Wisarut Suwanprasert retweetledi

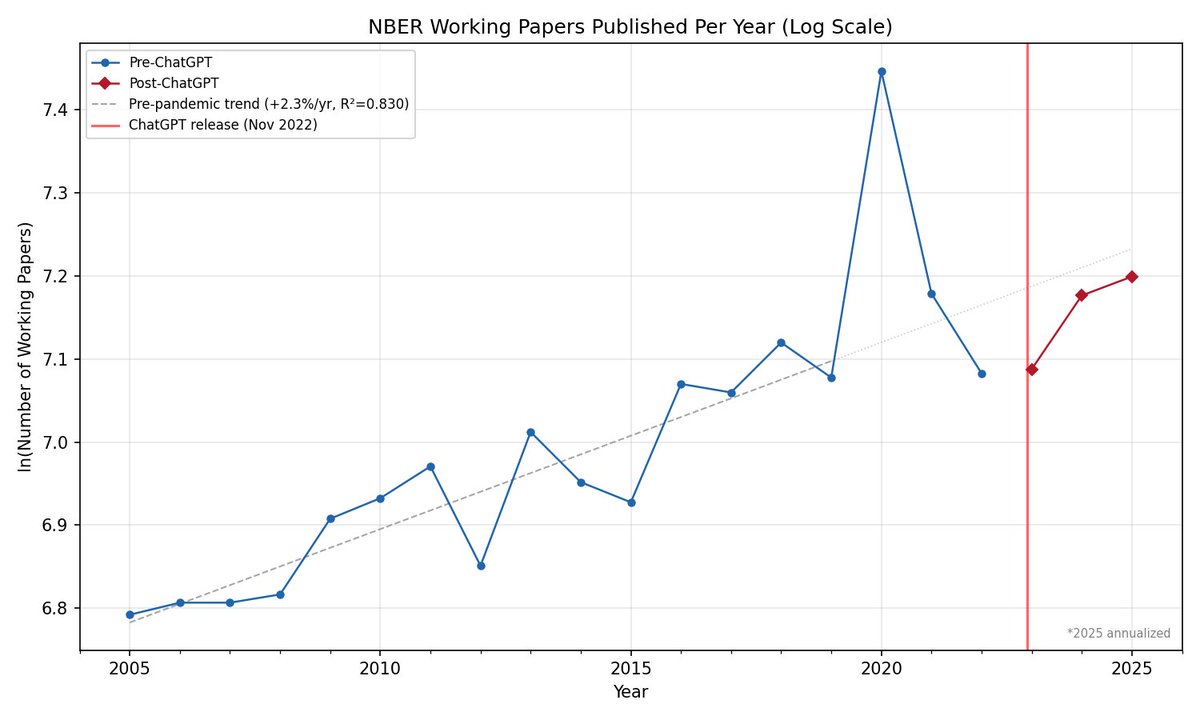

Advent of LLMs hasn't raised the number of NBER working papers above trend. (Or submissions to top journals: next tweet).

Why?

Probably because LLMs substitute for good RAs, but not for good ideas. And RA labor supply hasn't been the binding constraint in economic scholarship.

English