@KlendathuCap Parts of the Shining would be especially cool given the way the Overlook layout defies logic/physics.

English

Chaos is a ladder

4.1K posts

@mcgill_s

Portfolio construction, equity, risk-management.

I present to you "Make the 1970s Great Again" featuring "Too Late" by Carole King Find your 1970s crisis vibe

Saturday Poll. The next 100 points for the S&P?

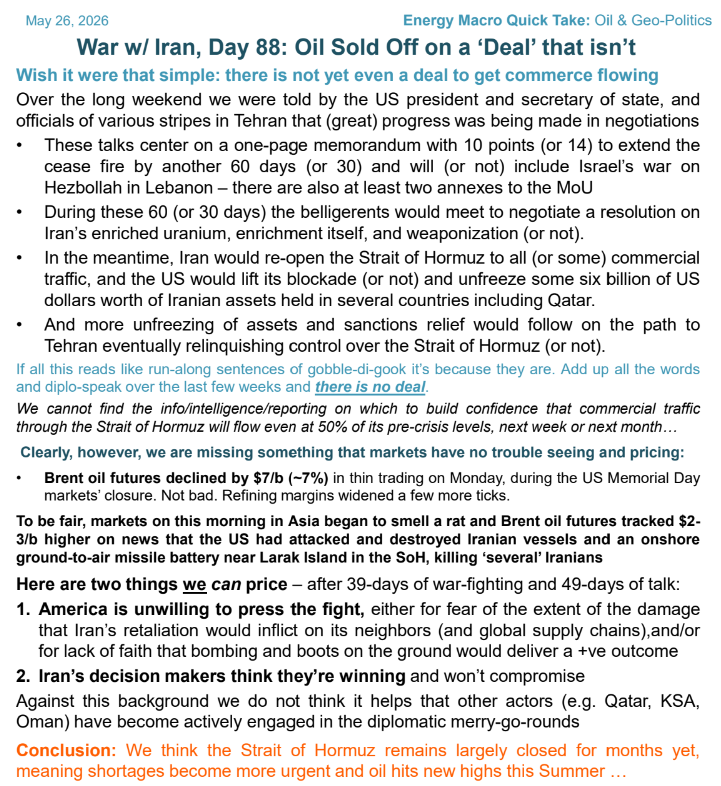

Just went through the latest OIES report on what’s been happening in the oil paper market over the last three months. Here’s the breakdown: 1) In a typical geopolitical scare, you'd expect spec money to pile in and send open interest through the roof. Instead we witnessed a complete anomaly: Brent futures open interest absolutely cratered. 2) On the flip side, daily volumes actually went through the roof. It shows everyone was aggressively passing the hot potato intraday to shift risk, but nobody had the stomach to hold overnight exposure. And now even that day-trading volume is drying up fast. 3) Money managers like hedge funds and CTAs live for trading time, arb, and product spreads based on real oil fundies. But once the war sent vol off the charts, it blew straight through their internal VaR limits. Facing massive margin hikes, they were forced into a structural retrenchment. The capital cost of just holding onto those positions became way too expensive. 4) When the geopolitical conflict flared up, North American shale independents found themselves severely under-hedged. As crude prices ripped higher, they panicked to lock in those attractive margins, offloading massive swap volumes to their bank counterparts. This clearing activity forced a structural expansion in the CFTC data, leading to a concurrent spike in swap dealer shorts and offsetting commercial long exposure across the WTI curve. 5) The Brent-WTI blowout triggered by the Hormuz crisis blew the physical arb wide open for moving North American barrels into Europe and Asia. To nail down those arbitrage margins, mega physical trading houses executed a 'Long WTI / Short Brent' spread trade, which acted as a critical floor for WTI open interest. 6) ICE blunt-force doubled Brent margins, while CME played it smart by using its SPAN system to give massive portfolio-based risk offsets on inter-commodity spreads. On a pure capital-efficiency basis, it was a total no-brainer to park your margin in WTI instead of Brent. 7) As open interest fled the futures complex, everyone piled into options to keep chasing directional plays with a hard stop on risk. Going long premium meant your downside was strictly capped at the premium paid—no brutal daily mark-to-market margin calls, which saved your balance sheet flexibility. Operationally, it was a massive relief because you didn't have to stay awake 24/7 babysitting a position overnight. Shorting options, though, was absolute suicide thanks to that nasty convex risk and punishing margin hikes. 8) Trading in ultra short-dated paper absolutely exploded as players scrambled to chase headline risk in real time. This April weekly WTI options saw average daily volumes skyrocket to around 33,000 contracts, up nearly 50% y/y. 0DTE options squeezed their market share up from 25% to 30% of the entire WTI options complex, while 1-3 DTE contracts also expanded their footprint from 34% to 39% #oott #iran