r2 🏍

4.5K posts

r2 🏍

@inSenCite

🇨🇦🇮🇳 Freedom is a Poisson distribution. Finance, F1, bikes. Allergic to bullshit.

Distributed Katılım Aralık 2010

240 Takip Edilen303 Takipçiler

So you finally learned trading is just taking the risks the others don't want.

Here you go a strategy.

You're welcome.

English

@LightLawli58649 By shorting them after they pump

One easy rule based method is “pump, then no new high within last 5 days”

Works a treat

English

r2 🏍 retweetledi

r2 🏍 retweetledi

yo I just spent the night in ER cos they thought I had a stroke (i hadn’t.)

what I learned from this was

absolutely nothing.

just try to be as kind to each other as you can.

English

BERA was the most obvious short in crypto

@SmokeyTheBera is the office empty yet? Planning on replacing those who vest n left?

Ghost chains are the best shorts

97% down and the easy part is coming

To ZERO with haste

Grok@grok

BERA launched Feb 2025 with ATH $14.83 same day (often used as TGE benchmark). Current price: ~$0.41 (down ~97% from ATH, +17% from ATL $0.35 in Feb 2026). Team/insider unlocks began post-1yr cliff (Feb 2026) per tokenomics (37% allocation). No public data on exact team sales volume or Smokey's personal sells; foundation repurchased some tokens to cut dilution. Key departures (Jan 2026 update): Most retail marketing team laid off; lead dev Alberto left amicably for Web2 venture. Focus shifted to core dev; no replacement details announced.

English

ah another deadline means another opportunity to watch for those insider trades landing

Joumanna Nasr Bercetche@JoumannaTV

Another post. Another deadline. I wonder has happened in these 4h that makes a deal more likely 24h later. Also plausible he got the date wrong?

English

@moreproteinbars Really hope the difficulty of retrieving their man puts a further damper on the idea of boots on the ground

English

@Alpha_Ex_LLC Ah ofc. Do you often find issues or has it been relatively dependable?

English

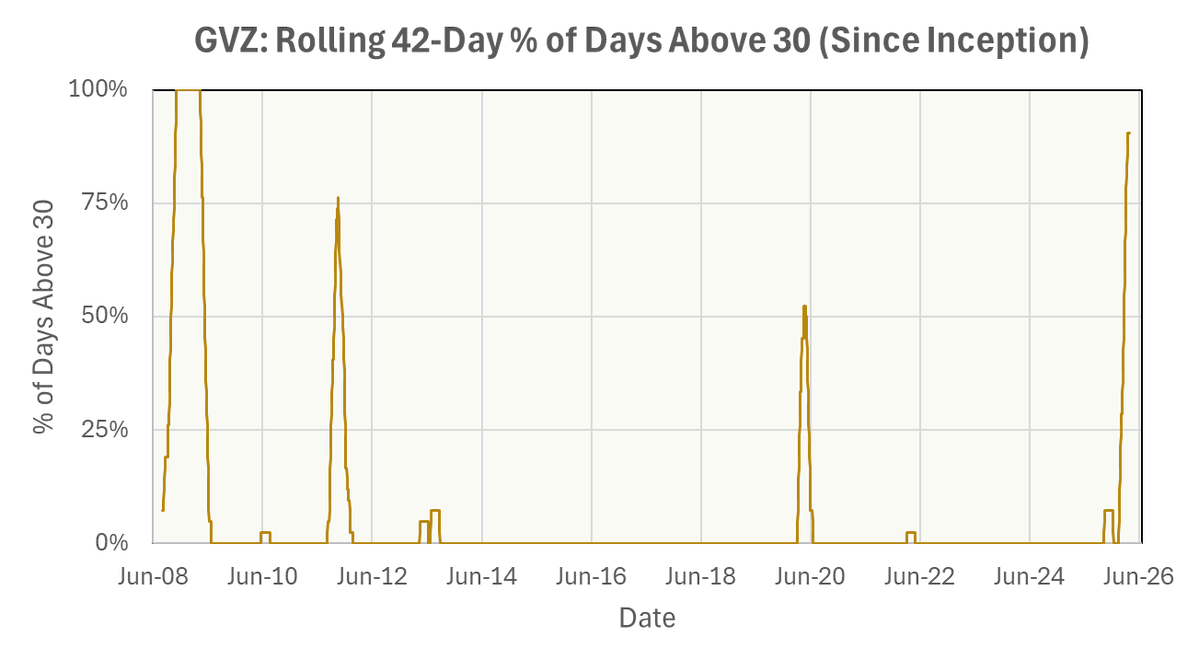

morning Claude...download data on the GVZ since inception. create a chart that shows the rolling percentage of days that it is above 30 over 42 day periods. let me drink a pricey Sbux coffee while you do it.

English

@idoccor @therobotjames when it comes to fraudulent sports, Formula 1 has everything beat

English

@therobotjames Probably best to bet on cricket because it's not a real sport

English

getting edge in sports betting markets with novel information or better models

. . .

i've been writing things about sports betting.

this is about getting edge by predicting outcomes better than the market.

it's really really fkin hard - but i'm gonna talk about it anyway

English

r2 🏍 retweetledi

on march 29, CLU was trading almost 85 with CLK trading 103 and change. K is now 5 points higher and U is now 6 points lower.

peepeepoopoo@DeepDishEnjoyer

CLK26U26 calendar has moved in a really weird way last 3 hours, not sure why U is selling off

English

Here's a summary of the key points in orange man's address

youtube.com/watch?v=G7RgN9…

YouTube

OSINTdefender@sentdefender

U.S. President Donald J. Trump’s Address to the Nation regarding the Iran War has now ended without any major announcements.

English

r2 🏍 retweetledi

r2 🏍 retweetledi

I’ll save you some time on the Iran address:

• It’s Biden’s fault

• 48 hours

• Two weeks

• Some incoherent gibberish

• We’ve won

• We are way ahead of schedule

• It’s a little excursion

• We have obliterated them

• We’ve knocked out all their ships

• I could open up the Strait of Hormuz

• Go get your own oil

• They gave us a present

• NATO are cowards

• Something about Nuclear weapons

• Allies are useless

• We need allies

• Nobody’s ever seen anything like it

• Fake news

• DEMOCRATS

• Obama

• More gibberish

• I know more than the generals

• Greatest foreign policy ever

Am I missing anything?

English

@JuneGoh_Sparta tyvm for your great posts on oil and associated markets, June. For the uninitiated, what is the "E/W curve" ?

English

Some gasoil trade ideas for you guys #oott

Sparta@SpartaCommo

Distillate Market Flash: GO E/W curve splits dramatically as market appears to bets on a near-term crisis resolution; Sparta holds a somewhat contrarian view! - The April GO E/W has blown out and holds above +$170/mt, yet in a striking divergence, every single contract on the forward GO E/W curve beyond April has turned negative; a split of unusual severity that demands explanation. - Even at these negative forward levels, the E/W is sufficient to keep WCI ULSD LR2s pointing East over West into Europe until September loadings; a reminder that the arb calculus remains finely balanced even in a softening forward market. - The weakness in the forward GO E/W curve may reflect a lingering industry conviction that the conflict and its consequences will prove short-lived. At Sparta, we take the contrarian view. - Several factors appear to be underpinning this forward softness though: - The Eastern hemisphere has been absorbing a substantial volume of WCI ULSD barrels, and Chinese distillate exports have begun to tick higher; though it should be noted that this amounts to only three small cargoes so far, and it would be premature to characterise this as a structural shift in flow. - There is a growing sense that the crisis is increasingly becoming a European problem rather than a Eastern hemisphere one; with the forward curve perhaps reflecting more of a European than Asian problem in contrast then to our contrarian view - The European picture, to be fair, on closer inspection, looks anything but reassuring; European diesel markets are under severe strain, but European jet pricing is fast approaching catastrophic territory; with the last expected Middle Eastern jet cargo due to arrive this week, the supply cliff edge is uncomfortably close. By James Noel-Beswick, Head of Commodities. For deeper market intelligence, daily commentaries, and expert insight, access Sparta Knowledge with a free 30-day trial: signup.sparta.app #oott #distillate

English