KK

722 posts

KK

@kkhors

Man has two lives. He will start living the second one when he realizes he only has one!

Katılım Kasım 2013

217 Takip Edilen119 Takipçiler

Since $NWBO has disclosed settlement from market makers, it's time to establish share buyback program.

These funds should not be used for R&D or G&A.

They were paid to redress direct shareholder harm.

Return shareholder capital as without it this company would be bankrupt.

English

KK retweetledi

Northwest Biotherapeutics: $NWBO

"first potential approval in the UK in 2026"

- First Berlin Equity Research

To me this looks like the greatest advance in treating brain cancer in 100 years. First Berlin think their therapy, DCVax-Direct, could treat all solid cancers.

English

KK retweetledi

$NWBO will be approved by 28th april just sit back and relax buy if you want to buy and enjoy

English

KK retweetledi

KK retweetledi

The Door is ALMOST closed:

(1) the last exit opportunity for bulls would be during the hit & rebound near 6870;

(2) after 6870, a flash crash would take place--what I warned, "200+ point" singal-day shocker.

(3) ystday's sneaky move was the last trap--but good for short entry

Master WU@MasterPandaWu

To Subs: (1) on the 30-min chart, the Black option seems in play here. (2) the pre-market plunge released the pressure, and put off the next wave's timing. (3) there is no impulsive downward move so far, so the consolidation would continue. (4) wait for 10:00am data to decice.

English

@alpharivelino But a man can make a living giving oral sex to other men… what a paradox!

English

KK retweetledi

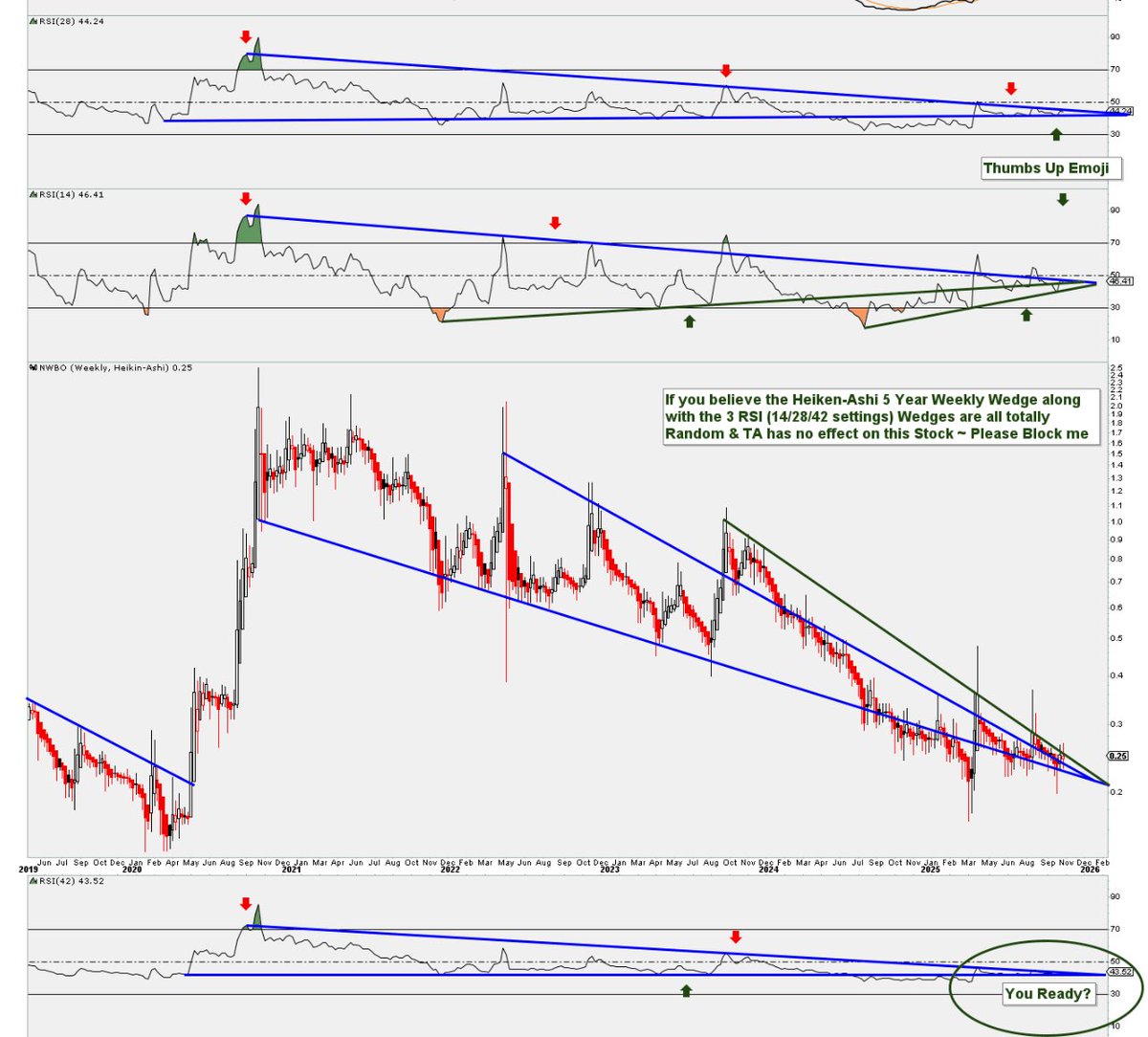

$NWBO 10 YR Daily

I highlighted handful of 4 YR indicators that exhibited extremely clean & straightforward TA Wedge breaks back in 2020: ran to $2.50

And now same indicators yet again extremely clean & straightforward 5 YR wedge breaks happening. Added detailed notes to chart

English

KK retweetledi

$nwbo Nwbo

Here is what the reality is

based on the facts

Go go go Nwbo

DCVax-L | CHM Nov 27–28 — the regulatory reality

DCVax-L is under the UK 150-day accelerated approval pathway.

The CHM meeting on Nov 27–28 occurred around Day ~143–145 — the final decision window.

At this stage, UK law is binary:

If CHM’s view is negative or blocked

• A formal CHM letter is issued

• Invokes Schedule 11

• Lists major objections

• Invites written/oral representations

• Must be sent promptly (by Day 150)

If CHM’s view is positive

• No CHM letter is issued

• File proceeds internally to MHRA licensing

There is no silent negative pathway.

Now the key overlay:

NWBO is a U.S. SEC-reporting company

Receipt of a negative regulatory letter is a material event and must be disclosed via Form 8-K within 4 business days.

As of today (Jan 12)

• No CHM letter

• No Schedule 11

• No objections

• No 8-K disclosure

Conclusion:

No letter + no SEC disclosure = no provisional negative CHM opinion.

The rejection path closed after the Nov 27–28 CHM meeting.

What remains is MHRA licensing mechanics, not scientific review.

CHM advice = positive / non-blocking.

Next step: MHRA grant.

English

KK retweetledi

🧨 Short Circuit in Penny Stock Land: How $NWBO Built a Quiet Exit Ramp From the OTC Trap

Before anyone pins this story to a single day, the boundary gets drawn once and cleanly.

What is known is boring and checkable. NWBO has an existing London Stock Exchange line under ticker 0K95 with ISIN US66737P6007, and the LSE’s instrument page shows an issue date of 24 January 2018. On 19 January 2026, the UK’s new public offers and admissions regime takes effect, and the FCA’s final rules in PS25/9 raise the “further issuance” prospectus trigger for transferable securities already admitted to trading from 20% to 75%. NWBO’s SEC filings show two specific share-count snapshots: in its 10-Q, the company states that as of November 13, 2025, it had 1,540,682,082 common shares outstanding. In its DEF 14A, it states that as of the close of business on November 14, 2025, it had 1,528,682,082 common shares outstanding and 818,142 preferred shares outstanding. Shareholders approved increasing authorized common shares from 1.7 billion to 2.6 billion, and the company filed a Certificate of Amendment on December 30, 2025 to effect that increase. NWBO’s filings also set out the Series C conversion mechanics: 10,000,000 Series C shares authorized, and each Series C share convertible into 25 common shares once conditions are met—implying up to 250 million common-equivalent shares.

What is possible follows from those facts. NWBO now has more ways to compress the time between “plan” and “execution,” and that weakens the most profitable OTC short thesis—the thesis that lives on delays and visible countdowns.

There’s a financial weather system that forms over the OTC market. It isn’t about good companies versus bad companies. It’s about what happens when a stock trades in thin liquidity, where big institutional buyers rarely show up, where financing is survival, and where the people who do show up every day can learn to steer the tape.

Northwest Biotherapeutics has lived under that weather system for years. Some investors see a slow-motion breakthrough story. Others see a slow-motion implosion. But both camps often miss the real plot. On OTC, the most profitable trade is rarely “the science is fake.” It’s something simpler and more brutal.

It’s “they won’t finance cleanly in time.”

And if that’s the bet, the counter-bet isn’t an argument. It’s a clock hack.

This piece explains how NWBO can reduce the market’s ability to trade its deadlines—through lawful disclosure timing, regulatory tempo, institutional access, market plumbing, and one sleeper asset most traders ignored: the London Stock Exchange rail called 0K95.

⸻

🏚️ The OTC Isn’t a Lower Exchange. It’s a Different Machine.

The OTC market is often described like it’s just a cheaper, lower version of a major exchange. It isn’t. It’s a different machine.

A major exchange is a crowded city. Even when sentiment turns sour, there are still pedestrians. There’s depth. Big funds can enter and exit without detonating the price because enough participants absorb slow, steady flows. The market has mass.

OTC is a rural road at night. A few cars pass. Sometimes none. When one driver taps the brakes, the whole road reacts.

That difference isn’t cosmetic. It changes everything.

OTC tends to mean thinner displayed depth, wider spreads, fewer persistent buyers, and far less automatic demand from institutions and index flows. Thin marginal demand makes price easier to steer, and steerability is what turns a financing calendar into a trade.

That is the trap.

⸻

🧠 The Real Short Bet: Time, Not Truth.

Short selling is straightforward: borrow shares, sell them, hope to buy them back later lower, return them, keep the difference. The risk is unlimited on the upside, which is why successful shorts don’t just bet on direction. They bet on structure.

In OTC biotech, the durable bet isn’t “the drug won’t work.” It’s “the company won’t survive long enough for the drug to matter.”

That survival risk collapses into three variables:

Cash runway.

Financing timing.

Regulatory uncertainty.

So the thesis becomes temporal:

They can’t finance cleanly before the next deadline.

That’s why OTC stocks can behave in a way that drives long investors insane. Good news doesn’t re-rate the stock; it gets sold into. Because the market interprets good news as a financing window. If the company still looks like it needs money, a rally is treated as supply.

Not because the news was fake. Because the clock is still on the short seller’s side.

To beat a time trade, the company has to reduce the market’s ability to trade the countdown.

⸻

🧾 The Shares: The Math That Turns Time Into a Weapon — The One-Third Partner Slot

This is what the “Rule of Thirds” idea means in plain English. It isn’t a code. It’s a deal shape.

In biopharma, there is a common middle ground between “no partner” and “buy the whole company.” A large company takes a meaningful minority stake—large enough to align incentives and justify serious capital, small enough to avoid control. That ownership band often sits in the one-third neighborhood because it’s a natural balance point: big enough to matter, not big enough to become a takeover.

That’s the one-third partner slot.

Now the numbers that make this more than vibes:

• NWBO’s 10-Q states 1,540,682,082 common shares outstanding as of Nov 13, 2025.

• NWBO’s DEF 14A states 1,528,682,082 common shares outstanding as of the Nov 14, 2025 record date.

• Authorized common shares increased from 1.7B to 2.6B, effective via a Dec 30, 2025 Certificate of Amendment.

Authorized shares are not dilution. They are capacity—legal inventory.

Capacity matters because it reduces delay. Delay is the oxygen of the time-based short thesis.

Now add the instrument lane that sits quietly in filings: Series C Convertible Preferred. NWBO disclosures describe Series C shares being convertible into 25 common shares per Series C share, and the designation of 10,000,000 Series C shares implies up to 250 million common-equivalents.

Put the geometry together:

• a 900 million increase in authorized common capacity

• a preferred conversion lane of up to 250 million common-equivalents

• a common base around 1.53–1.54 billion outstanding at the time

This is why the one-third partner slot keeps showing up in serious thinking. The cap table now enables a large minority stake to be structured through a combination of preferred conversion capacity and common issuance headroom, without requiring an outright acquisition and without forcing the company into a slow, tradeable survival raise.

That doesn’t say a partner exists. It says the company is now built to take one.

⸻

🎛️ Path Control: How Thin Liquidity Turns Into a Price Narrative

In a deep market, repetition is expensive. In a thin market, small persistent pressure can shape the path.

The tape teaches this lesson through repetition: rallies stall early, key levels fail, quiet-day downdrafts land harder than they should, and bids vanish when volatility spikes. Buyers learn not to chase. Holders learn to sell sooner. Once that behavior takes hold, it becomes cheaper to keep it in place.

That’s why the company doesn’t merely need good news. It needs an execution architecture that interrupts what the market has learned—by collapsing the reaction window.

⸻

🏛️ Institutions: The Missing Demand Layer That Changes Everything

OTC suppresses institutional participation not because institutions are sentimental, but because they are constrained. Many funds can’t buy, won’t buy, or can’t size positions rationally in thin OTC names.

A second venue is not just a second price. It’s a second compliance reality.

Institutional capital doesn’t arrive because a company is interesting. It arrives because a company is financeable: clean enough, liquid enough, and executable enough to defend in committee.

That’s why the 0K95 rail matters even before it becomes liquid. It widens the battlefield. It creates a second place where price can print under a recognized exchange environment.

And it is thin today. That’s a description, not an insult. Some market data views show periods with no trades, while others show sporadic bursts of volume—either way, it is not a deep, continuously traded line. Thinness doesn’t negate it. Thinness is exactly why a credible external print can matter disproportionately if attention and demand arrive at the same time.

⸻

🕳️ Scenario Analysis: The Swapbook Amplifier

This section describes a general mechanism; there is no public data demonstrating a specific large swapbook in NWBO.

A total return swap is a contract that gives a fund economic exposure to a stock without owning it outright. The counterparty—usually a prime broker—hedges by buying or shorting the real shares into the market.

The world learned this in Archegos. The SEC’s complaint states Archegos used swaps “to limit the visibility” of its aggregate holdings and shifted from cash equity to synthetic exposure via swaps as it approached the 5% reporting threshold. Congressional research notes Archegos reportedly never filed a 13D despite large economic exposure via total return swaps.

The takeaway is structural: economic exposure can be larger than what is visible on a short-interest report, and dealer hedging can amplify moves when the tape flips.

In thin names, that amplification doesn’t glide. It stair-steps.

⸻

🤫 The Quiet Weapon: UK MAR Delayed Disclosure

Silence is not emptiness. In regulated markets, silence can be a tool.

UK MAR—the UK Market Abuse Regulation—is the UK’s market integrity and disclosure rulebook. It governs inside information: material nonpublic information that would likely move a stock if investors knew it.

UK MAR requires prompt disclosure in general. But it also recognizes that some processes are materially important but operationally incomplete. Disclose too early and negotiations can collapse, unfinished regulatory processes can be distorted, and the public can be misled into treating intermediate states as final.

So UK MAR includes a lawful mechanism for delayed disclosure under strict conditions:

Immediate disclosure would prejudice legitimate interests.

Delay would not be likely to mislead the public.

Confidentiality can be maintained.

In a time-based short regime, the effect is surgical. Delayed disclosure forces shorts to trade probabilities instead of timing.

Inside a lawful quiet window, a company can prepare contingent financing terms, align partners under nondisclosure agreements, stage documentation, and build execution capacity so the announcement is not a scramble.

That is how the reaction window collapses: preparation happens while the countdown is invisible, and execution happens when certainty arrives.

⸻

🌉 The Sleeper Rail in London: 0K95 and the January Turn

NWBO has a London Stock Exchange trading line under ticker 0K95, and the LSE’s own page lists an issue date of 24 January 2018 and ISIN US66737P6007.

The January shift is the real turn. The rail existed. What changes in January is the operating environment: the new UK public offers and admissions regime takes effect on 19 January 2026, replacing the inherited UK Prospectus Regulation with the FCA’s new rulebook-led framework.

Activation is not a press release. Activation is a market event. It happens when real order flow runs through the London line, when brokers and market makers quote it with intent, and when London becomes the first venue to establish a reference price during a window when the US tape is offline.

Once it’s used, path control becomes containment. Containment is more expensive.

⸻

🏦 Why SETSqx Matters: Auctions Can Jump Where Continuous Trading Drifts

The London Stock Exchange’s SETSqx model is built for less liquid securities. The LSE describes it as combining a periodic electronic auction book with quote-driven market making.

Continuous trading can bleed buying pressure gradually. Auctions can bunch demand and clear it at a single equilibrium price. When demand overwhelms supply at the clearing event, the price steps.

London doesn’t need to become the primary market. It only needs to print a credible reference price during a moment when demand is concentrated and supply is thin.

⸻

📜 POATRs and PS25/9: The January Rule Change That Cuts Time Taxes

January 2026 matters because the UK’s capital-markets framework changes in a real way. The new regime takes effect 19 January 2026, and the FCA’s policy statement PS25/9 spells out a key change: increasing the threshold at which a prospectus is required for a further issuance of transferable securities from 20% to 75% of those same securities already admitted to trading.

That does not guarantee a financing. It reduces the slow prospectus bottleneck that forces financings to telegraph themselves and creates a long pre-financing window that shorts can front-run.

Shorten the window and the time trade loses oxygen.

⸻

🧬 Big Pharma: The Nonlinear Catalyst that Makes the Setup Financeable

What follows is scenario analysis, not a description of any announced transaction.

Big Pharma doesn’t finance stories. Big Pharma finances systems.

A major partner can remove solvency fragility in one move. It can validate diligence. It can improve financing terms. It can change the pricing regime from survival to optionality.

And the minority-stake deal shape described earlier is not theoretical. In 2019, Gilead and Galapagos announced a collaboration that included warrants allowing Gilead to increase ownership up to 29.9%, alongside a 10-year standstill restricting Gilead from seeking to acquire Galapagos or increasing its stake beyond that level.

That’s the template: meaningful ownership without control, paired with deep strategic access.

⸻

🧹 The 8-K: Not the Hinge, the Housekeeping

The structural story is bigger than one filing. But the filing matters in the way boring things matter in capital markets: it trims an overhang.

NWBO’s January 15, 2026 Form 8-K states that the company entered into a settlement agreement regarding Delaware Court of Chancery litigation relating to 2020 option awards, and that under the terms of the settlement the company’s insurance carriers will pay $2.25 million to the company and 17% of the challenged 2020 options will be cancelled, among other terms.

That isn’t a London prerequisite. It is friction reduction.

⸻

⚙️ Settlement Discipline: The Strong Claim Without Fairy Tales

Settlement discipline is not a guaranteed squeeze button. The strong claim is simpler: settlement culture changes the cost curve.

For instance, stricter buy-in practices or tighter stock-loan terms can raise the ongoing cost of maintaining shorts—higher borrow rates, reduced availability, recalls, and less tolerance for settlement mess in the prime broker’s own book. None of this guarantees a squeeze. It raises cost and risk at the exact moment a time-based short thesis depends on cheap persistence.

⸻

🗓️ The Holiday Window: Asymmetry that Can Matter

The holiday window is a calendar asymmetry.

For example, when U.S. markets are closed for Martin Luther King Jr. Day while London is open, the U.S. tape can’t respond intraday, but London can still print. If a real catalyst coincides with that kind of window, first-mover price discovery can land in London before the U.S. market has a chance to shape the tape.

That asymmetry can break rhythm. In thin names, rhythm is half the trade.

⸻

⚠️ What Forces Shorts to Cover: Risk Systems, Not Theater

Short squeezes don’t happen because the internet gets angry. They happen because risk systems enforce limits.

Price rises.

Shorts take mark-to-market losses.

Margin requirements rise.

Some shorts cover.

Covering pushes price higher.

More shorts hit limits.

The loop reinforces.

⸻

🔚 The Master Synthesis: Tempo vs Time

The OTC regime makes time tradeable. Shorts bet on the clock.

NWBO’s escape architecture attacks that thesis by attacking its fuel:

• POATRs/PS25/9 reduces a key prospectus time-tax for further issuances from 20% to 75% in the relevant context, shrinking pre-financing windows.

• UK MAR delayed disclosure enables lawful preparation under strict conditions, so execution can be faster once certainty arrives.

• 0K95 provides a real London rail, even if thin today, operating under SETSqx auction mechanics that can print stepwise references.

• Share capacity + Series C terms make a serious strategic partner deal shape mechanically feasible.

• Big Pharma precedent shows the large minority-stake template is real, not exotic.

• Swaps explain how visible short interest can understate exposure and why reversals can amplify under dealer hedging.

• 8-K housekeeping trims friction and removes a governance overhang.

⚖️ Disclaimer: This is for informational and educational purposes only and is not investment advice.

English

KK retweetledi

I stood in the lobby with my new friend @rdurairaj during this same conversation, and we both expressed our thoughts that Q1 2026 would be #NWBO ‘s time. LP gave a slight smirk that if you weren’t paying attention, you would have missed it and then responded, “As they say, from your lips to God’s ears.” Her position was one of poise and confidence the entire time. “We can launch whenever once we get the approval, we don’t have to wait for anyone or anything.” In my opinion, the MHRA would not expend such exorbitant time and resources on a product that they intend to deny. I think we are crossing the last t’s and dotting the last i’s.

English

KK retweetledi

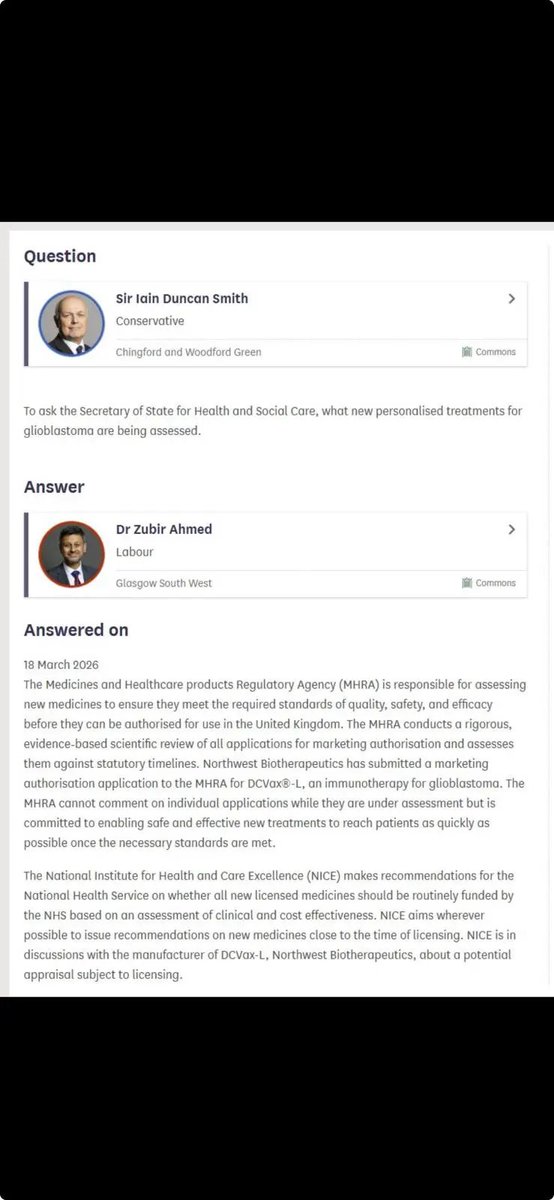

Important regulatory update (UK):

MHRA has issued UK MIA 54923 (dated 15 Dec 2025) to Advent BioServices covering commercial GMP manufacture of human cell therapy products, incl. QP batch release.

1. This licence scope explicitly covers biological / cell therapy medicinal …

English

KK retweetledi

TRUMP DECLARES VICTORY OVER HURRICANE SEASON!

Zero hurricanes in the GULF OF AMERICA!

English

KK retweetledi

Men,

This is why you must choose the healed one 🤯

English

There is ZERO difference between having a 50-year mortgage and renting.

Prove me wrong.

English

Social Awareness Poll: What is the best way to make housing more affordable for the younger generations?

English

$NWBO Friday Night Party

Weekly Heikin-Ashi & Multiple RSI Wedges

Watching Roadhouse @BoxerJ1974 @kkhors

GIF

English