@aleabitoreddit @itsDanielWu Not true, those "cant buy this/gimme US ticker nao pls" are missing from the picture..

English

Marollakki

205 posts

$WOLF was probably the most interesting one up there after restructuring. $LPKFF also for glass substrates and they own the laser induced deep etching at a $169m MC, so possibly most explosive 10x upside. $MTRN is probably the most stable one up there with decently high upside given it owns the mountain for ~65% of the world's Beryllium. There were a few others but just the fundamentals were either really bad or their bottleneck was too niche. $LPTH's bottleneck for example spreads across both defense, AI, drones, etc. $AXTI's bottleneck was so big and AI is such a big sector so it doesn't need to be spread across (but InP is used in a lot of other sectors too).

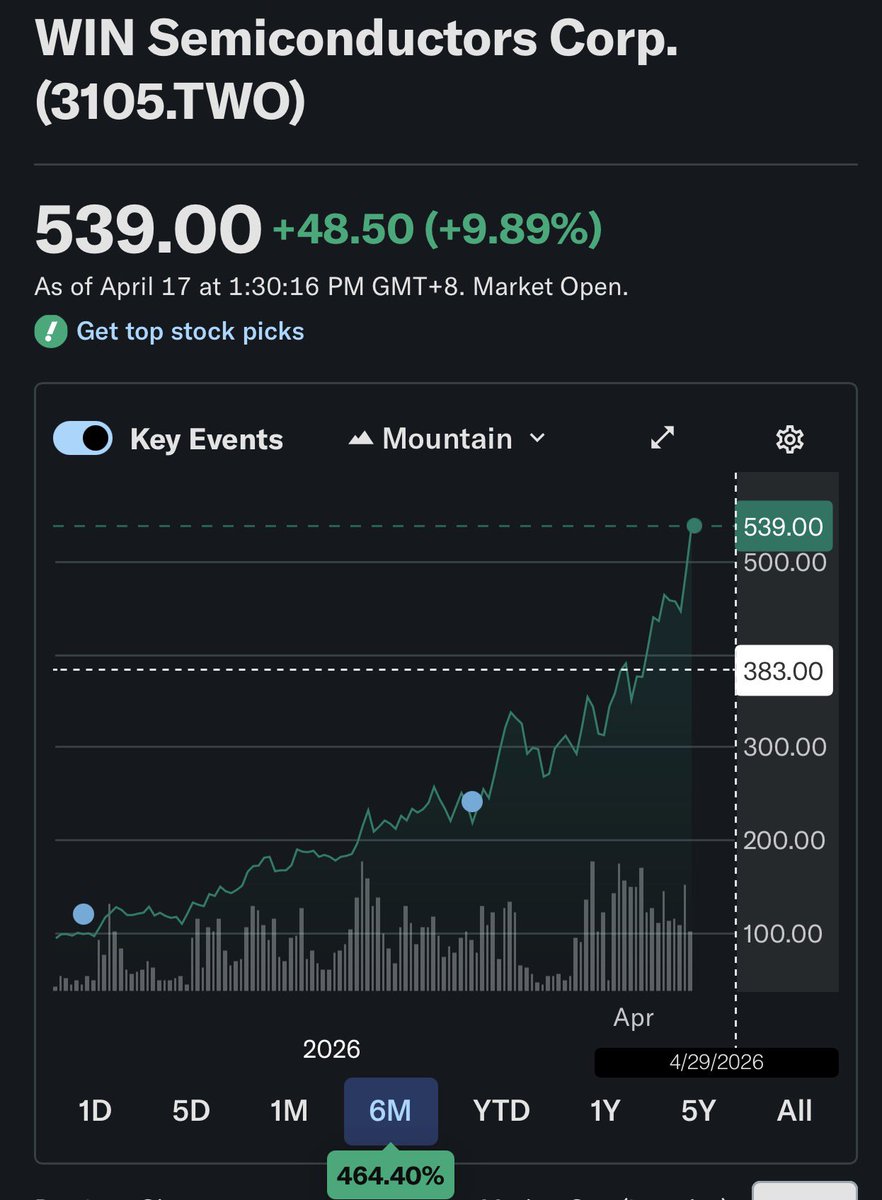

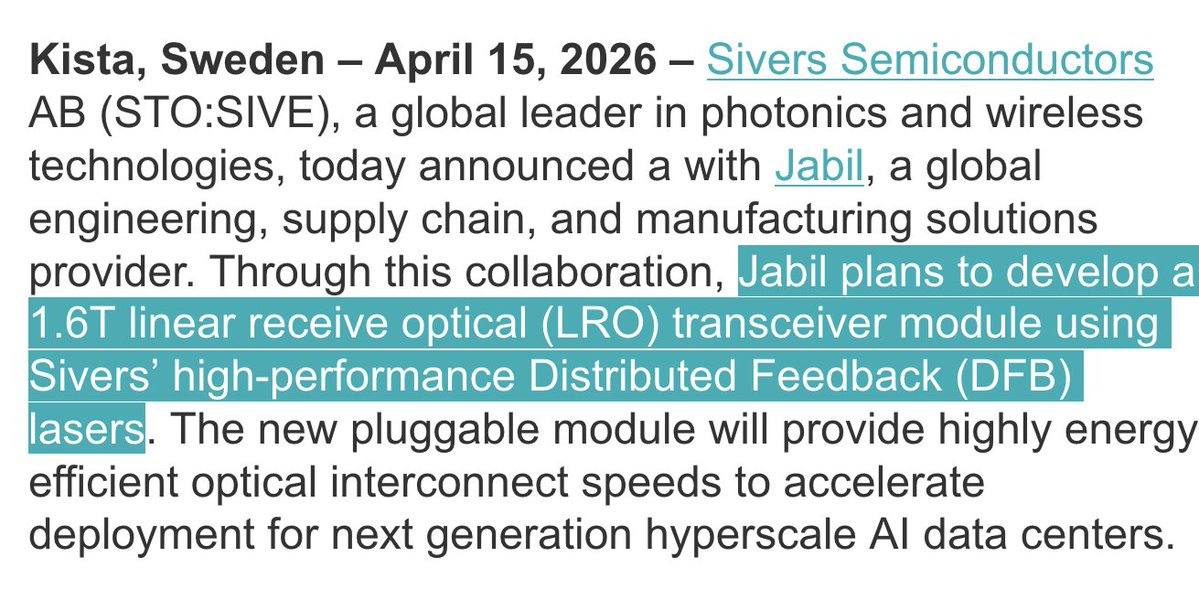

Frontrunning 1.6T/CPO within the broader photonics supercycle is the most compelling investment to me. I have high conviction in that statement. Which is why I'm long the entire supply chain (+1 extra bottlenecK) 1. $SIVE - Their laser revenue scales aggressively with $JBL, $MRVL, Ayar, O-Net. And I do think CPO/1.6T will blow away any conservative analyst projections from how hard $NVDA, $GOOGL, and others have been pushing photonics architectures. Downside risk is multi-sourcing, but there's a reason Jabil chose Sivers. When you compare $MTSI, $LITE, $COHR, Furukawa, and others. There's genuinely not many laser suppliers in the entire world... they're all $10B+, then you have this mini CHIPS act chokepoint trading at <$1B MC. 2. Shunsin (6451) - I don't see how it's possible Foxconn's optical foundry for testing, packaging, and assembly is valued at $1.5B MC less than $LWLG. When they look extremely derisked piggybacking off of Foxconn's photonics volume. $TSM's optical arm VisEra example is ~$5B, but they scale H2 2028 from Gen-3. Foxconn looks to be ramping up just next year. They're just scaling low fwd p/e multiples off of $NVDA CPO supply chain demand in Taiwan and all public indicators point to capacity expansion + extreme demand. 3. Win Semi - They're the foundry for Sivers to scale up DFB laser production. As well as $AVGO, SpaceX supply chains and others. When I do supply chain mapping and Win Semi pops up in every single frontier supply chain I see. There's probably something markets are not pricing in. 4. $MRVL - I find this genuinely compelling as a mini-Broadcomm. Their potential design with with $GOOGL today, helps the case past 2028. But the catalyst I was looking at was $MSFT Maia ramp, which happens H2 2026, and likely keep scaling up exponentially into 2027, 2028, 2029. Celestial acquisition was probably the smartest thing in the world for them. Maybe on next drop or CSP? 5. $HPS.A - Transformers/Switchgears are commodities + boring parts of the DC supply chain. However, when the bottleneck is 2-5 years, and you have backlog increasing 100%+... causing extreme shortages. It's only up 20%+ since my thesis post, but I do see this being de-risked given massive backlog visibility (even though it's inferred, they don't give exact #). I do think markets are missing something, especially with potential gross margin expansion from price hikes if they pull it off.... Again backlog + demand just de-risks this company, and it seems like a high growth compounder post facility expansion last year. There's many others like $NBIS, $JBL, $RPI, $TSEM, $LITE, $ARM, $SOI, $AXTI, $IQE, $ALRIB, Fittech, PCL, and others that I'm very fond of, but just mentioning 5 off the top of my head from today's prices... if I'm creating a new portfolio. Of course, it's good to barbell with other uncorrelated companies to AI supply chains, but these are just 5 I liked.

LPKF Laser are kinda interesting. Initial notes are: -> Owns LIDE - only 2-step laser + etch process hitting 5µm vias at 50:1 AR on glass panels. -> Every serious glass substrate player (SEMCO, SKC Absolics, LG Innotek, DNP, Intel) is a customer, partner, or in qualification. -> Their LIDE process is the only one hitting the spec envelope $AVGO/ $AAPL/ $NVDA ASICs actually require? -> €337M MC - seems to be priced as a solar-drag industrial laser co. Not as a chokepoint of the packaging transition. -> Pretty ugly P&L. I started a small position yesterday which I'll build out next week depending on how I feel when the time comes.

$EQR.AX Hinta saavutti tärkeän resistancen 0,36-0,39AUD alueen, jota testaillaan nyt jo kolmatta kertaa. Jokainen yritys on tehnyt alemmat huiput (lower high) sekä alemmat pohjat (lower low): Myyjät edelleen kontrollissa short term, kunnes tuo resistance rikotaan. > Daily Rsi myös painaa resistancea vastaan. Myyjät saapuivat viimeisellä tunnilla ja vastustaso toistaiseksi kesti vielä. Supporttina nouseva trendilinja ja sen lisäksi ≈0,3AUD tukitaso, jos ne rikotaan olisi tärkeää, että 0,265 tukitaso pitäisi ja hinta voisi tehdä double bottom/ korkeammat pohjat. (kuva 3) Tungsten / EQR hype X:ssä, sekä Usan ja Iranin välinen 2vk tulitauko ei toistaiseksi ole näkynyt niinkään osakkeen hinnassa, ainakaan odotusten mukaisesti. Jos tulitauko osoittautuu pelkäksi puheeksi lisämyyntipainetta todennäköisesti luvassa. #EQR #ASX #TUNGSTEN

@aleabitoreddit Whats next?

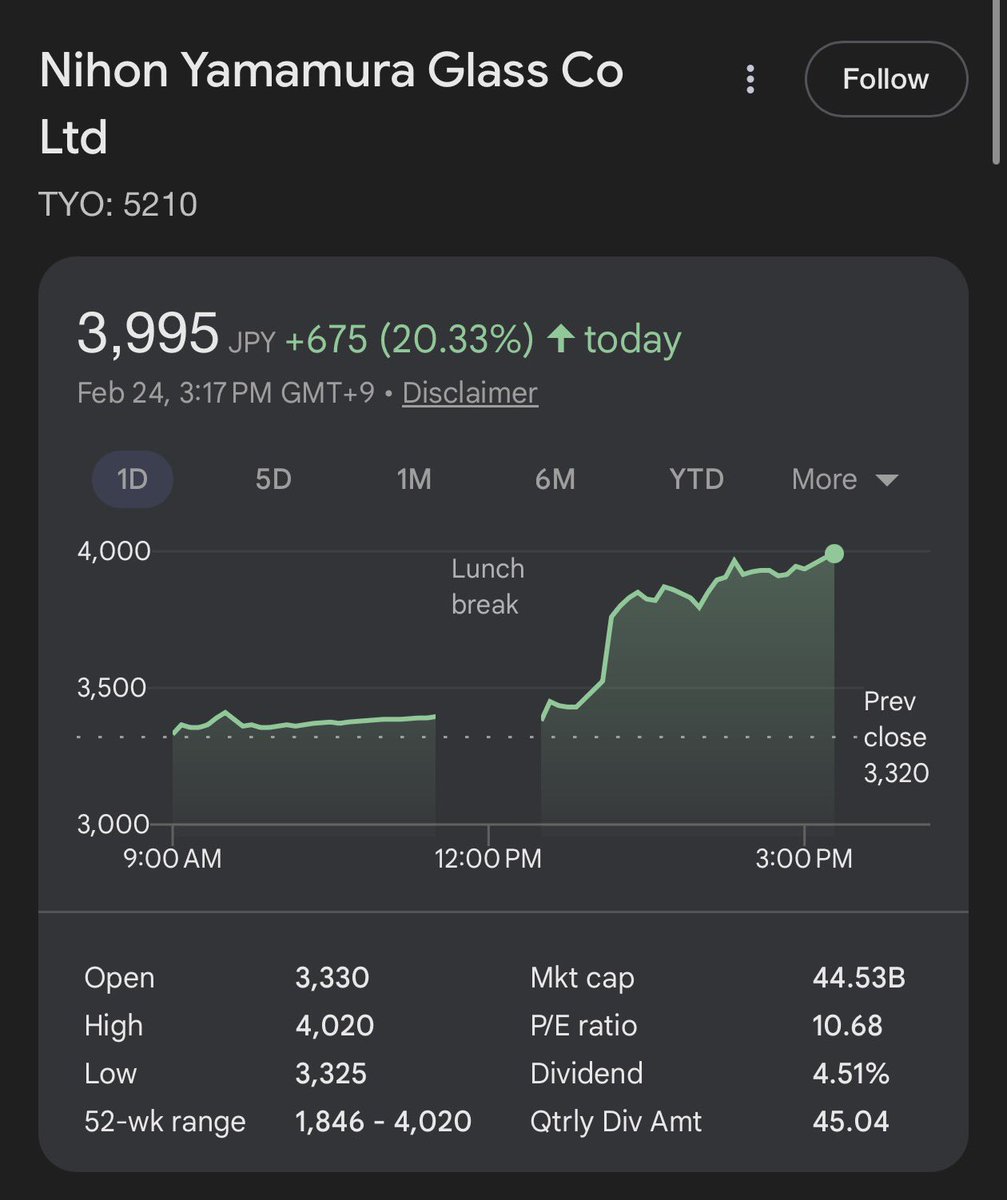

Took a closer look: Yamamura glass (TYO: 5210) is a banger. You’re basically buying the business for free? And their photonics division is growing 91% Y/Y for optical communication caps. You are paying $240M for a company that does $500M sales with $360M+ in actual book value (factories, equipment, cash) and a fast growing AI DC photonics division. Before this was a trap but -> they upped dividend amount to 5.5%, which is the biggest signal that value is now unlocked. And now from their Feb 12th earnings, they confirmed this was structural (not just one off that markets were fearing) It’s just wait and chill basically?