luda

104 posts

🛠️Investigating:

We are working to resolve an issue preventing players from Matchmaking into games.

We will provide more information as the situation unfolds.

Thank you for your patience.

English

@cryptopunk7213 just a wrapped kimi k2.6 model, nothing impressive about taking credit for another’s work lmao pathetic

English

this is huge news from Cursor, they've pulled of the impossible and turned their ai-wrapper into a in-destructible moat

sam altman literally called it <24hrs ago and here we are:

> cursor's ai agent harness is available for anyone to build on, which means ai models are now a commodity

> 1-time install and now anyone can run cursor's agent locally or via cloud. use any model (e.g. gpt 5.5) but with the added cursor harness that makes it 10X better.

> its so good that 3 of cursors biggest competitors are embedding it into their products.

> now cursor DOESN'T DEPEND on anthropic or openai. their own model (composer 2) competes directly!

yesterday sam altman said the ai model and harness are one and the same and today cursor turned their harness into a self-owned moat

fucking masterclass (coming from a former cursor / ai wrapper hater)

Cursor@cursor_ai

We’re introducing the Cursor SDK so you can build agents with the same runtime, harness, and models that power Cursor. Run agents from CI/CD pipelines, create automations for end-to-end workflows, or embed agents directly inside your products.

English

luda retweetledi

Ladies if your boyfriend uses the Claude Code VSCode extension instead of the terminal tool that’s not your boyfriend that’s your girlfriend

English

luda retweetledi

luda retweetledi

JUNE 2028.

The S&P is down 38% from its highs. Unemployment just printed 10.2%. Private credit is unraveling. Prime mortgages are cracking. AI didn’t disappoint. It exceeded every expectation.

What happened?

citriniresearch.com/p/2028gic

English

@RobinhoodApp can you make legend more responsive & load faster? it is too slow in general. Also add more ways to categorize and bucket holdings

English

@RobinhoodApp text scale sizing optionality in legend

Legend also needs to be faster, maybe just make a downloadable pc app bc it takes too long on the web to load charts and make trades. in order for legend to actually be useful it needs to be faster and more responsive

English

luda retweetledi

Dear AI Bears: Thank You For The False Narrative And The Cheaper Prices (Part 3)

I’ll start by thanking the AI bears for grasping at any detail no matter how small, distorted, or taken out of context when building their case against the AI revolution. On Wednesday, Oracle ($ORCL) reported Q2 earnings for the 2026 fiscal year and gave the bears something new to cling to. Oracle has decided to go all-in on AI and cloud, but it is doing so by tapping the debt markets rather than primarily funding this buildout through operating cash flow. In Q2, total revenue came in at $16.1 billion, and we continued to watch a legacy technology titan transform itself.

Cloud IaaS and SaaS accounted for $7.98 billion of total revenue, up 34% YoY. Meanwhile, the on-prem and software licensing business declined 3% YoY to $5.88 billion, highlighting the continued shift from legacy software to the cloud. Cloud Infrastructure (IaaS) generated $4.1 billion in revenue, up 68% YoY, while Cloud Applications (SaaS) grew 11% YoY to $3.9 billion. Oracle is staking its future on cloud and AI but the issue has become the funding approach. Bears have repeatedly cited the scale of hyperscaler CapEx, and Oracle just increased long-term debt from $82.24 billion to $99.98 billion. Citi published a research report indicating Oracle may need to raise $20–$30 billion in debt annually over the next three years based on the company’s expansion plans.

The bears finally got what they wanted. They can point to Oracle and argue:

· Negative net liquidity

· Reliance on debt markets

· Operating cash flow that cannot currently support CapEx objectives

This has contributed to commentary like the following on major finance shows such as Power Lunch:

“I think Michael Burry kind of suddenly made us realize that there really are a lot of uncertainties with regards to the future growth rate of these Magnificent Seven companies that are now competing in this AI race and in addition we know that there’s a lot of question marks about whether all this capital spending is going to pay off with a decent return. So suddenly there is a lot of uncertainty about the projections for strong growth in these seven companies.”

I’m happy to have a serious, intellectual discussion on this topic, because I believe the AI bears are wrong and ultimately fighting a losing battle. Technology does not remain stagnant, it advances. The Magnificent Seven are arguably the strongest collection of businesses ever created, led by some of the most capable management teams in corporate history. We are not watching one company making an isolated bet on a radical idea that may or may not work. These companies are actively building products and services around AI because AI has already been established as the next frontier of computing. Can we really take the bear case seriously when the executive teams at $NVDA $MSFT $META $AMZN $GOOGL $AAPL $TSLA have built trillion and multi-trillion-dollar businesses are signaling that we are still early in the AI cycle and that this is the future? I would rather listen to Andy Jassy, Sundar Pichai, Elon Musk, Mark Zuckerberg, Jensen Huang, and Satya Nadella than a cohort of bears on the sidelines who do not work in technology and have no involvement in the direction these companies are taking.

Statements like “there are question marks about whether all this capital spending is going to pay off with a decent return” are frustrating because they often sound like conclusions drawn from market caps and P/E ratios rather than from earnings calls, quarterly filings, and the operating results that have been unfolding for years. The statement is simply not supported by what we have been watching in real time. We have also seen what happens when CapEx is not treated as a priority.

Here are the facts:

In fiscal 2021, $AAPL allocated $11.09 billion to CapEx. Apple then allocated $10.71 billion in fiscal 2022, $19.96 billion in 2023, $9.45 billion in 2024, and $12.72 billion in 2025 for a total of $54.92 billion over the past five years. Since fiscal 2021, Apple increased annualized CapEx by $1.63 billion (14.7%). Over the same period, Apple generated $365.82 billion in revenue in fiscal 2021, which grew by $50.34 billion (13.76%) over the next four years to $416.16 billion. Apple’s cash from operations increased 7.16% ($7.44 billion) over the same period from $104.04 billion to $111.48 billion.

Now look at what happens when $MSFT, $GOOGL, $META, and $AMZN take CapEx seriously.

In fiscal 2021, Microsoft allocated $20.62 billion to CapEx, which grew 213% ($43.93 billion) to $64.55 billion in fiscal 2025. Over this five-year period, Microsoft allocated $181.64 billion toward CapEx. The impact on financial performance was substantial. In fiscal 2021, Microsoft generated $168.09 billion in revenue, which increased 67.61% ($113.64 billion) to $281.72 billion. Cash from operations increased 77.43% ($59.42 billion) over this period from $76.74 billion to $136.16 billion.

Microsoft was not an outlier. Google, Amazon, and Meta had similar outcomes.

In fiscal 2021, $GOOGL allocated $20.62 billion to CapEx, which increased 216.04% ($53.23 billion) to $77.87 billion in the TTM. Over the past five years, Google has allocated $218.78 billion to CapEx. Google’s revenue increased by $127.84 billion (49.62%) from $257.64 billion in 2021 to $385.47 billion in the TTM. Google’s cash from operations increased 65.22% ($59.77 billion) over the same period from $91.65 billion to $151.42 billion.

Meta is a similar story. Meta’s CapEx increased 235.65% ($44.04 billion) over the same period, rising from $18.69 billion in 2021 to $62.73 billion in the TTM. This supported revenue growth of 60.65% ($71.53 billion), from $117.93 billion to $189.46 billion. Meta’s cash from operations expanded 86.49% ($49.89 billion) from $57.68 billion to $107.57 billion from 2021 to the TTM.

For anyone to say there are “question marks” about whether this level of capital spending will produce a decent return is to ignore what has been happening quarter by quarter. Apple’s CapEx intensity increased modestly versus peers, while cloud and platform peers dramatically increased infrastructure investment and saw corresponding growth in revenue and operating cash flow.

I believe the bears finally got what they wanted with Oracle’s earnings because Oracle has become a convenient scapegoat for the broader AI bear case. Oracle has $19.77 billion in cash and short-term investments and $0 in long-term investments. Long-term debt now stands at $99.98 billion, putting net liquidity at -$80.22 billion. Oracle also generated $22.3 billion in operating cash flow over the TTM while allocating $35.48 billion toward CapEx, resulting in FCF of -$13.18 billion (operating cash flow minus CapEx, as reported). Bears finally have a metric they can latch onto but Oracle is one company, and its balance sheet structure does not define the rest of the AI ecosystem.

Bears should also keep in mind that debt funding is not automatically a problem; mismatch is. If Oracle’s RPO converts to revenue and margins hold, the funding mix could prove highly profitable. It is premature to treat Oracle as the definitive “poster child” for the AI bear thesis.

Now compare Oracle’s position to the hyperscalers.

Google has $98.5 billion in cash and short-term investments and another $63.8 billion in long-term investments. With $21.6 billion in long-term debt, Google’s net liquidity position is $140.69 billion. Google could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Google generated $151.42 billion in operating cash flow, exceeding the $77.87 billion allocated to CapEx, producing $73.55 billion in FCF.

Microsoft has $102.01 billion in cash and short-term investments and another $10.28 billion in long-term investments. With $35.38 billion in long-term debt, Microsoft’s net liquidity position is $147.04 billion. Microsoft could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Microsoft generated $147.04 billion in operating cash flow, exceeding the $69.02 billion allocated to CapEx, producing $78.02 billion in FCF.

Meta has $44.45 billion in cash and short-term investments and another $25.07 billion in long-term investments. With $28.83 billion in long-term debt, Meta’s net liquidity position is $40.69 billion. Meta could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Meta generated $107.57 billion in operating cash flow, exceeding the $62.73 billion allocated to CapEx, producing $44.84 billion in FCF.

Amazon has $94.2 billion in cash and short-term investments and another $20 billion in long-term investments. With $57.94 billion in long-term debt, Amazon’s net liquidity position is $56.26 billion. Amazon could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Amazon generated $130.69 billion in operating cash flow, exceeding the $120.13 billion allocated to CapEx, producing $10.56 billion in FCF.

While Oracle has negative net liquidity and negative FCF, the combination of Google, Microsoft, Amazon, and Meta tells the opposite story. Together, they hold $339.15 billion in cash and short-term investments and another $119.16 billion in long-term investments. After accounting for $143.76 billion in long-term debt, they still have a net liquidity position of $314.55 billion while generating $536.73 billion in operating cash flow and producing $206.97 billion in FCF. Bears can point to Oracle all they want, but Oracle’s situation does not impact Amazon, Meta, Microsoft, or Google and it does not change the trajectory of the AI revolution.

I also believe many bears have not been reading the earnings calls. If they had, they would see the AI narrative remains firmly intact. Don’t worry I’ll do the work for them:

MSFT

• MSFT guided to increase total AI capacity by 80%+ this year and to roughly double total datacenter footprint over the next two years

• MSFT highlighted a new flagship AI datacenter expected to scale to 2 gigawatts and go online next year

• Reported deploying the first large-scale cluster of NVIDIA GB300s and improving token throughput for GPT-4.1 and GPT-5 by 30%+ per GPU

• Azure AI Foundry scale of ~80,000 customers

• Commercial RPO increased 50%+ to nearly $400B, with a 2-year weighted average duration

GOOGL

• Reiterated a full-stack AI approach and highlighted scaling both NVIDIA GPUs and Google’s TPUs

• Announced shipping A4X Max instances powered by NVIDIA GB300 to Google Cloud customers

• Gemini processing 7B tokens per minute via direct API use

• Gemini app 650M MAUs with queries up 3x QoQ

• Rolled out AI Mode globally across 40 languages, scaling to 75M+ daily active users with Search

• 70%+ of existing Google Cloud customers use AI products as they emphasized larger deal momentum

• GenAI model product revenue growth 200%+ YoY

• Launched Gemini Enterprise 2M+ subscribers across 700 companies

• Google Cloud backlog grew 46% QoQ to $155B

AMZN

• AWS grew 20% YoY to $33.0B in Q3 (re-acceleration)

• Project Rainier launched a large AI compute cluster with 500,000 Trainium2 chips to build & deploy Anthropic’s Claude models

• Announced Amazon EC2 P6e-GB200 UltraServers using NVIDIA Grace Blackwell Superchips for training/deploying very large models

• Backlog/RPO (AWS) to $200B with additional deal activity after quarter-end

META

• AI recommendations drove engagement with 5% more time spent on Facebook and 10% on Threads in Q3 attributed to recommendation improvements; strong video momentum; and Reels scale commentary

• More than 1B monthly actives already use Meta AI, with usage rising as model quality improves

• Meta described capital deployment priorities as centered on AI products/models/business solutions and outlined steps to increase capacity

• Meta highlighted the scale of business messaging and the goal of using Business AIs to help businesses automate/sell/support at low cost

ORCL

• RPO at $523B, up $68B sequentially and up 438% YoY

• RPO to be recognized in the next 12 months grew 40% year over year

• 211 live and planned regions worldwide

• More than halfway through building 72 multicloud datacenters embedded inside AWS, Google Cloud, and Microsoft Azure

• The multicloud database business is up 817% in Q2

• All top-five AI models are available in Oracle Cloud, including OpenAI, xAI, Google, and Meta models

• Cloud revenue at $8B (up 33%) now accounts for half of Oracle’s total revenue

• Cloud Infrastructure revenue at $4.1B, up 66%, with GPU-related revenue up 177%

• Cloud database services up 30%; Autonomous Database up 43%; multicloud consumption up 817%

At the end of the day, the AI bear case increasingly depends on taking a company-specific funding decision and projecting it onto an entire technology cycle that is being funded very differently by the companies actually leading it. Oracle may have chosen a more aggressive balance sheet path to accelerate capacity which creates real execution and timing risk but it does not invalidate the broader thesis. The hyperscalers and platform leaders are not hoping AI works as they are actively monetizing it today. We are witnessing the hyperscalers expand backlog and remaining performance obligations, and converting infrastructure investment into revenue growth and operating cash flow in real time. If someone wants to debate valuation, competitive dynamics, or the pace of demand, I’m all for it but the lazy narrative that “CapEx won’t earn a decent return” ignores what we have already witnessed since 2021. The companies investing the most aggressively are the same companies expanding revenue, widening cash generation, and strengthening strategic moats.

Oracle is not proof that AI is a bubble. At most, Oracle is proof that funding choices matter and that execution matters. Meanwhile, the builders are telling you, quarter after quarter, that demand is still ramping, capacity is still constrained, and the opportunity set is still early. So yes, thank you AI bears for the cheaper prices and the recycled fear narrative. I’ll keep reading the filings, listening to the calls, and following the cash because when this cycle is judged in hindsight, it won’t be decided by who posted the best skepticism on TV. It will be decided by who built the infrastructure, captured the workloads, and compounded cash flows over the next decade.

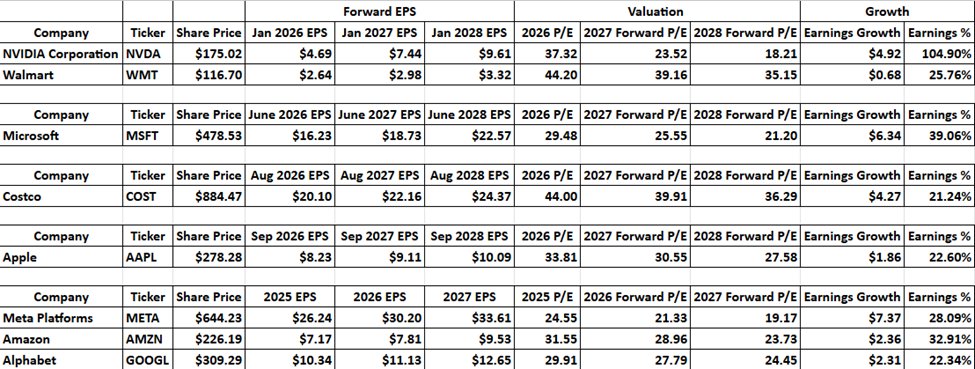

The reality is that the AI Bears just made great companies such as $NVDA, MSFT, AAPL, META, AMZN, and GOOGL cheaper on a forward basis. Below is a table I constructed based on the current fiscal year and the next two fiscal years. NVDA, WMT, MSFT, COST, and AAPL do not report on calendar years so you will see Jan 26, June 26, Aug 26, and Sep 26 to represent their current fiscal years then the next two years of consensus estimate projections to showcase the forward growth rates. META, AMZN, and GOOGL report on a calendar year so it will be a traditional 25,26,27 for the years.

Currently $WMT trades at 44.20 times Jan 26 earnings and 25.15 times Jan 28 earnings with 25.76% of EPS growth over the next two years. $COST trades at 44 times Sep 26 earnings and 36.29 times Sep 28 earnings with 21.24% EPS growth.

I am welcoming the ability to add to my positions in NVDA at 37.32 times Jan 26 earnings with an expected 104.90% EPS growth over the next two years which puts NVDA trading at 18.21 times Jan 28 earnings. NVDA is effectively a value stock here.

Investors are also able to add to META at 19.17, AMZN at 23.73 times, and GOOGL at 24.45 times 2027 earnings. MSFT is trading at 21.20 times June 28 earnings while AAPL is trading at 27.58 times Sep 28 earnings.

There are always pockets of the market that are expensive but its not lurking within the financials of NVDA, META, AMZN, MSFT, AAPL, and GOOGL. If we experience a continued drawdown these companies will get even cheaper on a forward basis so thank you AI Bears for allowing me to pick up more shares of companies I was planning on adding to anyway at lower forward valuations. In the short-term your help is always appreciated, and in the long-term I believe your likely to miss out on a tremendous amount of appreciation.

@amitisinvesting @KrisPatel99 @RealMattMoney @Futurenvesting @FunOfInvesting @Kross_Roads @StockMarketNerd @sam_badawi @dhurstell @DivesTech @fundstrat @ChrisCamillo @altcap

English

@chadbrocheese Hey Luda, I'm unable to send you a message due to your restrictions. Shoot me a DM and I'll send you the link.

English

I just documented Palantir co-founder's complete AI investment framework.

(7 tiers, $5 trillion market, specific stock picks)

Most investors chase AI stocks without understanding the ecosystem structure.

They buy random AI names...

Follow hype without strategy...

Miss systematic opportunities...

I went the research direction.

Just compiled the complete system revealing:

↳ Joe Lonsdale's 7-tier AI framework (energy to applications)

↳ Specific stock tickers for each investment tier

↳ Why Tier 5 applications offer best opportunities (but most are private)

↳Portfolio allocation strategies across risk levels

↳How infrastructure plays benefit regardless of AI winners

This isn't speculation - I'm showing actual framework from Palantir's co-founder who invests hundreds of millions in AI companies.

The most important insight?

Most best opportunities are in Tier 5, but you need public alternatives.

Want the full AI investment research document?

1. Connect with me

2. Comment "AI"

I'll send it directly to your DMs.

PS - This isn't about "AI hype trading." It's about systematic framework thinking for the biggest wealth creation event of our lifetime.

English

@AskRobinhood

RH Legend seems to be down, watch list & positions not loading, account balance & % change not loading 😬

English

luda retweetledi

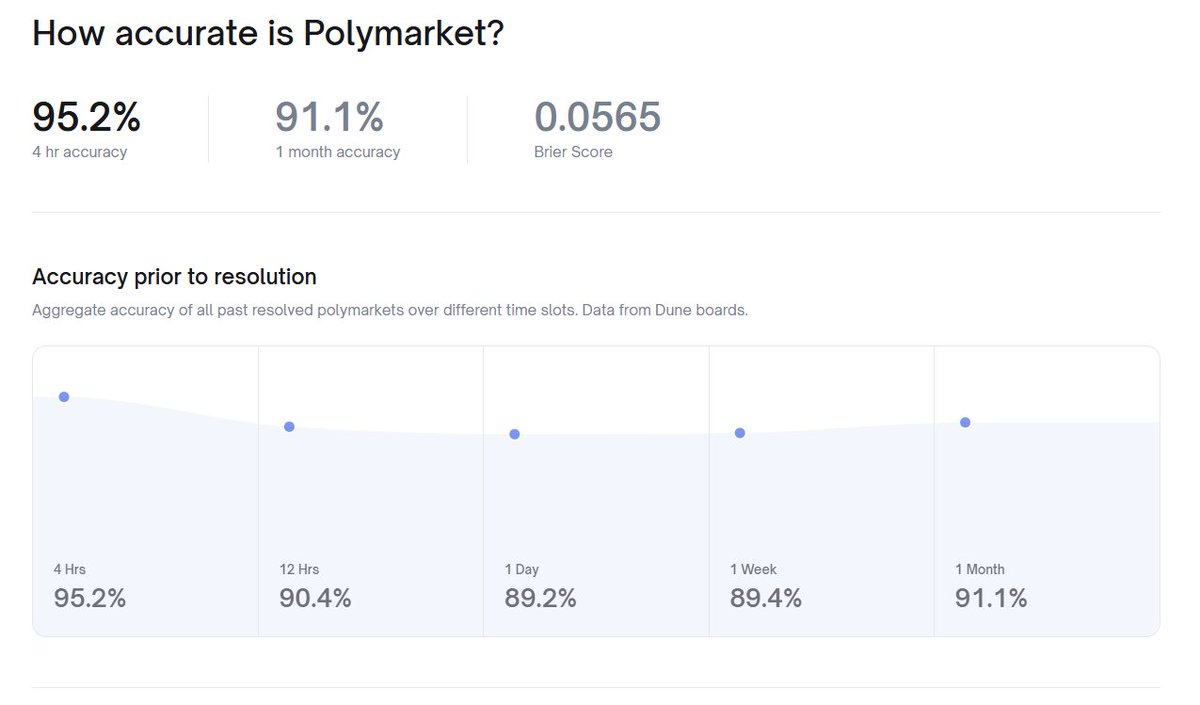

Polymarket’s data shows how close they already are to ‘truth in real time.’

Across thousands of markets, accuracy sits at 91% even a month before resolution and 95% just 4 hours out

The crowd really does know and quantify the odds.

English

luda retweetledi

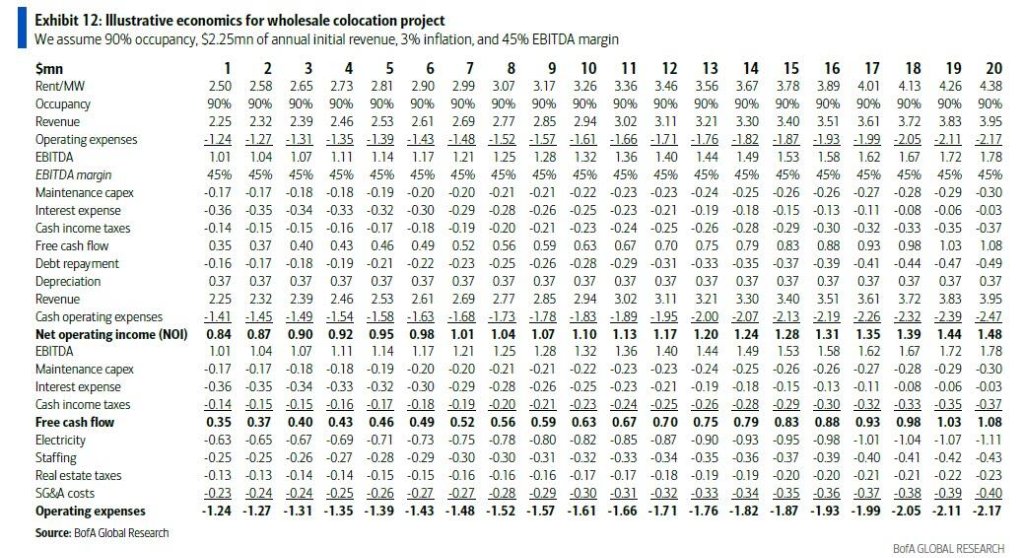

BofA: Why is global capital pouring into the data center industry?

1. Initial Investment:

Building a 1-megawatt (MW) data center requires approximately $2 million for land acquisition and power connection. The cost of the “powered shell” — including construction, electrical/mechanical systems, and cooling infrastructure — is around $11 million. In total, the capital expenditure per MW amounts to roughly $13 million.

2. Revenue and Profitability:

Each MW can generate $2–3 million in annual rental income. After deducting operating costs — including electricity (average U.S. industrial rate of $0.08 per kWh), labor (about two full-time employees per MW), and property tax (around 1% of asset value) — the EBITDA margin typically reaches a stable level of 40–50%.

3. Investment Returns:

Assuming a 20-year holding period and a project financing model (loan-to-value ratio of 46%, debt interest rate of 6%, and cost of equity at 10%), the project’s internal rate of return (IRR) can reach 11.0%. This represents a highly attractive return for infrastructure investors seeking long-term, stable cash flows.

English

luda retweetledi

J.P. Morgan has upgraded Dr. Parik Patel to 'Overweight' after his Christmas Dinner

English

luda retweetledi

I never talk about controversial topics like crypto at Christmas dinner. Instead, I prefer to stick with safe topics like politics and religion.

English

luda retweetledi

luda retweetledi

I’m on the 5th booster watching Tiger King 4. Ellen is President. The camps are for our own good. I’m excited about our day of sun next week. Everything is good.

English