contango2019 retweetledi

contango2019

24 posts

@DeepIceValue Actually both Mohnish and Li Lu bought MU a couple of years ago

English

Why arnt Buffett $BRK.B or Li Lu buying $MU, but both bought $GOOG instead?

English

为何我说这次不是buy the dip 不是什么跌了都要抄底。

这就是领导应当承担的责任和价值

微软拿了整整三年时间、砸下巨资做Copilot,结果被Claude一天就彻底颠覆。

再对比一下印度小哥和华人老法师的差别

Intel新CEO陈立武上任后,公司从濒死到股价翻倍连创新高

而微软CEO Satya 呢?最早入股到chatGPT一手好牌打的稀烂跌了30%。

Claude for Word今天一上线Office的未来已经改写。 这种本地编辑AI协同办公的丝滑感,共享上下文完全打击使用痛点。

我现在是庆幸自己从来就没好好学会怎么勇word excel和ppt。

Tigris 会讲课教授是好老师@tig88411109

看懂这个就知道不是每个股票都能去追高或者抄底的。 这也是我不买 $MSFT 这种创始人一个都不在的职业打工人当CEO的公司股票的原因。 应该把微软最大的危机讲清楚了。当然如果能如CEO说,压对“AI代理就是新APP” 路线转型,或许会有最大的弹性,目前还看不到可能性,

中文

contango2019 retweetledi

Warren Buffett measures the progress of his investments by asking ONE question:

𝐇𝐚𝐯𝐞 𝐭𝐡𝐞𝐢𝐫 𝐦𝐨𝐚𝐭𝐬 𝐖𝐈𝐃𝐄𝐍𝐄𝐃 𝐝𝐮𝐫𝐢𝐧𝐠 𝐭𝐡𝐞 𝐲𝐞𝐚𝐫?

Not maintained. 𝐖𝐢𝐝𝐞𝐧𝐞𝐝.

That is an important distinction.

There’s been a lot of discussion about SaaS names being cheap. $ADBE at 10x. $CRM at 12x. Attractive on the surface.

But before jumping to valuation, ask Buffett’s question first.

Have their moats widened in the past year?

For most, the answer is no. And that is a critical distinction that many investors may be neglecting.

Yes, AI could change this. The implementation of AI has the potential to widen the moats of some SaaS businesses. Yet, that is not clear right now.

But presenting a case that these companies are great investments simply because they trade at low multiples misses the point entirely.

Think about $GOOG. The stock traded down to a 15x multiple — despite being an extraordinarily wide moat business, an AI beneficiary, and a leader with massive distribution across every layer of the tech stack. That’s a very different conversation.

So why does $ADBE at 10x or $CRM at 12x deserve your capital when you can invest in businesses whose moats continue to widen?

That’s exactly why many intelligent investors are choosing to stay away.

It’s not that the value isn’t there on paper. It’s that the burden of proof hasn’t been met. Capital tends to flow toward disruptors — not toward the ones perceived to be disrupted.

Could there be a large turnaround? Of course. But potential doesn’t mean the risk is worth taking or that you should try to catch them on their way down.

I’m all for buying during peak fear. But buying $ASML at $600 or $GOOG at $150 is fundamentally different than buying $ADBE or $CRM today.

One is fear obscuring a widening moat. The other is a low multiple on a moat that may be quietly narrowing (or at the very least, not widening).

Those taking a leap of faith in some of these SaaS names may end up doing very well — and they should be rewarded if they are right! But don’t frame it like this is a no-brainer situation, because it isn’t.

$IGV

English

contango2019 retweetledi

@stockpickerspb @ManuInvests @wholemars That’s correct. That’s why I’m always asking myself what exactly Uber can offer and whether those value propositions can be easily replicated by competitors

English

$UBER

@wholemars is correct that Uber’s AV partnerships are not a moat. Partnerships are rarely ever a moat, but instead a RESULT of a moat.

Uber’s moat, which is much more powerful than a collection of partnerships, is the platform. This includes a massive network and ride data, powering its incredible demand prediction, matching, dispatching, and pricing models at an unmatched scale.

AV companies recognize the value proposition that Uber offers, which is why we see these partnerships.

Uber is in a position of power as we enter the AV transition, with an amazing management team to navigate through it.

Whole Mars Catalog@wholemars

English

@FluentInQuality Estimate FCF for big tech is really tricky - i would rather use a normalized fcf as the current capex level is unsustainable

English

Everyone is saying $MSFT is cheap after the drop.

Run the reverse DCF and think again.

The market is pricing in ~16% FCF growth for 10 straight years just to justify today's price.

That's not a bargain. That's a bet.

Worth it or not?

English

@ErnestWongBWM Not much barrier in AV Technology. Uber can always choose to own their fleet as a downside protection

English

We studied $UBER and while there is value in the network, ultimately couldn't see how they thrive in an AV world where suppliers get increasingly consolidated and Uber does not own the core technologies

Please tell me why I'm wrong.

English

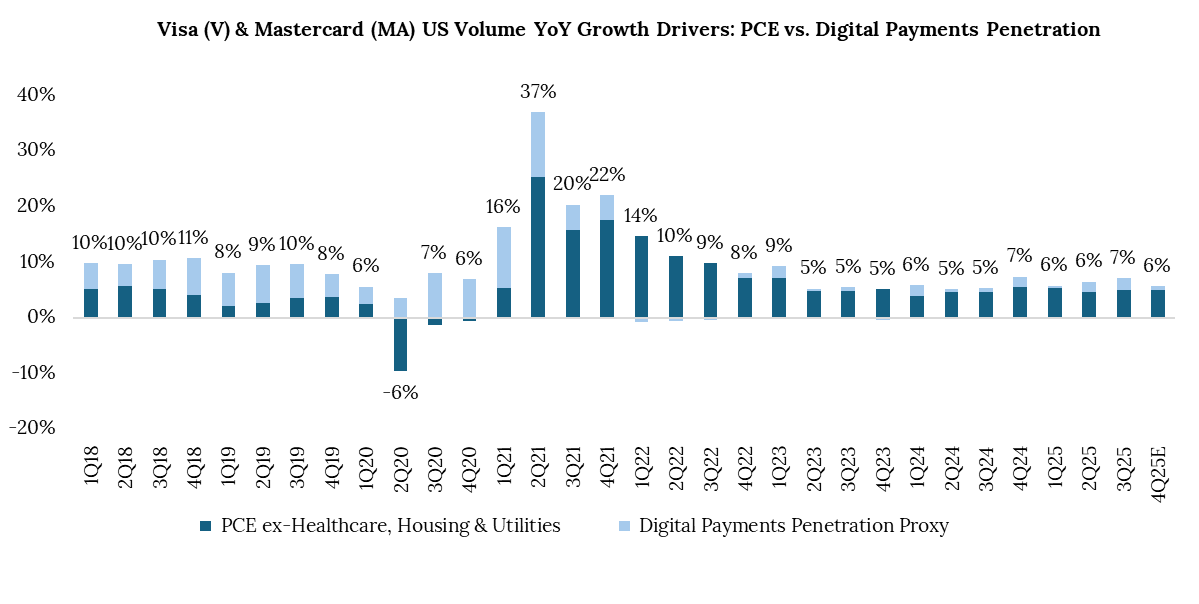

If you think about $V and $MA long-term volume growth drivers, it’s been a combination of personal consumption expenditures (PCE) — or the amount consumers are spending on goods and services regardless of what payment instrument they’re using — and digital payments penetration increasing — or the increasing number of consumers using digital/card payments versus cash or check (or a cardholder who already has a card using it for a higher percentage of their purchases over time).

For a long time, $V / $MA volume growth was more evenly split between end market / PCE growth and increasing digital penetration. This allowed them to sustain higher than industry growth (ie PCE) — typically ~2x that rate — and allowed both to maintain a certain level of growth in cyclical downturns (PCE falls but digital penetration gains carry more weight so they still grow) but given growth has converged more to PCE growth and digital penetration is going to be less of a driver moving forward, $V / $MA volume growth will more closely reflect PCE, which means it’ll be more heavily tied to macro economic up/down cycles — and generally, will grow slower going forward assuming PCE remains ~stable.

I hope this helps.

English

Interesting to decompose $V & $MA US volume growth into PCE growth and digital payments penetration gains (calculated by subtracting adj. PCE growth from $V & $MA growth). I adjusted PCE to exclude healthcare, housing & utilities since these are mostly non-addressable for typical consumer card payments.

In the few years leading up to Covid, digital payments penetration accounted for ~57% of $V & $MA's US growth. Since 2022, it's <10%.

At $V's Feb 2025 investor day, it stated US penetration was 60%+ (my rough math puts it 75%+). This demonstrates that $V & $MA US growth is mostly a PCE proxy now.

English

@Ahmedinvests Waiting time, reliability, and then coms to price. You don’t want to wait for 10mins for a ride to arrive and meet some rude drivers.

English

I hold $UBER and wanted to challenge my own thinking, so I did something simple.

Asked almost all my friends: do you ride with Uber or Lyft? Every single time the answer was "whatever's cheapest."

That's the tension I'm wrestling with on the mobility side.

Look, I still think they have a real business moat. Network effects are massive and AVs will probably partner with them for distribution.

From an investor perspective the competitive advantages look solid.

But as a customer, why would I care if I ride with $Uber or $Lyft or any other cheap alternative? The loyalty just isn't there like it is with other platforms.

This is why you should do this analysis yourself. Stop thinking purely from an investor view about moats and possibilities.

Actually ask your friends what they use and why. You'll find the customer level moat is way weaker than the business level moat suggests.

Mobility is tricky because price is the ultimate decision factor for most riders. $Uber's strength is the network effects keeping them competitive on price and availability, plus being the default partner for AV deployment. But customer switching costs? Basically zero.

That's the battle they need to win. Not just being the platform AVs partner with, but giving customers an actual reason to choose them beyond "they happened to be cheaper today."

Because right now most people just open both apps and pick the lower price.

Stress test your own holdings. The gap between investor thesis and customer reality can be pretty eye opening.

GIF

English

13Fs come out mid February

I’m still think it’s either $META or $ADBE

More likely it’s $META because Bill hasn’t historically bought software stocks but frequently dabbles in big tech

Aria Radnia 🇮🇷@ariaradnia

Bill Ackman says he’s “finishing due diligence on a company [they’ve] really wanted to own for years, now available at a bargain price” My bet is either $META or $ADBE

English

Disclosure: I am a long $FICO, $NFLX, and $HESAY. I have no remaining position in $V or $MA. This is not financial advice. My investment decisions are based on my own risk tolerance. Past performance is not indicative of future results.

I’ve decided to exit $V and $MA and reallocate that capital into $FICO.

I have zero interest in managing four different "battleground" positions across $NFLX, $FICO, $MA, and $V. I’d rather consolidate that energy into my highest-conviction ideas and own more of what I believe is the best horse in the race.

On the Q1 $FICO call, management reiterated their fiscal 2026 guidance, but they also explicitly noted that they will revisit and potentially update those numbers on the Q2 call. In my view, the current setup is a classic case of management being conservative. I’m choosing to size now rather than waiting to see if that raise materializes in a few months.

90% of the portfolio is static. This 10% shift is just about sharpening the portfolio and ensuring my capital is where I’m personally seeing the most improvement.

English

@bobspaysubstack I think at least half of the BNPL replies on V/MA payment network

English

Regulatory firestorm for the credit card industry $V and $MA

Okay, so my posts have been a bit meandering today, but here’s a recap:

President Trump has thrown his full weight behind the credit card competition act, which also had the support of his vice president in the past. I have no way of handicapping whether this will pass or not, but the odds are certainly higher after today and a vote almost certainly will happen in the Senate. The purpose of the bill is to drive down the cost of credit interchange by allowing merchants the option of processing a credit transaction over two unaffiliated networks. The technical implementation of such a thing would likely be complex and lengthy.

Lower credit interchange would have far reaching consequences. Significantly pared back or eliminated rewards programs is the most obvious. On the other hand, it would be a big boost for PSPs $PYPL $XYZ $TOST $SHOP that charge a gross fee to the merchant and interchange is a cost of goods sold, driving up the transaction margin.

Also sitting out there is the threatened 10% cap on credit card interest rates. Still think that is unlikely to go anywhere but $JPM certainly painted a dire picture of what the industry would look like if it happened (hint, a significant reduction in access to credit for a large portion of the population).

Right now, it looks like the ire of the Trump administration is squarely focused on the credit card industry. If you’re a bull you’re relying on President Trump’s preferred style of negotiation which is to make big threats to extract some (small) movement and claim victory. I still think that’s the more likely outcome.

Needless to say, if both of these measures passed or were implemented the industry would cease to exist anywhere near its current form.

English

What stock will be next all-in opportunity like $TSM, $META, $GOOG, $UNH were in recent years?

English

@QualityInvest5 Nice summary. I think would be good to list out Uber’s key value propositions as well, ie utilization optimization and demand aggregation

English

Every major Robo-Taxi partner tied to Uber, where they operate, and their autonomy level:

Waymo owned by Google $GOOGL

– Austin, Atlanta (Uber partnership)

– Level 4 autonomy

Wayve backed by $MSFT $NVDA $UBER and SoftBank

– United Kingdom (launching 2026)

– Level 4 autonomy

WeRide $WRD

– Abu Dhabi, Dubai (exclusive to Uber)

– Level 4 autonomy

Pony(.)ai $PONY

– Middle East and international markets (exclusive to Uber)

– Level 4 autonomy

Avride owned by Nebius $NBIS

– Dallas (Uber partnership)

– Level 4 autonomy

BYD $BYDDF

– United Kingdom (launching 2026)

– Level 4 capable vehicles through OEM partnership

Zoox owned by Amazon $AMZN

– San Francisco, Las Vegas (commercial operations)

– Level 4 autonomy

And then there’s the so-called “robotaxi leader”…

Tesla $TSLA

– Limited area of Austin, Texas

– Level 2 autonomy (supervised)

English

@guan_rui_ Do you think NFLX is a better core growth position compared with Meta? I think NFLX is more predictable as they constantly grows their size and content pool and no need incur massive capex as Meta. I am thinking to allocate 10% as core growth and look to hear ur thoughts

English