$SLNH Kati 2 getting closer and solid chance of lease announcement around first quarterly earnings call on August 13, 2026.

solunacomputing.com/news/monthly-u…

English

Geoff Sarna

104 posts

@gnsarna

Tech enthusiast & investor (AI, Blockchain, EVs, Space) | NFA

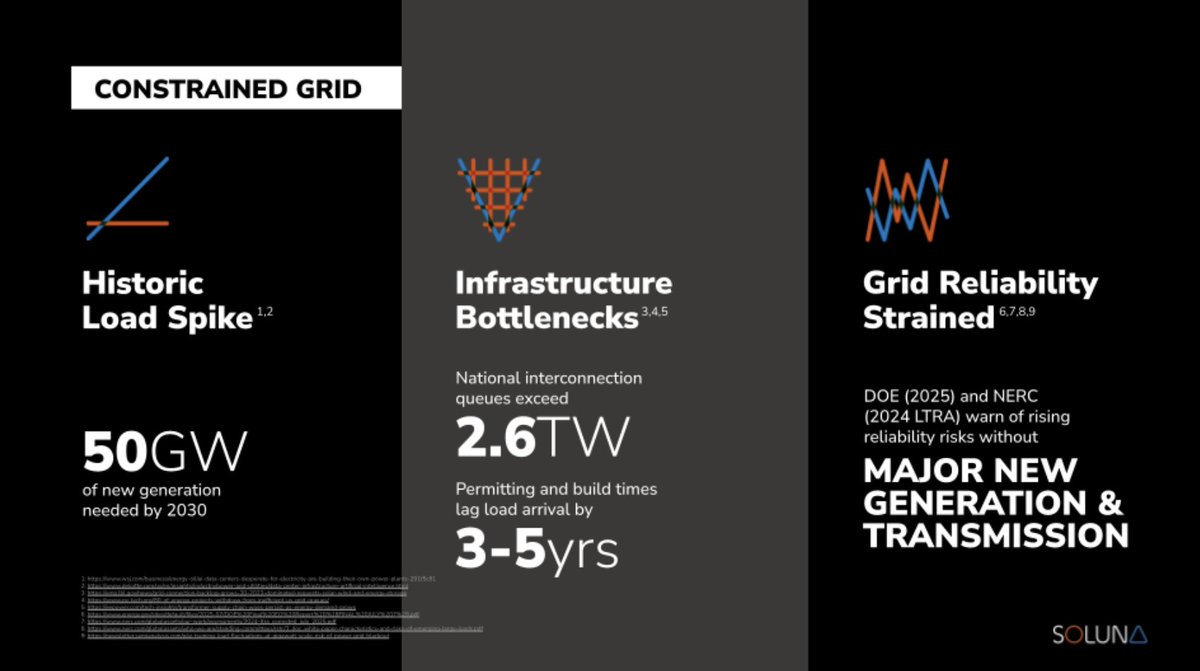

AI needs energy fast. Meanwhile, renewable power plants are forced to curtail or shut down when the grid can't handle the amount of power being produced. All that energy - wasted. Soluna has a solution. $SLNH

@perspez @whenuponly @chinoalemano @jbelizaireCEO Absolutely! Kati 2 AI announcements, Dorothy 3 AI announcements, and new AI announcements -- all before the end of 2026.

@RockwaterEQ Most of Soluna pipeline is fake, and for 2029, with a lot of dilution, not the time to buy it. DGXX at the same market cap than Soluna right now, with real stuff.

@SolunaHoldings $SLNH @SolunaHoldings has today released its May 2026 business update, and in my view this is one of the most important operational updates so far for the AI/HPC transition. The key point is simple: ▪︎ Kati 2 is moving from concept toward execution. ▪︎ Soluna confirmed that the definitive JV agreement with Metrobloks has now been signed, replacing the previously announced non-binding MOU. That is a meaningful step. A non-binding MOU is one thing. A definitive JV agreement is a much stronger structure for development, leasing, capital formation and execution. ▪︎ The update also says the design team has completed the initial design package for Kati 2, and that an RFP has been launched for the design-development and construction phase for Phase I, the first 100MW+ Critical IT. Here is the actual sequence before a project becomes buildable: ▪︎ JV structure. ▪︎ Initial design package. ▪︎ RFP for design-development and construction. ▪︎ Tenant diligence. ▪︎ Commercial negotiations. ▪︎ Capital raising. ▪︎ Then financing, construction and energization. The most important sentence in the entire update is probably this: “Tenant due diligence continues with Hyperscalers and Neoclouds. Formal commercial negotiations have started with at least one potential tenant.” That is a big step forward. Soluna is no longer just talking about general interest. At least one potential tenant has moved into formal commercial negotiations, while diligence with hyperscalers and neoclouds remains active. That is exactly the stage you want to see before a bankable AI/HPC lease can happen. The financing update is also important. Soluna said it has engaged a top-tier investment bank experienced in financing AI infrastructure projects to lead capital raising for Kati 2. That directly addresses one of the biggest questions investors have had: How will the first 100MW be financed? The answer appears to be moving toward a more serious AI-infrastructure capital stack, not just a simple microcap equity raise. If Kati 2 lands a bankable tenant, that can potentially support project-level financing, debt, strategic capital, tenant-backed structures and other infrastructure-style funding options. Dorothy 3 also continues to move forward. Soluna signed a definitive purchase agreement with a landowner for 300 acres. Environmental due diligence and survey work are underway. Fiber studies have launched. The company is coordinating with utilities to expand load and convert current BTC load toward AI. That supports the bigger roadmap: ▪︎ Kati 2 as the first major commercial AI/HPC proof point. ▪︎ Dorothy 3 as the owned-power follow-on backed by Briscoe. ▪︎ Briscoe itself is now integrated into Soluna’s operations, and the company completed scheduled gearbox maintenance on select turbines during May. That may sound boring, but it matters. Briscoe is not just a future AI narrative. It is a real 150MW power generation asset that Soluna is now operating, maintaining and integrating into the Dorothy platform. The Bitcoin hosting side also continues to support the transition. Dorothy 1A returned to full capacity after transformer repair work. Dorothy 2 remained strong with all customers at full capacity. Sophie also remained strong. Kati 1 continues to progress, with Galaxy’s 48MW operations steady, K1B Phase 1 reaching substantial completion, Phase 2 achieving mechanical completion and power commissioning, and Phase 3 ongoing ahead of schedule. That is important because BTC hosting is still the cash-flow bridge while the AI/HPC side matures. The update also shows that Soluna is building a broader platform, not only one project. Project Grace continues with PSSE/PSCAD modeling in collaboration with Siemens PTI. Annie is being developed for a potential new customer, with capital formation and modular construction design underway. Ellen, Hedy and Rosa are moving through interconnection and transmission processes.

After starting with the financing part, the next logical piece from yesterday’s $SLNH interview ( with @disruptorinvest )is Kati 2 itself. This was one of the most important parts of the conversation for me, because it showed how much the project has evolved. Kati 2 was originally discussed as an 83MW opportunity. Now Soluna is talking about a first 100MW deployment, a clear path toward a 350MW campus, and a longer-term roadmap that could eventually move toward 1GW+. That is a major change. @jbelizaireCEO described Kati 2 as probably the most active project in Soluna’s pipeline right now. Not just because of internal planning, but because several workstreams are moving at the same time: potential tenants, design firms, the Metrobloks JV, equipment providers, power design and development activity. What stood out is why the project was upsized. John said the demand signals for large-scale behind-the-meter AI capacity were already strong when Kati 2 was first scoped. Since then, those signals have become significantly stronger. The conversations Soluna is having now are not around small deployments. They are talking to hyperscalers, neoclouds and even chip OEMs about 300–400MW requirements, and they want capacity as soon as possible. That explains why 83MW was no longer enough. If serious AI infrastructure customers are asking for several hundred MW, Soluna needed Kati 2 to become a real campus opportunity, not just a single smaller site. At the same time, John made it clear that Soluna is not trying to build everything at once. The strategy is phased: start with a discrete 100MW deployment, prove the model, then scale toward 350MW and potentially beyond. That is the right way to think about Kati 2. The first 100MW is the proof point. The 350MW campus is the expansion case. The 1GW+ roadmap is the long-term optionality if power, tenant demand and financing line up. Another important detail is that Soluna has already selected architecture and engineering firms after a competitive RFP process. John described them as strong firms with direct AI experience. Design work is underway, procurement workstreams for long-lead equipment are starting, and Soluna is already working through electrical design, MEP, cooling, backup power, on-site generation and grid stability solutions. That makes Kati 2 feel much more concrete. John also described Kati 2 as Soluna’s next big flagship project. That says a lot about internal priority. Bitcoin hosting continues to matter for cash flow. Dorothy and Briscoe are important for vertical integration. But Kati 2 looks like the commercial bridge between Soluna’s current BTC business and the AI/HPC infrastructure valuation the market may eventually start to apply.