Mac retweetledi

Mac

58 posts

Mac

@mackhajuria

Personal opinions on tech and ads | https://t.co/rDSlaHh11I

New York, USA Katılım Temmuz 2019

121 Takip Edilen1.1K Takipçiler

Mac retweetledi

Margins are tight today, agreed.

But two things shift the math.

First, the cost stack is on a steep depreciation curve. Lidar, compute, sensors are all collapsing in price year over year. Margin headroom opens as the stack cheapens. This happens with all technology that gets commoditized.

Second, intermediaries don't survive on margin alone, they survive on what they uniquely deliver. For AV operators, that's direct access to demand at scale, which is exactly what Amazon provides its sellers. The stack consolidates around whoever owns that access.

Fascinating indeed.

English

At some point for an intermediary to take margin- they must add value.

In this case there are too many intermediaries and not enough revenue or margin to share. It’s not a race to the bottom it starts so near the bottom there is no early adopter breathing space .

It’s already a busted flush imo.

Vertical integration across technology and services …..or go home. Fascinating New Market to study.

English

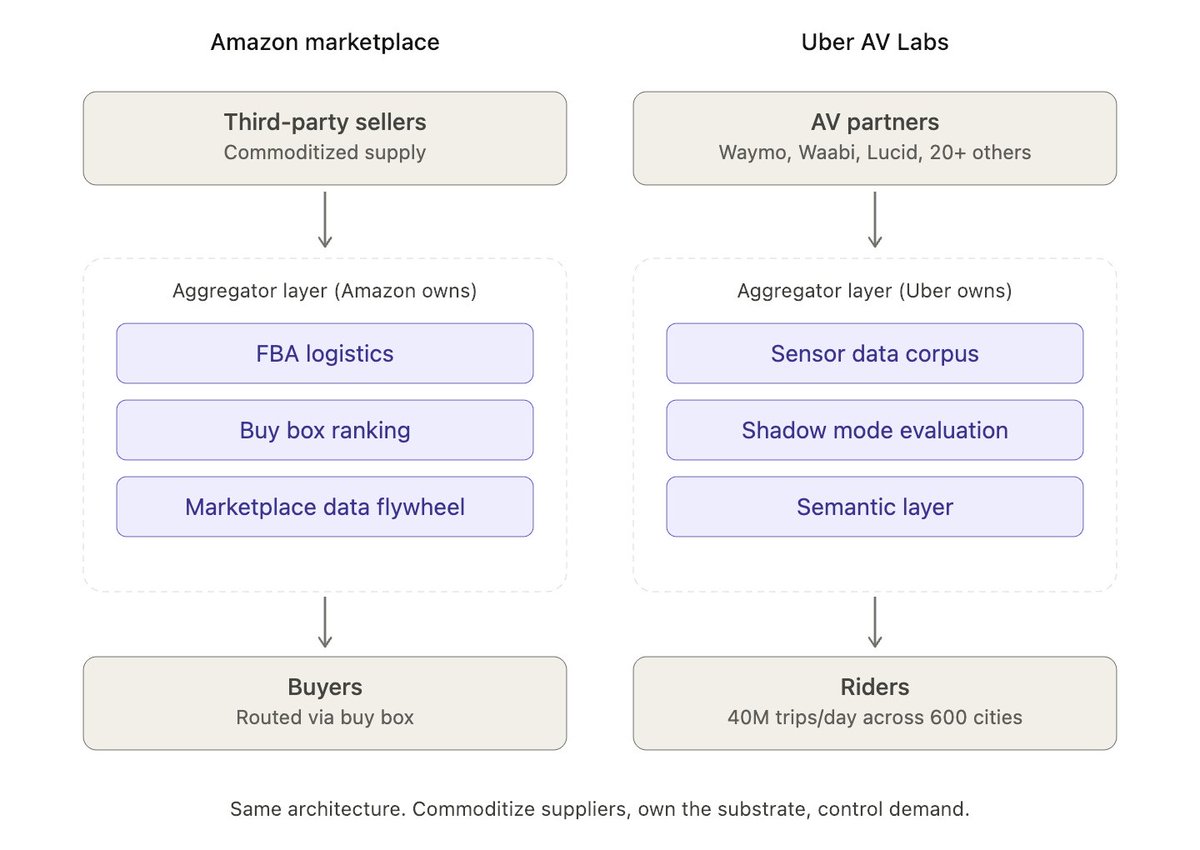

From a strategical lens, it can be stated that $UBER AV Labs is aggregation theory applied to autonomous mobility, and in my humble opinion it's the most underappreciated platform move.

Read past the "data collection" framing. This is Uber positioning itself as the indispensable data and demand aggregator for the entire AV stack. The $AMZN parallel keeps popping up in my head.

The supply-side problem: 20+ AV partners (Waymo, Waabi, Lucid) all need the same input. Real-world driving data at scale. The empirical benchmark is ~10M miles before an operator reaches its first public driverless launch. Tesla solved this with millions of customer cars. Waymo solved it with a decade of head start. Everyone else who is entering the market has a physical-limit problem and to say two manufacturers will run the world's AV ecosystem is very naive.

Now the Amazon analogy. Amazon didn't win retail by making the best products. It won by becoming the marketplace third-party sellers couldn't afford to skip, then quietly owning the layer underneath them. FBA for logistics. Buy Box for demand routing. Marketplace data feeding Amazon Basics. The sellers compete on Amazon's surface while Amazon owns the substrate.

Uber's natural advantage: 40M trips/day across 600 cities. Hundreds of sensor-kitted Ioniq 5s scaling onto the network. Critically, running paid rideshare missions, not test loops, so the data reflects the actual edge cases riders encounter every day. Trajectory: at least 2M miles/month by year-end, scaling through 2027.

Now the Amazon analogy. Amazon didn't win retail by making the best products. It won by becoming the infrastructure that made it economically viable for any seller, large or small, to reach a national customer base. FBA solved logistics. Prime solved trust. The marketplace aggregated demand sellers could not have reached on their own. The pie got bigger for everyone who plugged in.

Uber AV Labs is the same architecture pattern applied to autonomy. Collection inside real revenue trips with no constrained ODD. A semantic contextualization layer, not raw dumps. Long-tail mining of edge cases that AV stacks cannot manufacture in sim. A shared evaluation framework where partner ADS runs in shadow mode and divergences get flagged back. Think FBA for autonomy: shared rails so every partner can commercialize faster than they would solo.

The tell is the pricing decision. Uber is giving this away. Per CTO Praveen Naga, advancing partners' AV tech is worth more than any line item Uber could charge.

Classic platform logic. Grow the ecosystem, grow the pie.

In my humble opinion, this is the real thesis. The data isn't the product. It's something closer to a public good for the AV ecosystem that only Uber can produce at this scale. Every partner that taps in gets safer miles behind them, richer real-world distributions, and a faster path to commercialization than they could ever achieve alone.

Uber isn't selling shovels to the AV gold rush. Uber is building the foundation everyone gets to build on.

Not everyone is a $TSLA or a $GOOG

Balaji Krishnamurthy@_balaji_km

We have been busy bringing our AV Labs fleet to life. Over the coming months, many hundreds of cars fitted with a suite of sensors (cameras, lidars and radars) will be operating on Uber’s network. Importantly, these cars will be generating revenues and completing regular Uber trips - going to airports, driving through construction scenes, navigating congested downtown corridors - getting exposure to the variety of “edge” cases our network handles countless times each day, as we fulfill 40M trips daily. A common question we have asked ourselves and our partners - how much data is enough data? One way to think about this is that AV operators globally have needed at least 10M miles of data to reach their first public driverless launch. By the end of this year, this fleet will be generating at least 2M miles each month, and will scale further from there in 2027. For our partners, we will democratize access to data for autonomous development, and we will do so with the best in class data that only Uber can generate.

English

I appreciate the reply and the thought behind it.

But I think the Tesla CT example actually strengthens the thesis.

If raw data does not move cleanly across stacks, compute, and form factors (agreed, it doesn't), then whoever owns the canonical semantic layer above the raw stream becomes more valuable, not less.

$UBER explicitly says partners don't receive raw data. They receive semantic understanding plus shadow mode divergences. Platform-agnostic at the behavioral level.

On existential threat to the human-rider/human-driver model: completely agree and so does the CEO. The model will shift and be hybrid at first and the gradually more and more AVs will take over in the future. That's the strongest possible motivation for the aggregation play, not a counter to it.

On the margin stack of sensors, software, compute, charging, storage, maintenance all chasing a slice of $2/mile: also fair.

But thin margins are exactly the regime where aggregators win. Whoever routes the most demand to the most fleets survives the squeeze.

And "they don't make cars" isn't a bug of the thesis. It is the thesis. Amazon doesn't make most of what it sells either (and didn't especially when they first started).

English

You would be absolutely correct if the "Collected Data" was a universally defined format such that it was a clearly defined replicable commodity across and from multiple vehicle platforms - irrespective of sensor Set Up, vehicle size, on board compute , OTA capability and vehicle shape.

Despite the 8-9 Billion miles of Tesla data that Tesla collected from its 8m vehicle fleet ( In shadow mode) then labelled and categorised, and trained on, so they could deliver supervised "Autonomy" for the Model Y it didn't work for the Cybertruck. ( CT) And it doesn't work for the Cybercab. (CC)

It took them 9 Months of further data collection from CT , complimented by adjusted training, application trial and error to achieve an acceptable level of Autonomous safety for the CyberTruck.

Sadly - "Not all data is equal" and it's certainly not equal amongst Ubers 20+ very different, independent, aspirational AV participants.

I believe it is an order of magnitude more complex than you imagine.

Uber have NO choice but to continue to insinuate their inclusion & participation in the new technology of Driverless Robotaxi, that replaces their model of aggregating Human Riders with Human Drivers.

It really is an existential threat to their model .

Accelerated diversification away from Rides is a good strategy and Dara is a great CEO..

They do not make cars and many of their AV Partners don't make cars either . The Manufacturing partnerships required to deliver a functional AV requires multiple partnerships of Sensors, Software and Compute.

The Operational Partnerships for Charging, Storage, Cleaning and Maintenance are essential because Ube has none of that. these too seek margin.

Each partner is participating in pursuit of a share of the $2 per mile. Expect Rivers of red INK . It's a Problem.

English

Wayve was $UBER's preferred partner in the UK for L4 trials.

Now it's expanding to the US and working with Stellantis in Detroit.

Stellantis owns the following brands around the world:

Abarth

Alfa Romeo

Chrysler

Citroën

Dodge

DS Automobiles

Fiat

Jeep

Lancia

Maserati

Opel

Peugeot

RAM

Vauxhall

Alex Kendall@alexgkendall

I'm in Detroit today for some big news! Excited to work with @Stellantis to integrate our @wayve_ai Driver into their vehicles, starting in North America in 2028. Stellantis’ scale + Wayve’s global AI = magic for customers.

English

Mac retweetledi

In mid 2025 there were only 36M Uber One members.

Just the start!

$UBER

Andrew Macdonald@andrewgordonmac

50M+ Uber One members. 37 countries. 10 days of deals. ✈️ Bonus miles with Delta (@Delta) 🏨 Marriott Bonvoy points up for grabs (@MarriottBonvoy) 🎬 Fandango perks (@Fandango) 🛍️ Sephora, Best Buy, Kroger savings (@Sephora @BestBuy @kroger) 🍕 50% off Domino’s pizzas (@dominos) 🥪 BOGO Subway (@SUBWAY) ☕ Starbucks breakfast (@Starbucks)

English

Mac retweetledi

Bike ✅

Helmet ✅

Daam Pachchis Hai! (“Rides at just 25 Rupees”!)

English

In terms of affordability and pricing $TSLA ran this same playbook: start premium, scale down. Roadster → Model S → Model 3

$RIVN is now at R1 → R2 at $58K → $45K trim by late ’27

Wall St Engine@wallstengine

Rivian $RIVN says more R2 variants are coming. CEO RJ Scaringe didn’t give details, but said the Georgia plant is built for different versions. The R2 starts at $58K, deliveries begin around June, and a $45K trim with 275+ miles is due by late 2027.

English

$UBER Eats has launched in Finland

Andrew Macdonald@andrewgordonmac

Update - we are #1 in the Finnish app store! 🚀🥇🇫🇮

English

Mac retweetledi

.@Uber Q1’26 earnings are out — we’re off to an exceptional start to 2026:

✅Third straight quarter of 21%+ Gross Bookings growth

✅Non-GAAP EPS up 44% to $0.72

✅Nearly $10B of TTM Free Cash Flow — a record high

🥇Membership joined the 50/50 club — 50M members, 50% Gross Bookings coverage

🏋🏻♂️No skipped reps — delivering on our Mobility barbell strategy (low cost + premium)

💰Record $3B in share repurchases

Looking ahead, our product innovation, AV leadership, and AI momentum have us well positioned to accelerate the power of our platform. Let’s #GoGetIt!

investor.uber.com/news-events/ev…

English

$UBER Q1 2026 Earnings:

- Trips during the quarter grew 20% year-over-year (“YoY”) to 3.6 billion, driven by Monthly Active Platform Consumers (“MAPCs") growth of 17% YoY and monthly Trips per MAPC growth of 3% YoY.

- Gross Bookings grew 25% YoY to $53.7 billion, and 21% on a constant currency basis.

- Revenue grew 14% YoY to $13.2 billion, or 10% on a constant currency basis. Business model changes negatively impacted total revenue YoY growth by 9 percentage points, or 8 percentage points on a constant currency basis.

- GAAP Income from operations grew 57% YoY to $1.9 billion.

- GAAP Net income attributable to Uber Technologies, Inc. was $263 million, which includes a $1.5 billion net headwind (pre-tax) from revaluations of Uber’s equity investments. GAAP Diluted earnings per share (“EPS”) was $0.13.

- Adjusted EBITDA grew 33% YoY to $2.5 billion. Adjusted EBITDA margin as a percentage of Gross Bookings was 4.6%,up from 4.4% in Q1 2025.

English

Mac retweetledi

Your next getaway is just a tap away. Hotels are officially on Uber 🛎️

Book from 700,000+ stays around the world directly in the app. Uber One members get 10% back in credits on every stay, as well as 20% off at 10,000 featured properties.

Stop scrolling and start booking. Your room awaits.

English