Zhiyi Li

25 posts

Zhiyi Li retweetledi

I personally think valuations are extremely stupid now on $AAOI and $SIVE.

With AAOI you're doing $5.62B annualized revenue (probably higher), by midpoint next year. And it's a $8B MC.

With Sivers, I would est. it's close to ~5 forward 2028 P/E off 10% win allocation, 65% yield, and $75 ASP.

English

Zhiyi Li retweetledi

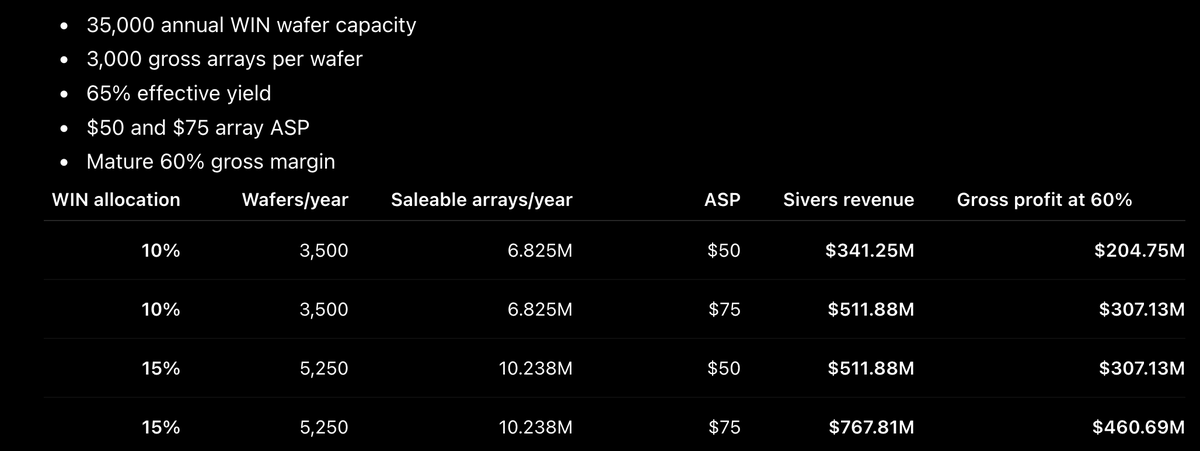

Lot of people were curious about $SIVE capacity volume ramp modeling through fab-light (Win Semi + others):

Using 10% of Win's wafer capacity as a low-end allocation (65% yield assumption, $50-$75 ASP):

Sivers would support $341-$512M worth of annual array revenue. Given upper end of managements 50-60%+ gross margin target, would be roughly:

$205–307M of annual gross profit.

Against Sivers current ~$1.1B MC, would be ~:

3.6–5.4× MC/gross profit if this capacity scenario plays out in 2028.

And at 15% would be $307–461M in gross profit (2.4–3.6× MC/gross profit)

Sivers CEO also replied that they're working with more fabs for capacity. And from an older deck, there looks to be more qualifications since 2024.

So capacity targets might be larger than what's stated here as CPO takes off.

I also expect to see revenue pipeline projections hiked in future quarters, as more qualification suppliers to into HVM.

_

As for demand side, CW also happens to be very bottlenecked.

Lumentum are buying CW off the open market due to EML obligations from their ER transcript.

And $AMD are signing LTAs to secure CW capacity (from Trendforce). So when Sivers is ramping with $GFS, $JBL, Ayar, $POET, O-NET and others...

Given the current constraints, it's highly likely any independent qualified capacity that comes online would be absorbed.

And as a cherry on top, Morgan Stanley named $SIVE (~$1.1B) as one of the three leading CPO laser players .

Alongside $55B+ players Coherent and Lumentum in their recent note for a reason...

_

TLDR: Sivers only needs a low end allocation from Win to make substantial gross income relative to current valuations.

I think the largest revenue upside that isn't modeled in if they TAM expansion with M&A after US NASDAQ listing.

By copying the Lumentum playbook with Cloud Light to build out entire transceiver modules or with optical engines.

Anders Storm@StormDirac

Your assumptions are wrong. Win Semiconductors has a InP capacity of 35.000 wafers per year. Assume even a low number 10% of that is 3500 wafers. There are approximately 3000 CW arrays on a wafer, price per Array >$50. At only 10% of this capacity Sivers could sell for more than $500m just for arrays..then you have pluggables, wireless...at 20% capacity...even more. Production qual has been ongoing for sometime, as WIN mgmt confirmed, hence should not be too far away.

English

I agree

Today is a crucial day for $SIVE

If we don’t see any insider selling (which is highly likely), I think we will see a strong rebound

Combined with the purchases by 6 insiders this week, including the CEO, it would represent a massive vote of confidence in $SIVE

On the other hand, I agree that even with a rebound, we will probably fluctuate in the 30-50 SEK range (as our colleague mentioned) until we start seeing recurring revenue

We'll see how the day goes and how the insiders move

Still, in the short term, this won't affect anything other than some people's confidence

In the long term, the fundamentals remain intact

Long on $SIVE

Fynn🇬🇧🏗️@fynnvestor

$SIVE down again today 🔴 It’s been a brutal few weeks for $SIVE and semis generally. The next big factor will be the Q2 Earnings Report in August. Until then we’ll probably just bounce around this €3-5 level

English

Zhiyi Li retweetledi

Morgan Stanley note on CPO today. Key participants include:

- $SIVE, $COHR, and $LITE in laser supply

- Broadcom and Nvidia in switch platforms

- Lightmatter, Ayar Labs, Marvell/Celestial, and POET in optical engines and photonics,

- $TSM, $GFS, and $TSEM in silicon photonics foundry capacity

I’ve covered all of these before, like Tower Semi.

But I’m especially happy that Morgan Stanley validated my research that $SIVE is one of the critical global players in CPO.

A small $1.5B laser company next to your two leading $60B+ companies…

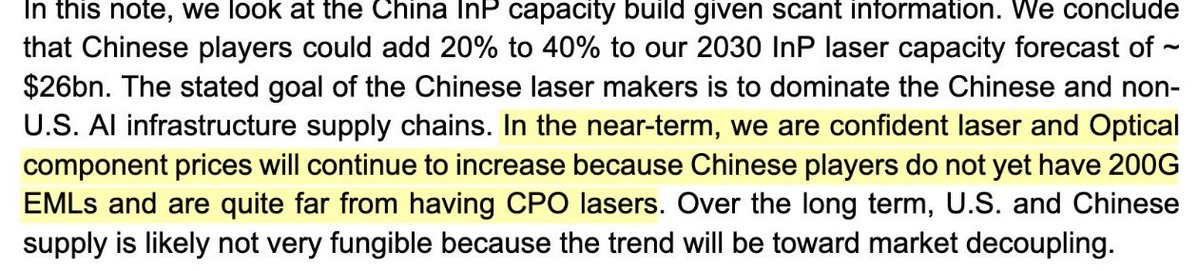

If you also synthesize Rosenblatt Securities recent note that China laser suppliers were quite far from having CPO lasers.

This kinda magnifies importance of the three Western leaders of that laser chokepoint.

English

Zhiyi Li retweetledi

TLDR of Innolight investor relations takeaways:

1. "Overall, 1.6T market demand has not contracted; instead, 800G demand has increased significantly compared with previous expectations"

Prob most important takeaway as a whole was 800G demand revision (also longer tail demand). Which is a bullish read through on US transceiver makers like $AAOI, $COHR, $LITE.

Lot of new customers like neoclouds, AI model companies, contributing to overall demand rather than just hyperscalers, diversification always a bonus.

2. Innolight said the shortage covers the module supply chain broadly including:

- Optical chips.

- Electrical chips.

- PCBs.

- Other module materials

From last ER, I think they singled out EMLs and CW optical chips as the most constrained. So Innolight's bottleneck list mention broadened since then.

They expect some of the component availability to improve gradually from the second half of 2026 through the first half of 2027.

Think a lot of this is already known from earlier though.

But just some confirmation + easing timelines (EML is extremely bottlenecked, same with CW, this is probably talking about other components).

3. Innolight said module-production equipment is not the constraint. Equipment lead times remain relatively short.

So this isn't really a bottleneck compared to others.

4. The overall proportion of silicon photonics continues to trend upward. Last year it was mainly 800G. This year, some 800G customers are further increasing their silicon-photonics proportion. 1.6T also added some new customers

Positive for SiPH penetration eg. $SIVE / $JBL, since this shifts away from EML toward CW.

Basically: main surprising takeaway is just 800g demand go brrr.

Apart from that just reaffirming bottlenecks/timelines/market speculation.

English

I think the bottom is here or very very close for $SIVE at around 40 SEK~ $4 USD. But I honestly do not know how long we will be around these prices. Nobody can time the market and we could sit here for a while.

The sell off across photonics, AI and CPO has been extreme. The macro is rough. The bears are loud. And yes it is easy to be bearish right now. It is always easy to be bearish during a drawdown, especially a major one...

But we happen to be in the middle of the biggest technological revolution of our lifetime.

And with that. we have a company with confirmed partnerships connecting to some of the most powerful companies on earth. $GFS. Ayar Labs. $JBL. $POET. O-Net and $ENA. A Fortune 100 wearable customer approaching volume phase. SATCOM and defense revenue already coming in. CPO just around the corner.

And the valuation sitting at roughly $1.2 billion.

That is a joke for what this company has built.

You do not attract this many multibillion dollar partners linked to hyperscalers by being average. These companies do not sign deals with companies they do not believe in. They chose $SIVE.

Institutions just bought at 57 SEK in an oversubscribed raise that closed overnight. That does not guarantee a floor. But there was enough conviction from serious money to fill that book in hours at a price 40 percent above where we are trading today.

$SIVE does have to execute. And I believe they will.

English

今天川普接受采访时两次谈到习近平

视频一:谁是他心中最最伟大的世界级领导人,川普首推习近平

视频二:习近平的哪一点最让他钦佩,他说习近平本可以让12艘驱逐舰为油轮护航,冲破封锁线,取得历史性成就。但习近平在他的请求下未介入伊朗战争。

——不禁让人怀疑:如果习近平攻打台湾,川普怎么办?

中文

When I visited Computex, Ayar Labs treated SIVE not as something they rely on exclusively, but more as one option among several.

I still haven’t seen any third-party or authoritative data showing that SIVE is superior to its competitors.

Jukan@jukan05

@aleabitoreddit I don't like $SIVE

English

$SiVE , good news ladies and gents, Institutional ownership has shown up for JP Morganchase as they crossed the 5% mandatory reporting threshold.

Official form:

mfn.se/cis/a/fi-se/fi…

English