English

Max Tannone

13.6K posts

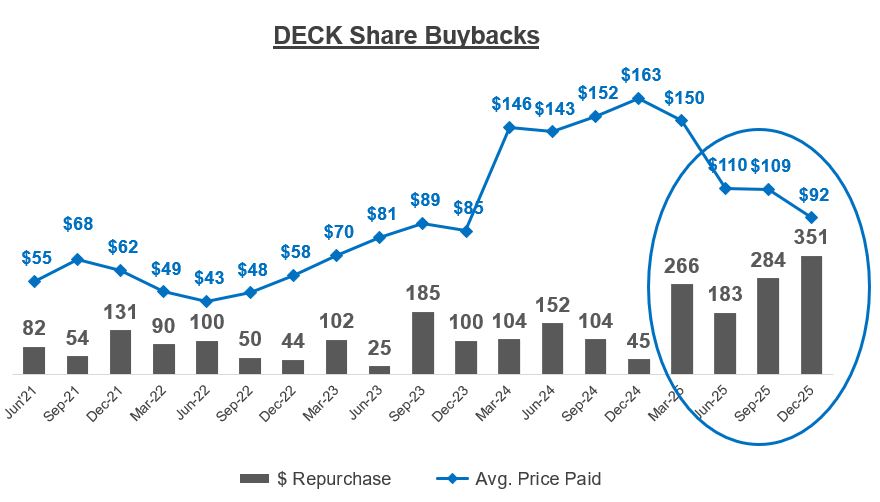

Shall we contribute to Top Ideas* for 2026? Recap: 2025 $GTX +99% “Turbocharged industrial” 2024 $LSXMK ( $SIRI) -(38)% “The Dogstar” 2023 $AER +158% “Compounding aerospace shortages” 2026: Top Idea $DECK Deckers Outdoors $DECK was one of the worst performers in the S&P 500 in 2025, down -(49)%. The stock price collapsed, but the business did not. At a ~16x P/E ratio (14x net of cash) Deckers is being valued like a cyclical apparel company, not a compounding brand platform with a demonstrated history of operating leverage. If Deckers can sustain high-single digit revenue growth then operating leverage and buybacks will deliver high-teens EPS growth, even before multiple expansion. The key risk is not that Deckers is a bad business; it’s that investors mistake category headwinds and temporary margin pressure for a permanent EPS growth slowdown. Business: Deckers Outdoor designs, market and sells innovative footwear and apparel for casual lifestyle use and high-performance activities. Deckers sells fashion, authenticity, functionality, quality, and comfort. The company has three core brands: UGG, HOKA and Teva Coming into the 2025 to forget, Deckers had a remarkable run. The stock price soared +450% from mid-2022 until 30 Jan 2025, having been added to the S&P500 in the fall of 2024 and undergoing a CEO handover when Dave Powers retired. At its apex, $DECK reached a 38x trailing P/E ratio on its guidance of $5.85 earnings. Delivering $6.33 for FY26 was deemed insufficient and the general consumer sell-off, tariffs and the belief in the re-emergence of Nike led to a substantial downward re-rating in 2025. Putting aside the stock chart, Deckers has proven itself by nurturing HOKA since it was acquired for $1.1 million in 2012 into a mult-billion dollar product brand alongside its seasonal cash cow UGGs. Valuation & Growth: Today $DECK is priced at $103.67 giving it a $15 billion market cap, no debt and $1.4 billion of cash ($9 per share). $DECK trades at a ~16x P/E ratio and ~14x P/E net of cash. $DECK’s trailing 5-year revenue and EPS CAGR was +18% and +32% EPS growth to $6.33 per share. Tariffs (Vietnam at 20%) were a substantial gross profit and net profit headwind in 2H’25 and current guidance calls for +7.5% revenue growth and ~flat profit growth in FY26. Deckers historically has profit growth far exceeding revenue growth due to operating leverage and they tend to be very conservative in their financial guidance. Deckers commitment to share repurchases (~2.5% annual net float reduction) and more aggressive recent pace accelerates EPS growth and takes advantage of present mispricing. Gross margins fluctuated between 50-58% since COVID and Operating margins ranged from 18-24%. $DECK generates substantial free cash flows as its nearly $1 billion of earnings converted into free cash flow with some only modest capex for distribution, store expansion and inventory builds to support higher sales. "Our confidence in our brands has not changed, and the long-term opportunities ahead are significant." - CEO Stefano Caroti 2Q25 $DECKs ~16x P/E ratio valuation needs to be put in the context of its growth. How many companies in your portfolio have delivered a 5-year EPS CAGR of ~33%? It’s ROE (net of excess cash and without debt leverage) exceeds 50%. Simply: $DECK ’s top line revenue growth is the engine that pulls the train. HOKA HOKA has reached $2.2 billion in annual sales with a +36% 3-year CAGR and +45% 5-year trailing. I estimate HOKA can sustain low-double-digit growth rates over the medium-term. UGG UGG has reached $2.5 billion in annual sales with a +8% 3-year CAGR and a +11% 5-year CAGR. I estimate UGG can sustain mid-single-digit growth rates over the medium-term. ~2/3 of Deckers sales are in the USA, resulting in a substantial headwind in 2H’25 & 1H’26. Sales growth and $5 price increases should create enough gross profit dollars to mitigate the tariff $ impact, but profit growth is impacted. Similar to $LULU, Deckers USA and DTC growth also slowed substantially in 2025 while International growth sustained double digits. Over time, management has guided to a 50/50 sales split as a result of international expansion (Europe, China, Asia, etc.). Deckers ability to manage the cyclicality of its UGG franchise has built robust relationships and unique capabilities to manage its supply chain and demand-pull model. Applying these learnings to HOKA has enabled it to both supercharge growth and now sustain brand heat in the face of increasing competition. Catalysts: 1. Time and valuation. Continued growth of its core brands HOKA and UGG, return to operating leverage following USA tariff imposition and accretive share repurchases at a 16x P/E are likely to prove the current valuation too conservative. 2. Continued top line growth. International expansion can enable continued high-single or low-double-digit topline growth over the medium-term. USA can return to growth. 3. Operating Leverage resumes. Lapping 20% Vietnam tariffs at midyear should allow Deckers to return to its algorithm of growing earnings faster than revenues through operating leverage. 4. Accretive buybacks. Similar to $LULU and $CROX, Deckers has become increasingly aggressive about repurchasing shares at reasonable valuations. Having averaged ~2.5% net buybacks over the past several years, the recent increase in pace and $2.5 billion Board buyback authorisation can enable nearly all of earnings to be directed to share repurchases, maintaining a robust balance sheet and enabling mid-single digit share count declines. Risks: 1. The thesis breaker: Competition 7936.JP ASICS has always made a reliable, heavy-duty Japanese-inspired gel running shoe. In the last few years they’ve done an increasingly good job of copying the foam, form, function, styles and colors of HOKA. Innovation is HOKA’s best defense against this reliable giant. $ONON has taken the high-end lifestyle market by storm. Lineup is less competitive on function, but wins the urban environment on form and style. They’ve the biggest threat to Nike’s core markets. $NKE Nike is the $50 billion iconic sports giant. Many articles cover their distribution and leadership troubles and tout their coming innovation. Vomero is a solid HOKA imitator, bringing Nike colors, design and marketing, but remains a show me story. Alphafly and carbon designs continue to dominate the elite and amateur road racing scene. $BRK.B Brooks Running. Reliable performance shoes that outperform in their core niche among American women. $BIRK sandals and clogs are a core personality signaling totem for certain segments and remains a notable competitor for UGGs as it expands into summer and spring silhouettes. Overall there are many competitors, each with strengths and weaknesses in their targeted niche (urban style, elite performance, everyday casual runner, trails, etc.). HOKA has carved its niche in the off-road trail markets through its UTMB affiliation and proven trail racing models. It will require continued innovation, marketing appeal and execution to grow beyond its roots. 2. Execution 2025 HOKA execution was negatively impacted by an overlapping release cadence of core styles with similar silhouettes. Designing innovative products for HOKA and UGG combined with unique styling, colors, and authentic market that resonates consumers while sustaining a demand pull (scarcity) model is no easy task but vital to sustained business success. Failure to innovate on product and drive brand heat, not tariffs, FX or macro noise is the key risk to slowing Deckers growth flywheel. 3. M&A Ever since its 2017 encounter an activist investor Deckers has been increasingly focused on delivering its core brands and has not been tempted by M&A. They have built a fortress balance sheet and stuck with accretive share buybac $CROX Heydude is a case in point of why not to pursue debt funded acquisitions. Summary: With an exceptionally high-ROE, proven operating leverage and disciplined capital allocation $DECK can outperform for many years by delivering high-single-digit revenue growth and mid- to high-teens EPS growth followed by multiple re-rating. Returns from $DECK are not derived from forecasting the next quarter but by allowing a proven business time for its fundamentals to compound during periods of market skepticism. *Ideas area presented at their then current trading price with the objective of holding and achieving strong returns over 1, 3 and 5+ years. Continue to hold all previous “Top ideas”.

I started my career during the throes of the GFC crisis, working on CDOs / CLOs / RMBS / CMBS. This gave me one of my earliest mental models, which I light-heartedly call “everything is bond math” - the ability to see that most financial assets with streams of cash flows are simply bonds in disguise. It’s proved useful for me. Let me share a few observations: 🧵1/8:

This is the first time in my life I’ve been net short crypto