@hillery_dan Doesn't it make STRK most desirable? Less ATM, get both dividends and MSTR upside. It's like a premium version of STRF (unless Strategy is near bankruptcy which is not happening).

English

futpib

158 posts

@futpib

High-octane internet retardation

Strategy has acquired 22,305 BTC for ~$2.13 billion at ~$95,284 per bitcoin. As of 1/19/2026, we hodl 709,715 $BTC acquired for ~$53.92 billion at ~$75,979 per bitcoin. $MSTR $STRC $STRK $STRF $STRD $STRE strategy.com/press/strategy…

Elon Musk has said that AI will end America's debt crisis within 3 years, per BI

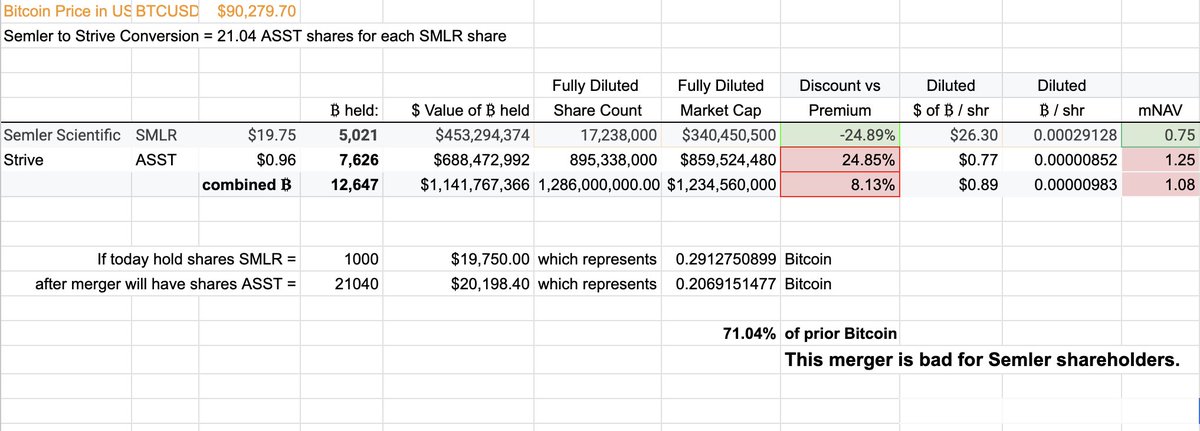

@cryptofordocs 💯 This is definitely good from a fiat standpoint, for SMLR holders. Hopefully you were buying SMLR bc it was trading <mNAV, like I was. 21.05 shares of ASST at $4.3 is $90.5, which is 3x the value today of SMLR at $29.18

@BillyM2k 2026 will be a banger

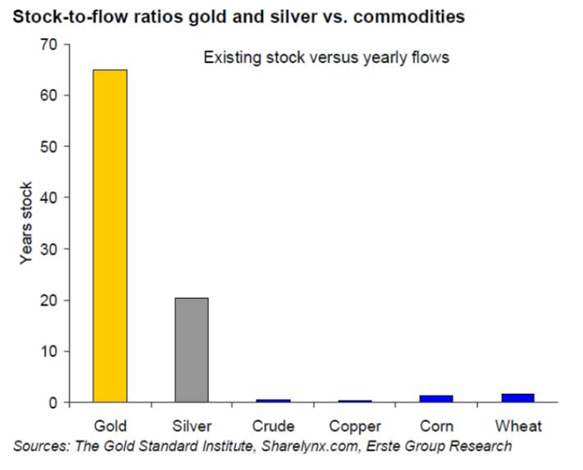

Silver’s 200 year chart is insane. What’s going on with Silver is not normal. You are witnessing history.