A Belgian Investor

439 posts

A Belgian Investor

@d_schau

CFO. Married. Father of 3. Investor since 2023. Hoping to bring value to you.

België Katılım Şubat 2014

2.4K Takip Edilen313 Takipçiler

📣 MILESTONE 📣

In the summer of last year, I took the big step of resigning from my position as an equity analyst at Baillie Gifford in Edinburgh after two fantastic years and moving back home to Denmark.

Ever since I was a teenager, I’ve had the goal of one day running my own investment fund. This was to happen before I turned 30 and after gaining more than a decade of stock picking experience. As soon as I moved home, I set the project in motion. Due to extended preparations and countless discussions around structure, setup, and registrations, I ended up a year behind schedule, but now it’s finally time to launch!

Sung Partnership is officially open for investment.

Sung Partnership is a small, private investment company managed by Sung Capital, with the simple ambition of generating attractive long-term returns through concentrated stock picking in overlooked corners of the global equity markets. If you’ve followed my writing here on the platform, you probably already know how we do things. The fund’s portfolio will typically consist of 5–15 companies where we identify significant mispricings relative to intrinsic value — often in nano/micro/small caps, special situations, and other companies that large pools of capital (hedge funds, mutual funds, and pension funds) cannot or will not consider.

We don’t engage in macro forecasting or market timing. The focus is exclusively on fundamental investing with a wide margin of safety and protection against permanent capital loss.

The partnership is built on a simple principle: the manager (myself) invests side by side with partners with virtually my entire liquid net worth.

The first half of the portfolio has been established, and additional positions will be added throughout the year. A professional board has been appointed, and I’m working on building the right investor base until we eventually close to new capital.

It’s very important that potential partners are aligned with our investment method. I’ve written a short and personal e-book about my investment method and how I work on a daily basis which you can find on sungpartnership.com

If you’d like to learn more about the partnership, you’re always welcome to reach out.

English

I'm probably the only person on fintwit with a negative return this year (about -2-5%), but let's look ahead to 2026. As we say in Germany Guten Rutsch! (Good sliding)

English

Merry Christmas 🎄🌟

What a year. Some stuff went surprisingly well (Iron Ore, Steel, Platinum) while other lagged (mostly oil). I go into 2026 with record high cash, a clear mind and fire in my eyes.

Greetings from Cyprus

English

Zoomd Technologies ( $ZOMD.V | $ZMDTF ) : A dive into the business model, valuation, and forward outlook.

Capital light compounder or value trap? Read it here (free): underlyingvalue.substack.com/p/zoomd-techno…

English

@kakashiii111 I can only wonder how many retail shareholders are (un)aware of these dynamics.

English

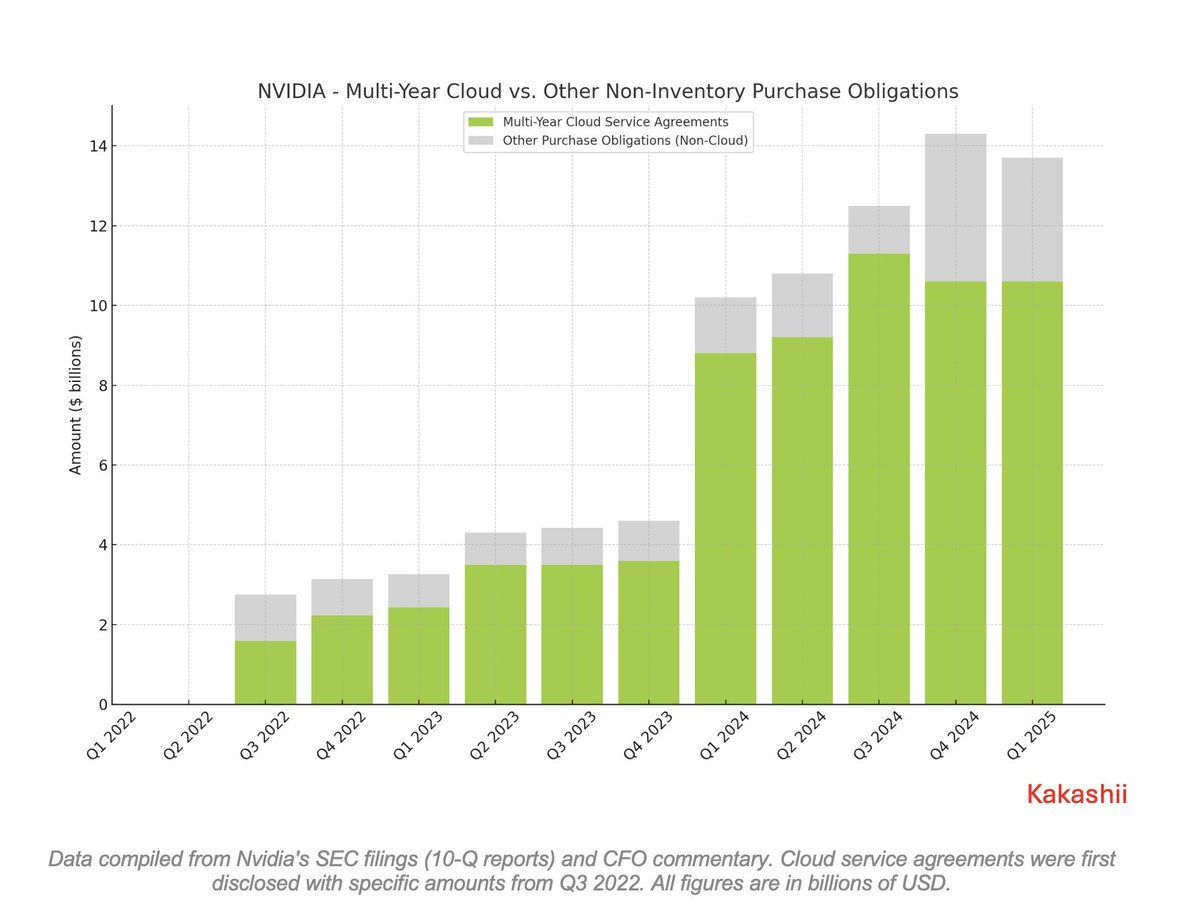

Nvidia Presents the Cloud Credits Boom

NVIDIA’s cloud credits method began in the second half of 2022, when they announced partnerships with “cloud service providers” to offer cloud-based infrastructure for training AI models—just in time for ChatGPT’s launch and the AI FOMO frenzy.

Why Did Nvidia Come Up With This?

Nvidia realized their own cloud services might not make money quickly and would require significant time and investment to grow. So, by partnering with cloud companies, Nvidia lets these companies join the AI party by scoring GPUs without needing to come up with the cash.

How Does the Cloud Credits System Work?

Nvidia “sells” these GPUs to the cloud companies, but instead of getting paid cash right away, Nvidia receives something called cloud credits. These credits allow Nvidia to “buy” services from those cloud providers later.

When Nvidia “sells” GPUs to cloud providers and gets cloud credits instead of cash, it essentially means Nvidia is recording a receivable or an asset—a kind of IOU or prepaid balance with those partners.

These credits represent Nvidia’s right to use services from the cloud providers later—like a trade or barter arrangement, not immediate cash income.

Accounting Perspective

From an accounting point of view, Nvidia books revenue from the GPU “sale”, but simultaneously it creates an obligation to consume cloud services in return.

Then, the credits become an obligation for Nvidia because they must eventually “pay” for services by using those credits. It’s not pure profit until the services are actually consumed or settled.

This approach helps Nvidia show revenue growth now, while cash flow or actual costs get balanced over time as cloud services are used.

What Is the Scale of Nvidia’s Use of This?

In just 2.5 years, these cloud credits jumped from $1.6 billion to over $10 billion per quarter—a 10x surge (!). That’s the NVIDIA magic: a clever way to fuel the AI narrative by looping capital through cloud partners while booking revenue on the other end.

English

@finance_schmidt @aktien_max Their entire reporting pack is intentionally misleading (or at least presenting things in the best possible light).

That tells you all you need to know about managements integrity, and attitude towards shareholders.

Cheap for good reasons, imo.

English

@aktien_max ...Jahreszericht darauf hin, dass sie die Mietzahlungen nicht vom FCF abziehen. Aus Transparengründen sollten das meinem Empfinden nach alle nach IFRS berichtenden Unternehmen machen, da irreführende Begriffsverwendung.

Deutsch

Hm... ob es nachhaltig ist, dass $HFG nur zum 3,2x des Free Cashflow notiert? 🤔

MAX RAHN@aktien_max

$HFG Jedes Mal, wenn ich mir HelloFresh ansehe, kann ich es nicht glauben: der Laden macht einfach über 7 Milliarden € Umsatz pro Jahr. Das ist mehr Umsatz als bei Vonovia $VNA.DE 👉 Meinst du, der Markt unterschätzt HelloFresh deutlich?

Deutsch

@evfcfaddict @aktieblogg @Secrets4stocks @stonkmetal @AravacaCap @ObscurValuation @SebKrog @FinSkeptic @NoBrainerStock @unfixed_income @diegobmilano @wusatiuk @Franfra51045228 @HindsightCapLLP @ReturnsJourney @SteigerwaldValu @AmsterdamStock Thanks for all the effort you put into organizing it, Andy!

English

A few $FOUR excerpts from CFO Chris Cruz at KBW Fintech Payments Conference

English

A Belgian Investor retweetledi

Ummm... $NVDA is currently trading at 27.6x sales, which means the "market" expects $NVDA to pay it, as a dividend, 100% of its sales, every yr, for the next 27.6yrs. I'll remind you of this quote from Sun Microsystems' CEO when the dot.com bubble burst in 2002.

Laigt Bringer@Jespabe

@GordonJohnson19 Everyone is bearish on AI today. Wtf are you saying?

English

Today we reached 10,000$. I'm Not sure we can reach the goal of 120,000 but I will do my best to try. Our people need all the help they can get, the situation is quite dire

✙ Constantine ✙@Teoyaomiquu

Hello everyone, friends, followers, and supporters of Ukraine. Today I'm starting a new fundraiser for $120,000 to help Ukraine with engineering equipment, heavy trucks with cranes, and excavators. (Donation link at the end.) Please take a minute of your time to read and watch the video to understand why this is important. Also, please repost, like, and comment. Unfortunately, the situation on the front line is far from ideal. Our units are severely understaffed, and Russia continues slowly grinding us down.One of the key reasons I focus on engineering equipment is because it's often an overlooked low-hanging fruit that helps solve manpower shortages, saves defenders' lives, and saves millions of dollars. To put it in numbers: 1️⃣ Building a proper bunker for an infantry platoon takes 2 weeks and 8 people without an excavator. With an excavator, it takes around 3 days and 3 people, effectively reducing toil 9 times. 2️⃣ Unloading a vehicle full of 6-meter logs for fortifications takes 6 people and 4 hours by hand. With a crane, it takes 2 people and less than an hour, reducing toil 24 times. I can't emphasize enough how important and helpful this equipment has been. It might not look exciting, but it's the backbone of the Ukrainian Armed Forces. The more we can supply, the more lives we can save. Thank you for reading. I'm grateful that you made it to this point. Donation link🔗: paypal.com/donate?campaig…

English

@TheREALMADriD94 I'm going to assume they have these institutions sign NDA's. And in any case, these meetings are conducted within a closed setting.

EVO's concerns will be centered around disclosure and confidentiality, not their time spent/invested.

Again, this is just my assumption.

English

Linton noted that Evolution holds "more than 500 investor meetings per year.

Please, make one more and let retail ask questions. It would only increase the number of meetings by 0.2%, while providing great value for everyone.

Wolf of Harcourt Street@wolfofharcourt

Q&A with $EVO Investor Relations thewolfofharcourtstreet.com/p/q-and-a-with…

English

Profitlichschmidlin blog article on distributors with a lot of interesting insights on $AZE.BR and their moat:

profitlich-schmidlin.de/50x/?trk=feed_…

English

One major difference between large caps and microcaps is that, in large caps, the main drivers of your returns are typically: industry > business model > management.

In microcaps, it’s the opposite: management > business model > industry.

English

@wolfofharcourt Would you mind sharing this list of topics?

English

$EVO interview - quick update

I’ve received quite a few messages asking about this, so here’s the sequence of events:

1. Their IR team reached out to me (not the other way around), inviting me to ask any questions I might have.

2. I accepted, and after some back and forth, we agreed to do a Q&A session.

3. I sent them a list of topics I wanted to cover in advance, focused on what I believe truly matters to investors, rather than the usual questions analysts ask on conference calls.

4. Since sending that list, there’s been complete radio silence. I’ve followed up twice with no response.

Draw your own conclusions.

English

My only takeaway from the large-cap tech earnings AH is that these are no longer the asset-light darlings where you can assume all growth is good growth.

$GOOG spent 23% of sales on capex this quarter, and $MSFT came in at 25%. You really have to trust that management knows what they’re doing when deploying $70–100B of capital annually. Or whatever number.

It’s never been done at this scale before. And we all know how the story usually goes for companies that go through a period of massive asset growth without the ROIC to back it up.

English

@PiyDW @weary_centurion You don't seem to understand 'your margin is my opportunity'.

You should look at gross margin and not take rate.

Lowering take rates makes perfect sense in a volume driven sector.

English

@weary_centurion this is what companies in weak positions do. Thats why funds look for companies increasing their GM/take rates etc.

English

$PYPL

No…

PayPal explicitly addressed the ongoing take rate compression in both the prepared remarks and Q&A, framing it as a deliberate, strategic trade off to drive volume growth, merchant loyalty, and long-term profitability

Not a sign of weakness

Fiscal.ai@fiscal_ai

PayPal reported its lowest transaction take rate ever this quarter. Is this a headwind shareholders should be worried about? $PYPL

English

@FinanceFilosoof Er is niets gemakkelijk aan.

Het is weinigen gegeven om de nodige discipline te behouden. En dan spreek ik nog niet over zaken als mentale weerbaarheid bij tegenslagen,..

Mensen zijn mensen en geen machines. En het leven gebeurt, en zit vol ongeplande zaken.

Waardeloze take

Nederlands

100.000 euro per jaar sparen is best makkelijk eens je al even in de FIRE-community zit.

De reden?

Geld verdienen is een exponentieel proces. In het begin is het vechten om je eerste 10.000 euro per jaar te sparen. Maar dan begin je op te bouwen, dalen je uitgaven, begin je meer te werken in extra jobs, stijgt je inkomen en voordat je het weet heb je na enkele jaren je eerste 50.000 euro gespaard.

En dan gaat het snel.

Je kan beginnen ondernemen met dat geld, meer risico nemen, je inkomsten stijgen en twee jaar later ga je aan je eerste 100k vermogen zitten. Dan kan je beginnen investeren in kapitaal intensieve verdienmodellen. Dat geld beleg je in je bedrijf of privé en je blijft gewoon doorgroeien.

Als je dan ook nog eens dat kapitaal hebt, kan je daar nog een turbo opzetten door geld te lenen. Dan bouw je vastgoedprojecten, lever je ze op en daar pak je dan ook tienduizenden euro’s op. Of je belegt het en dan begint opnieuw het spel van exponentiële groei.

Het moraal van het verhaal?

100.000 euro per jaar sparen is makkelijk eens je beseft dat geld en inkomsten exponentieel groeien. Geld maakt geld. Alleen lijkt het enorm moeilijk eens je vandaag nog maar een paar honderd of duizend euro per jaar kunt sparen. Maar eens je die eerste euro's hebt, zet je ineens een turbo op je verdienpotentieel. Dat is dan ook mijn tip. Zorg dat je zo snel mogelijk je eerste spaarbuffer hebt. De rest volgt dan automatisch als je op dezelfde weg bezig blijft.

Nederlands

@gnufs Great insights, as always.

I have been thinking about the option to split the co in 2. It might be the best way to move forward.

One company to fully focus on grey / black markets and 1 that can serve the white markets.

Probably easier said then done.

English

Evolution's Q3 2025: Quarter in Review

dontdistribute.com/p/evolutions-q…

English

A few thoughts on $EVO's Q3 2025

...some charts, management capitulation and the outlook

English

In case anyone wants to reach out, talk stocks or pay us a drink, we are back at christmas market Schönbrunn Palace on November 14, ~5:00 PM CET together with lots stock picking friends travelling to Vienna from 13 different countries. Can’t wait!

Andy@evfcfaddict

Christmas in Vienna with the microcap gang… @david_katunaric @SebKrog

English

Cutting Evolution Gaming $EVO – A Few Thoughts 👇🏻

I decided to take a small loss on Evolution Gaming today. It wasn’t a big position and I didn’t lose much – around 6% – thanks to having bought in at what I thought was a pretty attractive price. That alone made the decision easier. But I still think it’s worth unpacking what went into it, because the story around Evolution remains fascinating.

When Cheap Isn’t Enough

Let’s start with the positives. Valuation still looks undemanding. When I last valued the business, it was trading around 11x free cash flow, which would now put it at roughly a 10% FCF yield. On a more conservative basis – only counting the "regulated markets" FCF – the multiple comes closer to 30x FCF based on conservative margin assumptions. For a company with Evolution’s business model and clearly leading market position, that’s not expensive.

The business continues to return capital to shareholders, and as long as it’s not structurally declining, those buybacks and dividends should carry investors to decent returns. A rerate to even 15x FCF could do wonders. And when sentiment turns – which it probably will at some point – the stock could rebound quickly. We’ve seen this movie before with Medpace $MEDP recently when expectations were rock-bottom and the stock exploded after a decent quarter (it's close to a double from the lows now), and even with Edenred just this week $EDEN (a 20% 1-day pop after solid results; HSD growth). A single quarter of 8–9% growth could easily trigger a 15–20% move for $EVO too.

Why Sell Then?

So why did I still sell? Because I’ve become more open to stepping away from positions where fundamentals alone don’t tell the full story. The latest outlook and commentary on the earnings call didn’t exactly inspire confidence. There’s a decent chance we’ll see more lackluster quarters ahead and the stock does nothing.

To me, that means dead capital. Even if downside is limited, so is upside – and the opportunity cost starts to matter. If you’re looking for a solid dividend, some buyback support, and a low bar for a turnaround, Evolution might still fit your style. It just doesn’t fit mine right now.

Structural Headwinds – And Why Asia Worries Me

What keeps me uneasy are the structural headwinds that seem more significant than I initially assumed. Asia remains a real puzzle. If Evolution can find effective mechanisms to combat cybercrime activities, that could strengthen the moat dramatically and add another layer to the already strong moat. Same with ringfencing and regulatory compliance – the more complex the infrastructure, the higher the barriers to entry.

But the other side of that coin is clear. Those very efforts create friction for growth and put pressure on margins. And as the latest results show, finding the right balance between compliance and ambition isn’t trivial. Overshoot, and you stifle growth; undershoot, and you risk regulatory blowback.

I'm worried $EVO falls in the "legacy moat" bucket today. A company that clearly is highly competitively advantaged but that lacks reinvestment opportunities to benefit from the moat; the moat protects high ROIC, but if there are no/little reinvestment opportunities to leverage that ROIC, the moat becomes much less valuable.

The New Landscape of Gambling & Entertainment

Another thought that’s been forming recently: competition may now come from directions I didn’t use to consider. Prediction markets, gambling on speculative assets (I just today tweeted about the $2B market cap drop in the Counter-Strike skins market), AND even the stock market itself!

The New York Times this week published an op-ed titled “Gambling. Investing. Gaming. There’s No Difference Anymore.”

The author wrote:

“If it feels as if gambling is everywhere, that’s because it is. But today’s gamblers aren’t just retirees at poker tables. They’re young men on smartphones. And thanks to a series of quasi-legal innovations by the online wagering industry, Americans can now bet on virtually anything from their investment accounts.

In recent years, this industry has been gamifying the investing experience; on brightly colored smartphone apps, risking your money is as easy and attractive as playing Candy Crush. On the app of the investment brokerage Robinhood, users can now buy stocks on one tab, “bet” on Oscars outcomes on another and trade crypto on a third.”

That quote stood out to me. On the same Robinhood $HOOD app, you can buy stocks, bet on the Oscars, and trade crypto – all within seconds. The lines are blurring fast. And of course, every other entertainment platform – TikTok, YouTube, Netflix, gaming, Sora – competes for the same attention span.

I still believe Evolution’s business model is one of the best ever designed. For anyone unfamiliar, I’d recommend the @Speedwell_LLC podcast with Todd Haushalter, which captures just how unique and difficult to run this model is. But it’s hard to ignore that the best days of growth might already be behind the company.

Lessons from a Familiar Pattern

This situation reminds me a bit of my short-lived investment in The Italian Sea Group $TISG. That too looked like a straightforward 10% yield play. But I underestimated the impact of the Bayesian yacht incident – shrugged it off as a non-event – and later realized it wasn’t. Cutting that position was the right call, and the stock’s down another 25% since.

Maybe I’m making a similar judgment call here, and maybe I’m wrong. Again, one good quarter and the stock flies. But investing isn’t about being right all the time. It’s about managing risk, freeing up capital, and positioning yourself for better odds elsewhere.

A Word on Management

One lingering question for me is leadership. At one point today, I genuinely wondered whether the CEO is still the right person to lead the company through this phase. To be fair, he handled the call well – no sugarcoating, direct answers, good grasp of the challenges. But performance has been lackluster for several quarters now. Execution needs to speak louder than words soon.

I’m still keeping an eye on Evolution. It’s a remarkable business with a fortress-like model, but right now, I see more attractive opportunities elsewhere. Cheap can protect your downside, but sometimes it also traps your capital. I’d rather stay patient, keep my optionality, and wait for setups that align more cleanly with both my conviction and my time horizon.

English