is panic.

This won’t last forever.

My catalyst right now is the release of strategic reserves. There is a big misunderstanding about how reserves actually work. Reserves are not meant to replace total production. They are meant to supplement supply during disruptions. Countries like the United States still have massive domestic production and access to imports, which means reserves don’t have to cover the entire market. They are released gradually to stabilize prices.

When reserves are used alongside ongoing production, they can last for a very long time and have a powerful effect on the market. That combination can push oil prices lower much faster than people expect and buy time for Israel and the United States to finish the work more calmly while the Strait of Hormuz is secured.

And when this is over, the panic premium disappears and a peace premium replaces it.

That’s when oil crashes.

Mark my words. The same conditions that created the opportunity at 58 are now pointing the other way.

Give it three to six months and I believe you will see oil sub 60.

Watch conditions. Ignore opinions.

Z@ZeeContrarian1

The Iran–U.S. situation could make you rich Look at what’s happening right now. The U.S. keeps shifting forces into the region-carrier groups, aircraft, assets. Every few days there’s another update, more hardware being repositioned. This costs an absolute fortune. You don’t do this publicly, at this scale, unless there’s a real reason. Technically, this would hit the front month of the oil curve hardest - a backwardation shock, very similar to a $VIX spike. That’s exactly the kind of move where options pay. If you’ve been following me, you probably started building your position a couple of days ago. If not, I don’t think it’s too late. Now look at the probability tree. 50% probability nothing happens - you lose the premium. 40% probability an attack happens - oil spikes and you’re looking at 5x–10x on your options. And then the tail: 10% probability this escalates further. Iran retaliates against regional oil infrastructure or neighbors. If that happens, oil goes vertical and you’re talking 20x–30x returns. You almost never see asymmetry like this. Situations like this don’t come around often.

English

@realroseceline You do NOT want to be exposed to inflationary currencies with oil headed north of $100 for the foreseeable future

English

$DLO an attractive investment opportunity at $11/share

$DLO may be mispriced after falling roughly 80% from its high, despite continued growth in the business.

$DLO is essentially payments infrastructure connecting global merchants with consumers in emerging markets. Companies like streaming platforms, marketplaces, SaaS, and global tech companie want to sell in places like Brazil, Nigeria, India, etc but payment systems there are fragmented and require local entities, regulatory approvals, multiple integrations, etc.

$DLO simplifies this by providing one integration that allows merchants to accept hundreds of local payment methods across more than 40 countries. $DLO becomes the payment bridge between global commerce and emerging market consumers, a massive addressable market since billions of people in these regions are still underbanked but increasingly shopping online.

Last quarter the company generated about $282m in revenue, up 52%, beating expectations slightly. Earnings per share was $0.17, also above estimates. Total payment volume reached $10.4b, growing nearly 60%.

On a TTM basis revenue is ~$960m, growing roughly 32%, while free cash flow increased to ~$37m, up 28%. Analysts expect revenue growth to remain strong, with high 20% growth projected over the next several years, making $DLO one of the faster growing fintech companies.

Another point is geographic diversification. Historically $DLO generated most of its revenue from LATAM. In 2022 ~91% of revenue came from LATAM, but by 2025 that declined to 78%, not because LATAM shrank but because the company expanded into Africa and Asia, reducing regional risk and expanding the opportunity.

Another interesting detail is $DLO scale relative to its customer base. The company serves roughly 1,000 customers and somewhat ironically also has about 1,000 employees. That is a small customer base given the size of the global opportunity. Most clients are large multinational companies, but there is no reason $DLO cannot expand beyond that. As global commerce expands, it is reasonable to imagine $DLO eventually serving 5–10k global merchants, allowing payment volume to grow dramatically without proportional cost increases.

Customer engagement is strong. $DLO has 136% NRR, meaning existing clients increase their spend each year. In software and payments businesses anything above 120% is considered excellent, so 136% suggests that once companies integrate with $DLO they expand usage significantly.

It is also important to understand the structure of the business model, which is capital light and cloud based. Unlike traditional payment infrastructure companies that rely on legacy systems, $DLO can scale into new markets without major cost increases. As payment volume grows, more revenue falls to the bottom line, creating operating leverage.

$DLO already works with many of the world’s largest technology companies, including 6 members of the “Magnificent Seven.” This positions $DLO as a critical infrastructure partner for global companies expanding internationally.

Despite these fundamentals, $DLO is heavily discounted relative to its past highs, with a forward P/E around 17 and analyst price targets generally around $15 to $19. The disconnect between strong growth and depressed valuation creates an attractive risk reward opportunity for long term investors, in my opinion.

However there are risks since $DLO operates in emerging markets, it faces challenges from currency volatility, regulatory changes and macroeconomic instability that can impact payment volumes and margins. Competition and merchant concentration also need to be considered.

$DLO is positioned to take a small tax from transactions at the intersection of global ecommerce growth and emerging market digitization, two powerful long term trends. If those trends continue and $DLO executes well, the stock could become a multibagger over the next ~5 years, even if it remains volatile in the short term.

🌹

English

@PeterBerezinBCA @rrobert7771 Nope. They will use Trumps TACO as leverage until they get what they want. 1. Removal of all US bases in the region. 2. Dismantle of Isreals atomic weapons.

This will never happen, so the war continues

English

@rrobert7771 If Trump stops the bombardment, the Iranians will too.

English

I disagree. It completely makes sense for Trump to short oil futures a few hours before he declares victory and deescalates.

ron insana@rinsana

The Treasury reportedly plans to short oil futures next week to drive down energy prices. If oil infrastructure in the ME is badly damaged, Gulf States shut in production & the Strait remains closed, prices will blow through their shorts, potentially causing losses of taxpayer $!

English

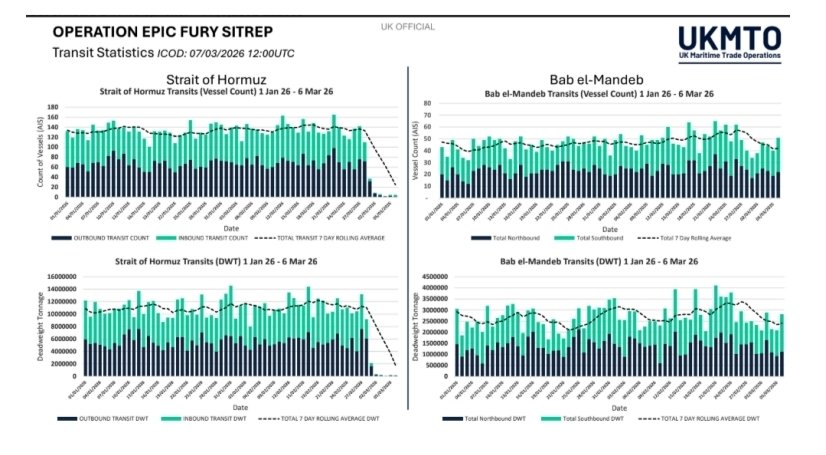

Strait of Hormuz vessel transits remain low - UKMTO

English

@aleabitoreddit The fear is global recession and demand destruction, and therefore lower multiples

English

The sentiment around KOSPI | $EWY (SK Hynix / Samsung) on

Crude Oil / LNG / Helium either:

Disrupting Supply or Compressing Margins are overblown.

The supply chain disruption and energy cost threats to SK Hynix, Samsung are sensationalized noise.

Here's why:

1. Crude Oil:

The a likely scenario if oil prices increase 31% and oil floats to $120/bbl:

In this case, the effect on oil has almost no material impact on SK Hynix and South Korean memory equities.

There are increased energy costs via oil-pegged LNG/JKM prices on Korean equities, mainly for companies surviving on razor-thin 5% to 10% margins.

However, a KEPCO 70% rate hike has little material affect on Samsung/SK Hynix, given memory prices have soared with Samsung doubling NAND prices Q2.

From disclosed financial from, their SK Hynix's annual electricity bill exceeds ₩1 trillion per DIGITIMES (~$750M). Which against FY2025 revenue of ₩97.15 trillion represents roughly 1–2% of revenue.

SK Hynix posted a 58% operating margin in Q4 2025. Against this backdrop, the energy cost shock is small:

If we model a 50% increase in energy costs:

- Hit to SK Hynix quarterly OP (₩19.17T): ~₩134 billion-~₩146 billion (0.76%)

- Hit to Samsung DS quarterly OP (₩16.4T): ~₩407 billion (2.4%)

Every 50% energy cost spike would shave roughly .7% off SK Hynix margins and 2.4% off Samsung operating margins.

Analysts project SK Hynix margins could reach 70%+ on conventional DRAM in 2026. Energy costs do not meaningfully threaten Korean semiconductor operating margins, even if they were to increase by 100%.

However, this is material to companies with low operating margins of 5-10%

The Losers: Traditional heavy manufacturing (steel, basic chemicals, standard flat glass).

The Winners: Samsung/SK Hynix.

The main risk is second-order effects on supply chains such as increased material costs. This is very hard to model, but in an example where:

an industrial company forces 30% price hikes on raw materials (chemicals, specialty gases), it barely dents the fabs.

Materials are roughly 15-20% of semiconductor COGS, so mathematically, a 30% spike in material costs only shaves an additional ~2% off SK Hynix's operating margins.

A combined 3-4% direct (utilities) and indirect (materials) energy headwind is easily absorbed by an oligopoly printing 70% margins (and increasing prices).

In majority of cases, the costs likely get passed down to hyperscalers through NAND/DRAM price hikes.

In the very worst case scenario of oil prices increasing 3x or 5x.

The main affect on oil increasing hundreds of percent are two factors:

- Global macroeconomic shock, causing global inflation (affecting every single company, from $GOOGL to $COST).

- KRW (South korean Won) USD/KRW exchange rate blowout.

KRW depreciation from sustained high oil is a real second order risk, but historically Korean memory exporters benefit from won weakness on the revenue side. The majority of Samsung/SK Hynix sales are dollar denominated wheras costs are won denominated. So a weaker KRW is actually margin accretive for exporters, which partially offsets the energy cost headwind.

But in an extreme case of oil prices hiking 5x, the only longs in that apocalyptic world are crude oil itself, defense contractors like $LMT / $NOC, domestic US energy producers, and the US Dollar.

This is unlikely to happen.

The financial media and algorithms will likely panic, but , if crude oil goes from $91 to $120 and KEPCO increases energy costs:

The data shows there's little affect on Samsung / SK Hynix in specific, and the main impact are on players with razer-thin operating margins.

2. LNG:

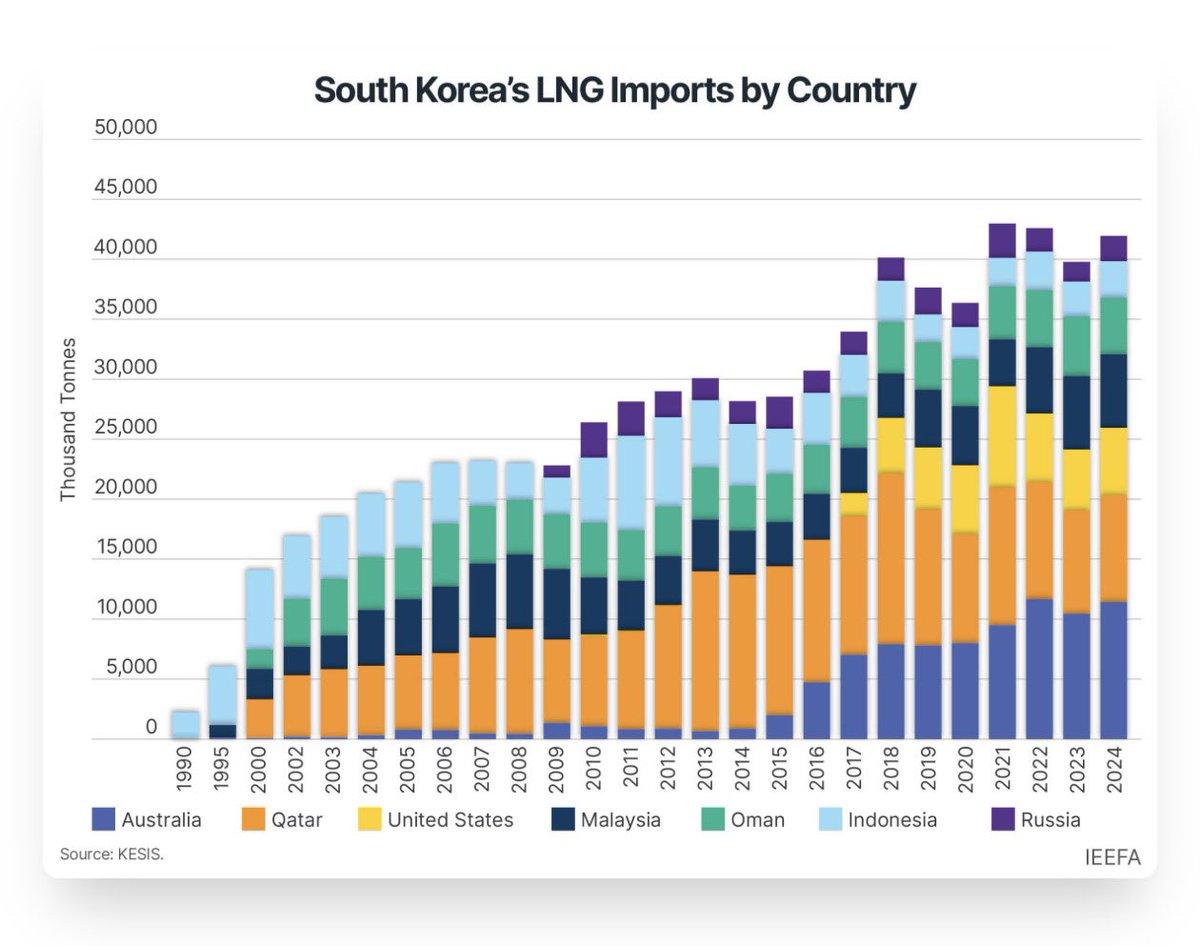

If the Hormuz closed, the majority of South Korea’s LNG imports would be unaffected.

The media has been quoting Hormuz + LNG flows going to China, INdia, SK, and Japan. But if we look at the trade data from South Korea, that’s just a fraction of their total imports.

Majority of imports arrive via Hormuz free routes, eg. Australia (24.6%), US (12.2%), Malaysia, Indonesia (~20%), and Russia/Sakhalin (~4.6%). Then the rest filled in with minor sources from Nigeria, Peru, Brunei, PNG, etc.

The 82% of 2024 important were long term contracts that were oil-indexed, and as we've modeled above, increasing energy costs would hurt opex by 1-2% per 50% increase, but given DRAM/NAND price hikes and operating margins hitting 70%+, this would make a very little dent.

Even if they did, costs would be passed onto hyperscalers.

South Korea learned their lesson from 2022 and diversified sources, and there's little impact on LNG supply disruption. The main concern is oil impacting hiking of LNG.

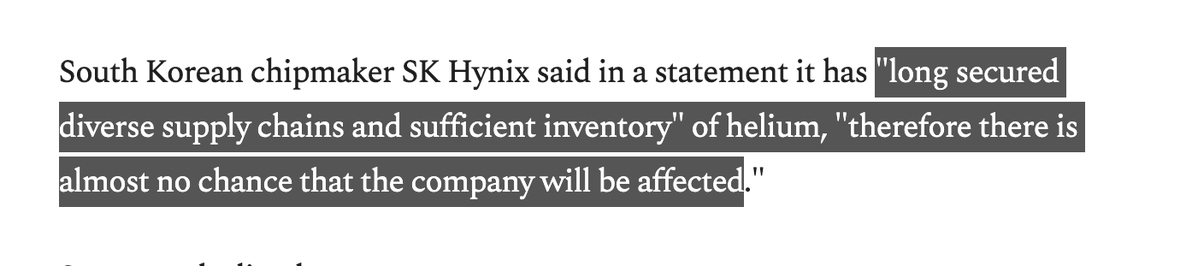

3. Helium:

SK Hynix statement: “Long secured diverse supply chains and sufficient inventory" of helium.

"Therefore there is almost no chance that the company will be affected [by helium].

The reality is larger players like $TSM to SK Hynix have diversified their supply chains against foreign events.

Helium is critical to semiconductor supply chains, but the media narrative is sensational. Especially when the largest memory company puts out an assertive statement that there’s no chance the company [SK Hynix] will be affected.

_

But to South Korean equities in Samsung/SK Hynix, fears around Oil/LNG/Helium look disconnected from reality:

The algorithms selling off SK Hynix because of helium and KEPCO rate hikes are acting on bad math. It is fundamentally a supply chain non-issue.

The main threat is oil and energy costs on global macroeconomic shock affecting everything from consumer goods to inflation.

March 3 "Black Tuesday" crash dropped KOSPI dropped 7.2% and SK Hynix fell 11.5% in a single session on exactly these energy security fears as the main catalyst. Of course, forced liquidations from leverage added fuel to the fire.

However, the disconnect between fundamentals and price action is the trade. If margins were actually threatened, the selloff would be justified.

But, the sell-off destroyed more value in one day than DECADES of hiked energy cost increases could have.

The fact that the math doesn't support the fear is precisely why it's Korea is a buy, as markets are selling off on emotion rather than looking at the structural expanding profitability despite increasing oil/energy costs.

English

@calvinfroedge Problem is that the US's LNG export terminals are already running at 100%. The cheap US gas is literally trapped in the country. Long US chemical and fertilizer producers.

English

Here's the big dilemma. The US caused this fuel price spike.

If we restrict exports, we hang our allies out to dry. If we export too much, fuel prices in the United States go parabolic.

Craig Fuller 🛩🚛🚂⚓️@FreightAlley

There is no diesel supply issue in the US, but its important to know how diesel is priced. US diesel is priced against the NYMEX heating oil contract, which is traded based on WTI, which is influenced by global oil prices (Brent). The ULSD Rack price is essentially the wholesale price (tied to the heating oil contract) that is paid by downstream suppliers that add taxes, transportation, and their own markups. The pressure isn't domestic supplies, we have plenty, its global.

English

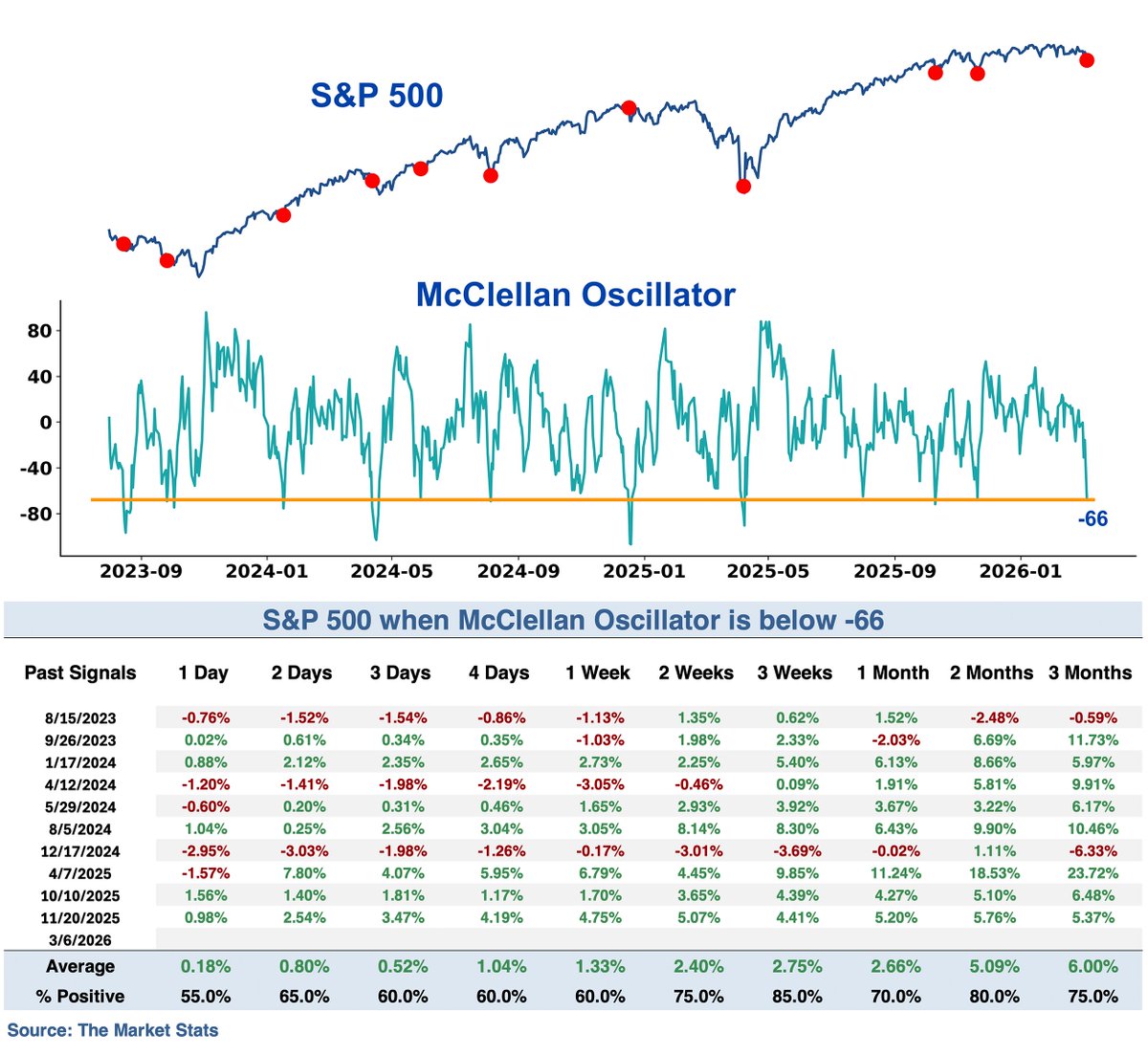

Market breadth is oversold

The McClellan Oscillator dropped below -66

Over the past 3 years, similar oversold readings saw $SPX higher 9 out of 10 times three weeks later, with an average gain of +2.75%

English

@fomocapdao - China and Russia enters the chat

- Orange man sends nuke

- Au revoir

English

If This Turns into Full War of Attrition (Next 2–8 Weeks)

Iran’s strategy: Fire 500 of missiles/drones per week. Target Israeli cities + Gulf oil & water to force the US/Israel to the table or collapse Gulf economies.

Week 1–2

Iran’s attacks on Israel drop in volume but continue (Haifa, Tel Aviv, military bases).

Iran ramps up strikes on Gulf energy: Qatar LNG halted, UAE oil terminals on fire, Oman ports hit, Iraqi Rumaila oil field shut, Saudi Aramco incidents).

Week 3–6

Full Attrition Kicks In

Oil impact on all Gulf countries:

Iran threatens/attacks more refineries, pipelines, and ports in Saudi Arabia, UAE, Qatar, Kuwait, Oman.

Strait of Hormuz partially or fully disrupted (Iran already claims “complete control” and has hit tankers).

Result: 15–20% of world oil & LNG supply offline global oil prices $150–250/barrel.

Gulf economies crash: QatarEnergy, Aramco, ADNOC halt exports. Storage fills up forced shutdowns. Governments lose billions daily.

Water impact on all Gulf countries (the real killer):

Gulf states depend on desalination for everything (Saudi 70%, UAE 42%, Qatar/Kuwait 90%+ of drinking water).

Iran has already attacked power stations feeding desalination plants (e.g., Fujairah, UAE).

If Iran escalates (they already signaled “you hit ours, we hit yours”): One or two precise missile/drone strikes on Jubail (Saudi), Ras Al Khair, or Taweelah (UAE) plants = catastrophe.

Riyadh (8.5 million people) could run out of water in 7 days and face mass evacuation. Same for Dubai, Abu Dhabi, Doha.

No quick fix, plants take months to repair. Contaminated seawater or power loss - humanitarian disaster, riots, refugee waves.

Endgame (2+ Months)

Best case for Israel/US:

They destroy enough Iranian launch sites and production factories Iran runs low on missiles, regime cracks under internal pressure.

Likely case:

Stalemate. Oil prices stay sky-high for months - global recession. Gulf water crises force Saudi/UAE to beg for ceasefire or join strikes on Iran.

Worst case:

Iran hits major desalination clusters, millions displaced across Gulf. Oil shock triggers worldwide energy crisis (Europe/Asia hardest hit). Possible wider war with Saudi Arabia or direct US ground involvement.

Bottom line: Iran cannot “win” conventionally, but in pure attrition it can make the Gulf unlivable by hitting water (more dangerous than oil) while crippling global energy. The US/Israel campaign is currently winning on degradation, but every extra week of Iranian missile/drone fire brings the Gulf closer to water + oil collapse.

English

I predict Brent Crude will reach an all time high before the end of 2026

English

@calvinfroedge How would you position the petrochemical stocks?

English