Simon French@Frencheconomics

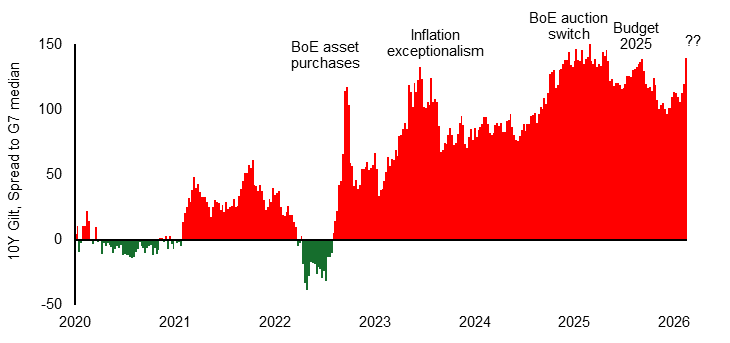

The big move in the short end of the Gilt curve (+90bp since Iran War began) has a lot of influencing factors right now, and there is a degree of selective interpretation depending on priors. But I would suggest a top five:

1. The UK is by DM standards a high inflation economy (because it rations energy, land and capital). Inflation has averaged 3%/year since 2010. An energy shock hits UK hardest, so inflation premia on short dated Gilts quickly emerges

2. UK rate cuts and an inflation slowdown were a consensus trade for Q2 so unwinding that positioning by allocators risks overshooting - particularly with a scarcity of institutional Gilt buyers (one of the legacies of the ongoing DB-DC pensions transition) and ongoing QT

3. An expensive bailout of household and business energy bills would likely result in an unexpected increase in short-dated Gilt issuance - so higher interest rates will be required to clear the market. I am surprised GBP has held up so well FWIW.

4. Rayner manoeuvres of recent days brings UK political change (with more issuance, more spending, more friction, institutional uncertainty) back on the table. Pricing that impact (comments about the OBR are classic bogeyman tactics) remains tricky, but qualitatively it certainly has been noticed.

5. BoE appears worried around inflation expectations - that remain elevated, at least in survey-based measures. A hawkish reaction that asserts low tolerance for any “look through” reprices the UK rate path. That kicked off yesterday’s move - but the qualitative MPC comments couldn’t justify, in isolation, the degree of repricing.

Some of these factors unwind v quickly on anything that looks like a ceasefire - the benefits of being a high beta sovereign. Some are longer-lasting (political/structural) and should signal to Labour MPs demanding “rewritten fiscal rules” that the starting appetite for more issuance is already thin.