DaniCN

151 posts

DaniCN

@dcn000041

Interested in businesses news and investing

Katılım Mayıs 2022

121 Takip Edilen16 Takipçiler

Competition is the reason we never got a SuperApp. WeChat in China is installed by ~95% of the Chinese population.

PayPay is installed by 2/3 Japanese smartphone users, and is about to IPO on Nasdaq.

Go get your alpha with my in-depth research piece:

research.typefcapital.com/p/pre-ipo-shou…

English

$PYPL To be honest, this is such a missed opportunity. The optics were great; positioning the business for the next era of finance. Having a ~20% market share of ALL digital commerce globally, they have about a third of all cards in circulation vaulted (data moat).

- Deals with all major LLM providers to power agentic commerce

- Use the data moat to build the best ads business in the world (knows what you buy and when, and where)

- Generating a lot of cash flow, buying back shares

- Seamless guest checkout solutions

- Severely undervalued

So what went wrong? Simply execution. A word often undervalued when it comes to investing, raw and sheer execution. No matter how well a business is set up, if they can't execute on the opportunities, it's all for naught.

As for what I'll do with my position, I am not sure yet. What I can say for sure is that I am not very excited about the company.

English

@JuanRodrig07 Yes, I run today different Montercarlo simu with the main AI considering slightly net income decline and steady 6B buybacks. The results:

Final multiple for 2031

p10: 2.05x

p25: 2.35x

p50: 2.72x

p75: 3.12x

p90: 3.55x

I'm considering deleting the broker app and X for a time.

English

@QualityInvest5 Try to be a bit more emphatic man... No need to attack other investors... I remember your big mistake with fiserv and not every one reminds you to look anything...

English

For the $PYPL bois

Remember to look at fundamentals next time and be objective, you got this 😉

English

@WagerWizard00 @Kross_Roads @TheLongInvest FCF will be relative flat, at this prices they buy 15% of the float/year. In theory in a couple of years we won't be in red... And I have nothing to compensate neither I can expect multibaggers without making the same mistake of concentration. Somethimes the best is do nothing.

English

@dcn000041 @Kross_Roads @TheLongInvest Haha dude I’m in same bought. It’s was one of three positions for me but it was by far the biggest. But I’ll ride this out. I have a 5-10 year horizon, so I’m def not selling this deep in the red.

English

I want to be make my position clear

I am NOT selling $PYPL

I don’t sell deep under the 200 WMA and being in a position where they could buy half their company right now with their assets

Cash flow guides the price….eventually

English

@Kross_Roads @TheLongInvest Thanks Roy! It was a value trap and we refused to see it, I'm personally trapped, it was my only position, and now I can not do otherwise than waiting, I cannot afford to declare this loss. Apparently I'm now a long investor because I must.

English

I don't disagree with you. The "eventually" is the hard part. With that guidance (which yes, it's sandbagged), it might take a long time.

But I know you have long horizons.

Hard for me to sell here and move on, but the thesis is broken for me personally.

I wish you, and other shareholders, and the organization well.

English

DaniCN retweetledi

$PYPL

I’m writing this ahead of earnings because I’m genuinely debating trimming or exiting PayPal, and it’s not because of the chart, a single quarter’s numbers, or me being impatient about holding time.

This is a thesis check. The business is still solid, but the investment thesis has weakened relative to other opportunities I can allocate into right now.

Basic Earnings expectations (which are fine):

🟢 Revenue: $8.9B (small beat)

🟢 EPS: $1.32 ($0.03 beat)

🟢 Guidance: raised

🟢 FCF: $3.6B

If they hit those, great but honestly, that’s not the core issue. Here's what I'm laser-focused on:

1⃣ SPEED

What worries me is slow execution and delivery on initiatives that should be moving faster. Projects feel like they’re taking longer than expected (e.g., PYPL World, Fastlane, getting Venmo to send money to PayPal, etc.)

Branded checkout is slowing, even if product experience is improving. That's not great. Not my main concern, but I'll put it in the speed bucket.

2⃣ CLARITY

New projects rarely get mentioned outside of the initial announcement and kickoff. Timelines and success criteria are fuzzy at best, and non-existent far too often.

Communication tends to show up only when something is negative, not as a steady cadence of progress updates.

What happened to Fastlane? What about ads? Smart receipts? Did that get scrapped? Etc.

3⃣ MACRO BLAME

The past couple quarters there as been too much macro blame and not enough “here’s what we control + here’s the plan.”

Look, I LOVE the transparency here on showing where you're weak and where there are concerns. But you cannot just say, "Well, it's not good" and then not talk about what you can control, change, or do to address it.

Healthy companies talk about the macro a little, but stay focused on what they can control. Strong companies rarely talk about the macro being weak. You know who does? Weak companies.

WHAT I MUST SEE

Specific updates on key initiatives with real checkposts (what ships, when, and what “working” looks like).

Guidance that actually reflects acceleration in revenue / branded trends (not just cost/efficiency optimism).

Sharper messaging: less “macro did it,” more ownership + execution narrative + measurable milestones.

FINAL THOUGHTS

I’m not looking for perfection. I’m looking for momentum, accountability, and a timeline. If they guide showing acceleration, I will 100% believe this team (since they're conservative on that front). If they tell us a roadmap, TAM, and early results, I'll take that. If they acknowledge the macro, fine. But that should not be the focus. Control what you can control, or your stock looks like PainPal.

English

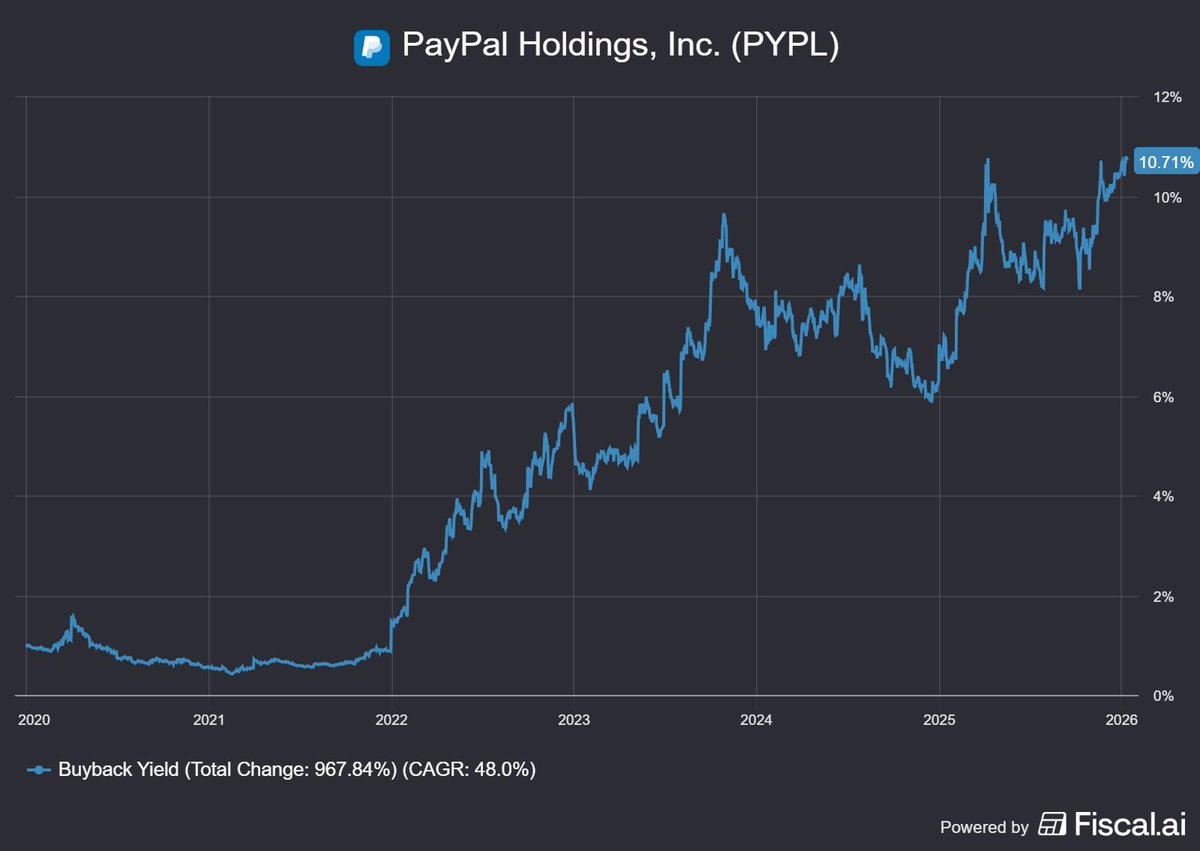

@JuanRodrig07 Realmente no hay un buybacks yield porque ese dinero no llega al inversor mientras la acción y los multiplos pueden seguir comprimiendose... (Lo digo desde la frustración).

Se está haciendo duro sostener $PYPL cuando hasta sus comparables suben...

Español

@JuanRodrig07 @Kross_Roads TBH in the announcement in LinkedIn posted by the Microsoft guy, PayPal plays a minor role and it is only one more player in the copilot checkout...

linkedin.com/posts/paulflon…

English

@Kross_Roads It's been all agentic and Ads lately, which I think both will be successful. The issue is, as you said, that they won't bring any meaningful revenue anytime soon.

We need an update on PayPal World - their website still says 'Coming Late 2025', but nothing yet.

English

$PYPL PayPal + $MSFT partnering for Agentic Commerce is a good thing. PayPal will get a piece of this pie in the future as they're partnered with so many platforms, no matter who wins.

The problem for the stock is that Agentic Commerce is too far away to deliver meaningful revenue any time soon, and also very speculative at this point.

That said, I like that PayPal is continuing to innovate and building for the future. That didn't happen often enough prior to @acce. But to change the direction of the stock, a more near-term shift is needed.

PayPal@PayPal

We’re teaming up with @Microsoft to power their launch of Copilot Checkout, making it easier for shoppers to discover, decide, and complete purchases in one place: newsroom.paypal-corp.com/2026-01-08-Pay…

English

DaniCN retweetledi

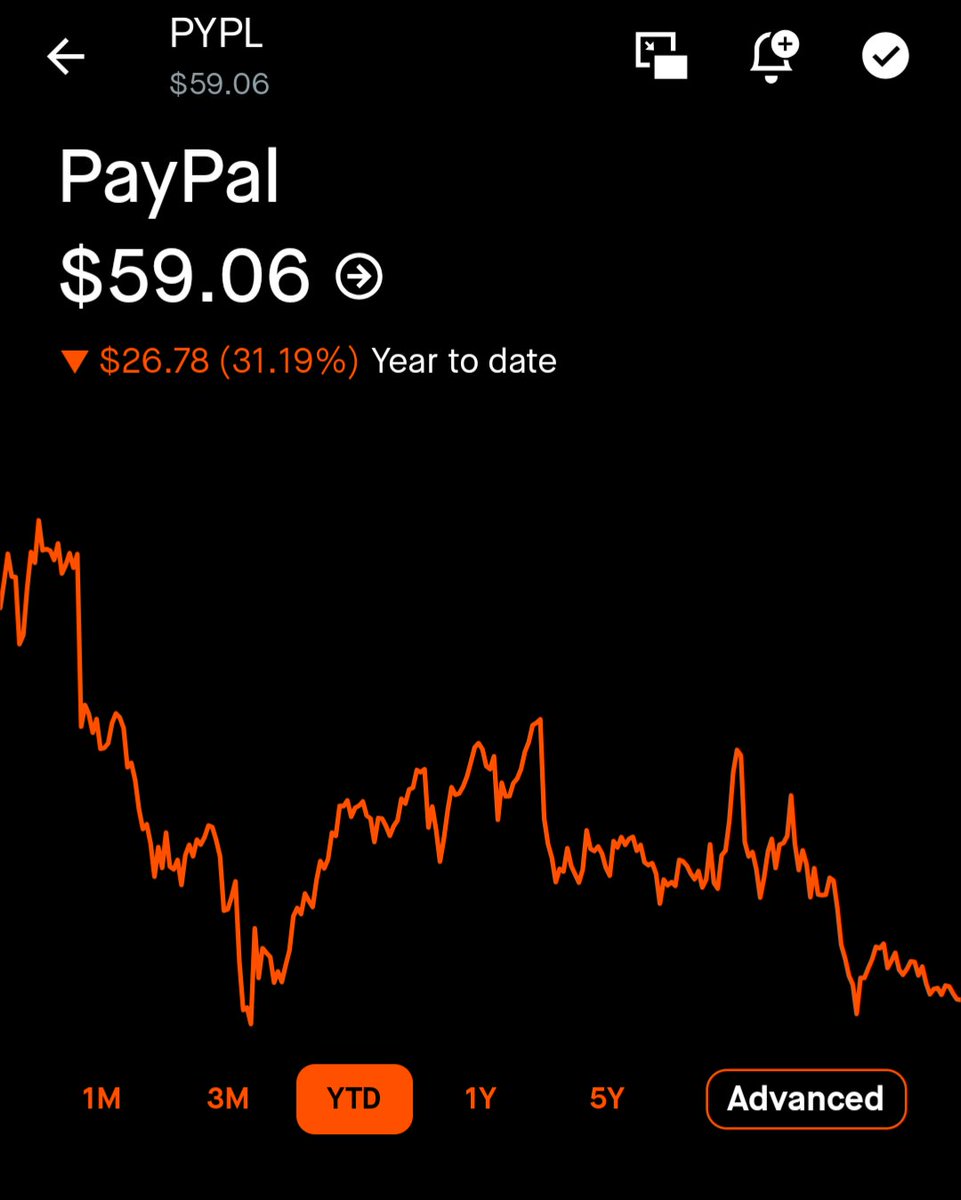

$PYPL PayPal has had yet another terrible year of stock performance. While I think there have definitely been missteps along the way, -31% doesn't feel deserved.

If it repeats this next year, it'll be trading around $40/share. It's just hard to see that kind of downside when they're continuing to grow (albeit slowly) and innovate (albeit slower rollouts for the most part).

Yet it feels like if we have a red start to the year and PayPal stumbles in their communication in Q4 earnings and guides extremely conservatively, we might see it, or at least $40's.

Would I buy more in that scenario?

Resoundingly, no, if I felt the cause was leadership and execution. If they fail to share a roadmap that the market believes, and fail to talk about new innovations and their scaling progress, that's on leadership and I'd be more keen to sell a large chunk of my remaining position despite an even more absurd valuation.

That'd probably mark the bottom.

English

@TallSeller @bobspaysubstack @grok tell me more about this No/low FEE rails and how likely is to affect $PYPL in the near medium and long term.

English

@bobspaysubstack How can $PYPL survive Juniper Research’s NO/low FEE rails growth set to 100X PayPal’s TPV globally by 2033? In USA alone #FedNow has seen 6,432,619% value transacted growth Q3 2023 to Q3 2025; & just getting started. The intersection of solutions will eat $PYPL user base & TPV.

English

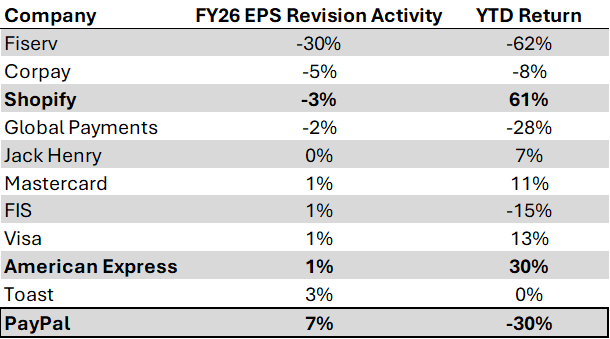

PayPal $PYPL: Another data point suggesting dislocation between price and fundamentals.

Typically, price follows revision activity across the market. Even though $PYPL has among the best upward revision activity to FY26E EPS among Payments companies, the stock's down 30% YTD. As an aside, shockingly, Shopify $SHOP is up 61% YTD despite its FY26E EPS falling from $1.90 to start the year to $1.85 now. Same goes for American Express $AXP, up 30% despite minimal change to FY26E EPS.

A $PYPL skeptic would say FY26E EPS is likely too high (as the company has recently talked down 2026) and upward EPS revision activity may be due to heavier buyback and/or buyback at lower prices. That's fair. But at a certain point, through sheer force of will, if estimates continue to move higher, price must follow for $PYPL, in my opinion.

English

@JuanRodrig07 @DividendDynasty @Kross_Roads @Couch_Investor @weary_centurion Mark Grether, our last hope!

English

@DividendDynasty @Kross_Roads @Couch_Investor @weary_centurion I hope so too. He sounds very confident about how well-positioned they are to win in this space.

English

$PYPL This is a GREAT interview from Dr. Mark Grether.

Pay attention on minute 3:40. So... PayPal Ads Manager for SMBs was launched two weeks ago? Wasn't it supposed to be in 2026? That is awesome.

A few interesting things Dr. Grether mentioned:

"For us, it's about helping them (SMBs) monetize eyeballs, we help them to make money which then they can choose to reinvest into lower prices, more advertising, or maybe they just take a few more dollars home"

"On Venmo, in October we were sold out in terms of the real estate we made available for advertisement. I was positively surprised on how interesting it is from an advertiser's perspective to advertise on Venmo"

"We have a lot of conversations with our merchants where we say: if you basically implement PayPal, give us more presentment, it means we have actually more transaction data, which we can leverage to help you grow your retail media advertising business. We can not only help retails sell more, we can also help merchants make more money by improving their retail media business"

This is BY FAR the best interview I've seen a PayPal executive give in a long, long time. This guy rocks.

Very excited to see what's next for PayPal Ads 🙌

Thanks @Iam_rouble for sharing!

English

@JuanRodrig07 I ran some simulations yesterday, and it will take around 3 years for BNPL and cards to be meaningful in the TPV mix while checkout button is flat, Paypal Ads aside. But if some of the initiatives work minimally, there is literally no downside of the price... Not selling.

English

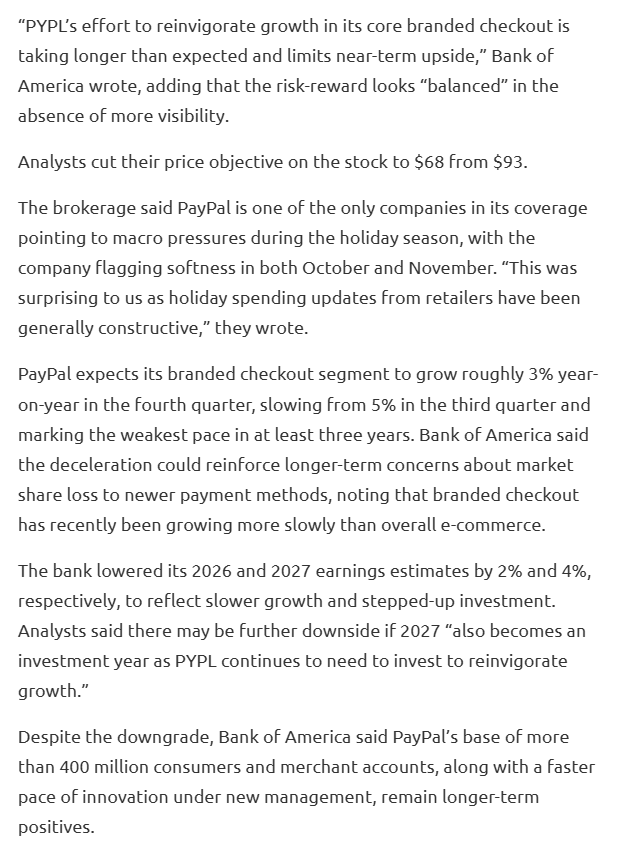

$PYPL Honestly, I can't be mad after reading the reasons for the downgrade. Let me explain:

-BofA 'surprised' when hearing macro pressures as holiday spending updates from retailers have been generally constructive.

-Branded checkout segment to grow 3% in Q4 (somewhat optimistic in my opinion, I wouldn't be surprised to see 1-2% growth)

-Slower growth in 2026/27 given more investments.

-They remain constructive long-term.

Why am I not mad? Well, during the Q3 call, the CEO mentioned they have reached a 'turning point'. But we found out within the past month that macro pressure persisted, and they would see slower growth in Q4. Also, CFO mentioned that in 2026 they would also grow a little slower.

Also, how can analysts be bullish if we have not heard anything from the new initiatives in terms of potential revenue/growth moving forward? No updates on ads, agentic commerce still too early, and Fastlane hasn't been mentioned lately (not good).

We DO know that BNPL and Venmo are killing it, but that won't be enough to accelerate revenue growth, at least for now.

Again, can't be mad when you see this downgrade. The short-term story has changed since they released Q3 earnings, so I completely understand if they want to stay neutral.

Any thoughts?

Juan@JuanRodrig07

$PYPL PayPal downgraded to Neutral from Buy at BofA BofA lowers price target to $68 from $93 😳 ‘The firm had expected product innovation and the upgraded checkout experience to drive increased usage of the PayPal button at checkout, but instead Q4 will see a step down in branded checkout growth and 2026 will be an investment year’ $PYPL down 1.8% in pre-market trading 🔴

English

DaniCN retweetledi

@jose_elias_nvr Nah, es mas fácil que eso Josete.

Tú padre trabajaba un tercio del día porque con eso mantenía a su familia y le daba para vivir dignamente.

A la generación de ahora no le da la gana hacer el mismo esfuerzo que tú padre para compartir estudio de 30 metros con dos desconocidos.

Español

@JuanRodrig07 @weary_centurion Tbh all investment community advice to not do market timing and to DCA... Here we ask the opposite... I don't know, maybe they think the stock can go even lower....

English

What's crazy to me is how indifferent they are to all this. They will spend more in 2026, so why don't accelerate buybacks now at record low valuations, buy back an extra $3B worth of stock or so, and then spend less buying back shares next year when the stock price is higher? Wouldn't that make sense?

Every single retail investor is begging them to accelerate buybacks, but instead, they issued a dividend. Seems like they do it on purpose sometimes.

They have a big chance to prove us all wrong in the next earnings call. Hope they deliver.

English

@JuanRodrig07 Fully agree... She said "we are very excited" on multiple occasions, but honestly they don't sound real anymore... I think we all were expecting a strong rebound on Q4 but they sound more like a flat, if not worst 2026... It's really becoming a cost opportunity...

English

$PYPL Jamie Miller just finished her presentation at the UBS Conference. Key takeaways and some thoughts:

- Consumer pressure persists (now mostly a PayPal-specific issue)

- Expecting lower branded checkout growth in Q4, but full-year guidance unchanged

- Higher spending planned in 2026 → slower EPS growth

- No details provided on Black Friday/Cyber Monday

The problem isn’t Jamie Miller. The problem is PayPal’s inconsistent messaging and lack of enthusiasm, which is why they keep disappointing investors presentation after presentation.

Q3 felt like a turning point: OpenAI deal, strong results, stock hit $80. Cool, we're all happy.

Then what? Back to talking about slowing consumer spending and weaker branded checkout growth. After that, back to focusing on the negatives instead of the positives.

Venmo is killing it (Diego Scotti did great during his presentation last month), the ex-Uber ads leader is delivering, BNPL is growing fast, the stablecoin is gaining traction, PayPal is well-positioned for agentic commerce, and they have plenty of capital to accelerate buybacks, and pretty much NONE of this gets highlighted?

Don’t give me the “they’re frustrated about the stock price” excuse. They have full control over the narrative and still struggle to tell an exciting story.

Question remains: they clearly have the execution, but how do they finally learn to sell the story and get investors excited again?

Curious to hear your thoughts

English

DaniCN retweetledi

$PYPL YESTERDAY the CEO published a video of how well the Cyber 5 has gone with double digit growth across several categories.

TODAY, the CFO goes and says that macro pressures persist.

Something does not add up, honestly

English