geetfun

10.7K posts

geetfun

@geetfun

ex @google Make app store screenshots: https://t.co/EDnhuwrce6 Build Guides: https://t.co/2ZVY3w8WvA Send Emails: https://t.co/wMe3Ll7mnJ Play Games: https://t.co/XDHcesaYsd

"Learn to weld" will go down like "learn to code." Lot of companies building AI "brains" for robots that should, among other things, know how to weld. Idea that AI won't disrupt blue collar work feels like fallacy.

Now John will say you can't hedge that way. You absolutely can. The reason Asian refiners were hedging against Dubai in the first place was convention. Their crude slate was predominantly Middle East, their product pricing was Dubai referenced, and keeping everything in the same benchmark universe simplified the book. But as more WTI Midland enters the Asian crude diet, hedging against the Brent benchmark that actually contains that grade is a tighter correlation, not a looser one. Not to mention the fact that S&P Global Platts, on March 2nd suspended nominations for any crude grade that requires transit through the Strait of Hormuz. That killed three of the five grades immediately. Dubai, Upper Zakum, and Al Shaheen all load from inside the Strait and can't get out. Only Oman (loads outside the Strait) and Murban remain deliverable.

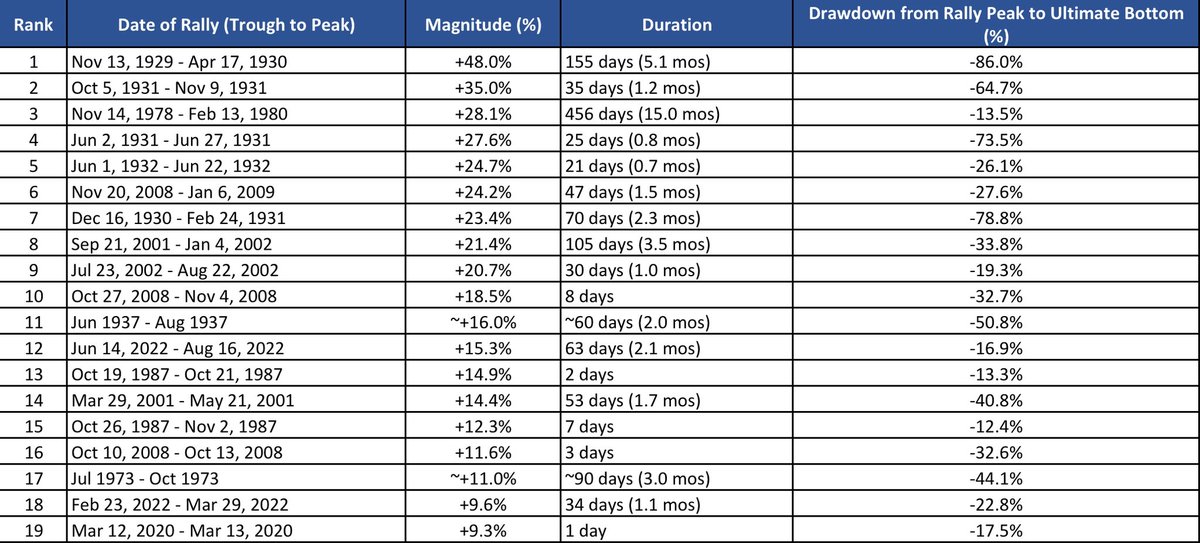

NASDAQ 100 OFFICIALLY ENTERS CORRECTION

Likely going to put in a bottom on Monday…in the short term, at least.