Sabitlenmiş Tweet

I appreciate this line from @nntaleb: "Never ask anyone for their opinion, forecast, or recommendation. Just ask them what they have—or don't have—in their portfolio." I'll post summaries of my write-ups. They aren't recommendations, just a record of my reasons for my trades.

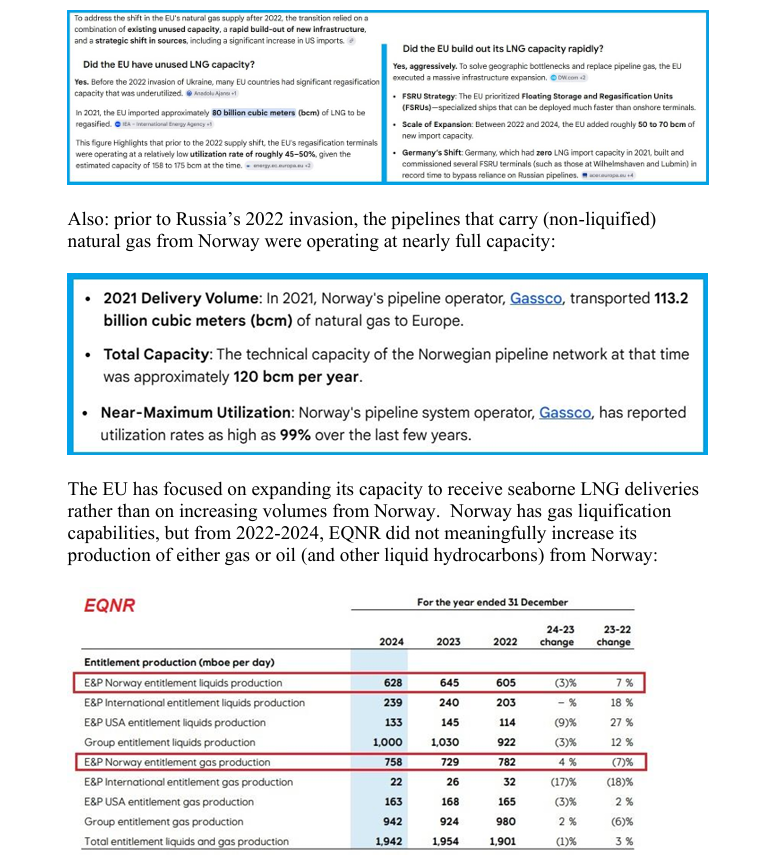

English