Nicholas Kosinski retweetledi

Nicholas Kosinski

50 posts

Nicholas Kosinski retweetledi

Dear AI bears: this is not the dot-com bubble 2.0

Why today’s AI build-out looks nothing like 1999 and what that means for investors

Every time the Nasdaq makes new highs, bears compare the AI revolution to the dot-com bubble. It’s an easy comparison, but if you actually look under the hood, it doesn’t hold up. Yes, there are speculative corners within AI and some of those stocks will get crushed but that can be said about any market. The core of today’s AI build-out is being driven by some of the most profitable companies in history, funding long-duration infrastructure out of cash flow—not fragile startups living off endless equity raises.

If you want to understand whether this is really 1999 again, you have to start by remembering what dot-com actually was.

What really drove the dot-com bubble

The 1990s were a genuine technological revolution. The internet went from an academic network to a mainstream platform thanks to browsers like Mosaic and Netscape. Between 1995 and 2000, the market surged 400–500%, and suddenly anything with a “.com” in its name could command a multi-billion-dollar valuation.

The problem wasn’t the underlying technology. It was the way capital was deployed on top of it. Many of the high-flying names had no profitability, minimal revenue, and in some cases literally no revenue at all. Traditional valuation metrics were discarded and the mantra became scale first, worry about profits later.

Investors convinced themselves that the internet would create winner-take-all markets, so any price could be justified for the perceived winner. Venture capital firms raised enormous funds and had to put money to work. A competitive race among VCs led to faster dealmaking, thinner diligence, and ever-higher valuations.

The playbook was simple and reckless: spend aggressively on marketing, undercut prices, and acquire users at any cost. Burning cash wasn’t a red flag; it was almost a badge of honor. The assumption was that once dominance was achieved, profitability would magically follow.

Heading into 2000cmany dot-com companies had deeply negative operating cash flow and no credible path to positive earnings. Their survival depended on an endless stream of fresh capital which included venture funding before an IPO, secondary offerings and convertible debt after the IPO. That made the whole ecosystem overly sensitive to shifts in sentiment and macro conditions. A fragile business model + extreme valuation is the exact recipe for a bubble.

How the dot-com bubble actually popped

Bubbles can survive a long time before it bursts. In 1999–2000, several catalysts hit almost at once. The Federal Reserve raised rates by 175 basis points between June 1999 and May 2000, increasing discount rates and making safer assets more attractive relative to unprofitable dot-com companies. The Nasdaq peaked on March 10, 2000, at 5,048.

Soon after, Japan slipped back into recession, rattling global markets. MicroStrategy’s accounting restatement highlighted how aggressive some earnings claims had become. Barron’s ran its now-famous “Burning Up” piece, pointing out that many dot-com companies were literally going to run out of cash. At the same time, the Microsoft antitrust case reminded the market that even dominant tech firms operated under regulatory risk.

When the mood shifted, the IPO window slammed shut. Secondary offerings dried up. Venture capital became more selective. Companies that had been reliant on constant capital infusions suddenly had no room to operate. The Nasdaq fell roughly 78% from its March 2000 peak to its October 2002 low.

Leverage made everything worse. Many investors had bought hot tech names on margin, and as prices fell, margin calls forced them to sell into a declining market. Hedge funds running leveraged momentum strategies were forced to unwind. The result was not a gentle re-pricing; it was a cascade of forced selling.

On top of that, the telecom and infrastructure side of the boom turned out just as fragile. Telecom operators had borrowed heavily to build out networks. When demand and pricing disappointed, they were left with excess capacity and crushing debt loads. WorldCom, Global Crossing, NorthPoint and others went bankrupt, wiping out equity holders and inflicting major losses on creditors. That feedback loop between collapsing equity values and credit stress deepened the downturn and amplified the dot-com crash.

If you’re trying to map that entire setup onto 2025 AI, you’re starting from the wrong base case.

Why the AI build-out is fundamentally different

The single biggest difference between the dot-com era and now is simple: who is doing the spending, and how they’re funding it.

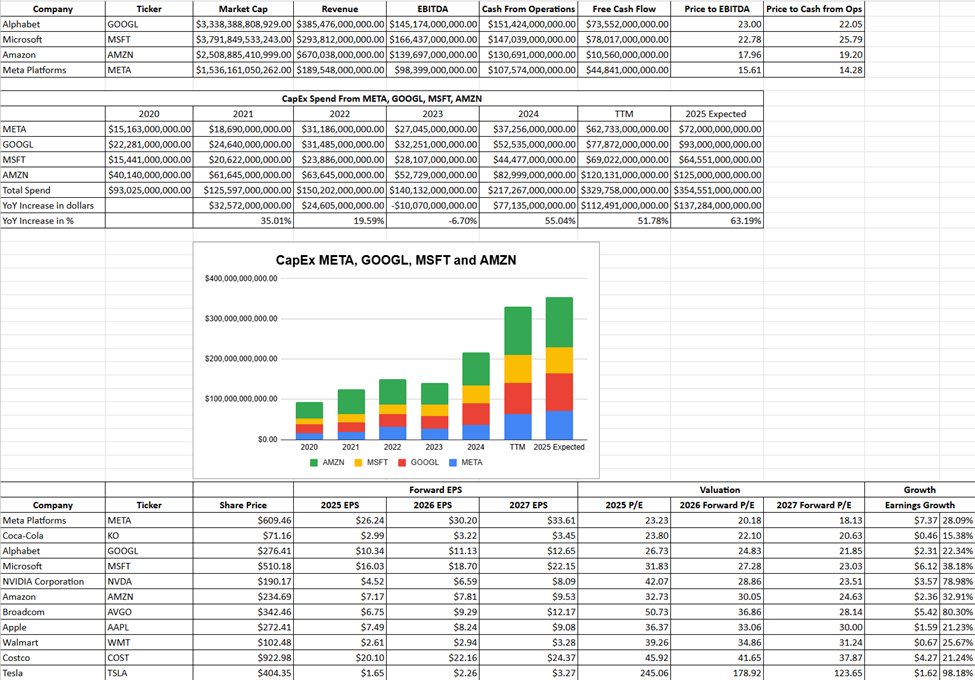

The core of the AI boom is not a swarm of tiny, unprofitable companies betting everything on a single idea. It’s a handful of massive, hyper-profitable platforms including $MSFT $AMZN $GOOGL $META deploying record capex into cloud and AI infrastructure which is largely being funded by internally generated cash flow.

If you want to stress-test the AI story, don’t look at the tiny speculative names first. Look at MSFT, AMZN, GOOGL, and META. Their earnings reports tell you more about the durability of this cycle than any meme stock catching an elevated valuation.

In the most recent quarter (Q3 2025 for AMZN/GOOGL/META, Q1 for Microsoft), these three cloud/AI giants MSFT, AMZN, and GOOGL generated about $97.3 billion in revenue from their cloud/AI divisions alone. Collectively, they reported roughly $755 billion in backlog tied to these businesses: approximately $400 billion at Microsoft, $200 billion at Amazon, and $155 billion at Alphabet.

Backlog is critical as it’s not capex. It’s contracted or committed customer demand dollars customers are planning to spend on these services over time. That demand is what’s driving these companies to commit unprecedented sums of capital to data centers, networking, and AI infrastructure.

The big four by the numbers

You don’t have to guess about demand; you can see it in the operating results. I believe that the bears who are trying to correlate the AI revolution to the dot-com bubble haven’t gone through the latest earnings reports which reveal just how much demand there really is.

MSFT: Microsoft Cloud revenue reached $49.1 billion in Q3, up 26% year-over-year. The Intelligent Cloud segment, which includes Azure, generated $30.9 billion in revenue, up 28%, and is now running at roughly a $123 billion annualized rate with $13.4 billion in quarterly operating income. Commercial remaining performance obligation (RPO) has grown more than 50% to nearly $400 billion, with a weighted average contract duration of just two years. On the product side, Microsoft is using Azure AI Foundry to help customers build AI applications and agents. Foundry already has tens of thousands of customers, including the vast majority of the Fortune 500. Across its ecosystem, Microsoft has hundreds of millions of monthly active users of AI features, with first-party Copilots representing a rapidly growing share.

GOOGL: Google Cloud revenue grew 34% year-over-year to $15.2 billion, and cloud backlog increased to roughly $155 billion, up sharply from a year ago. Google has signed more billion-dollar cloud deals in the first nine months of 2025 than in the previous two years combined. Its Gemini models are handling massive volumes of tokens via API and consumer interfaces, with the Gemini app and AI Overviews touching hundreds of millions to billions of users. Enterprise adoption is also ramping, with millions of paid seats across a broad base of companies.

Amazon (AWS): AWS revenue increased 20% year-over-year to $33.0 billion and is now operating at an annualized run rate of roughly $132 billion. Over the past 12 months, AWS has added several gigawatts of power capacity which is more than any other cloud provider and plans to double total power capacity by the end of 2027. Backlog has climbed to around $200 billion. AWS launched AgentCore, a set of infrastructure building blocks for secure, scalable AI agents, and has already seen hefty developer adoption. On the retail side, Amazon is deploying AI throughout the business from tools that help millions of sellers create better product listings to Rufus, its AI shopping assistant. Rufus now serves hundreds of millions of customers and is on track to deliver billions in incremental annualized sales.

Meta: Meta is a reminder that AI isn’t just about cloud and infrastructure it’s also about monetization on top of those platforms. The annualized revenue run rate flowing through Meta’s AI-powered ad tools has already surpassed $60 billion. Meta is working on unifying three major AI systems which include Facebook, Instagram, and ads recommendations into a single model architecture (Lattice). More than a billion people are already interacting with Meta AI features across the family of apps.

These are not companies telling “maybe someday” stories. They are reporting real revenue, operating income, and contracted demand tied directly to AI and cloud.

Follow the cash, not the hot takes

The strongest argument against “AI = dot-com 2.0” isn’t just the top-line growth, it’s the cash flow. Look at the core financials of these four businesses over the trailing twelve months:

Together, MSFT, AMZN, GOOGL, and META have generated roughly $1.54 trillion in revenue, $549.71 billion in EBITDA, $536.73 billion in cash from operations, and $206.97 billion in free cash flow (FCF). Over that same period, they spent $329.76 billion on capex and still produced over $200 billion in free cash flow after that spending.

In 2024 alone, they spent $217.27 billion on capex, an increase of about $77 billion (55%) year-over-year. Over the trailing twelve months, capex climbed to $329.76 billion, up another $112.49 billion (about 52%) above 2024 levels. Based on recent management commentary, combined capex for these four is expected to reach roughly $354.55 billion in 2025 which is more than 60% above 2024 levels.

Bears look at those capex numbers and see a bubble. They try to map today’s spending directly onto the reckless telecom/infrastructure build-out of the late 1990s. The problem with that analogy is that this spending is not being funded by speculative venture debt or serial equity offerings. It’s being funded by rising operating cash flow at four of the most profitable companies in the world.

This is not one highly leveraged player betting the farm on a single unproven idea. This is a group of trillion-dollar platforms, with diversified revenue streams and fortress balance sheets, responding to clear, measurable customer demand in cloud and AI.

Ask yourself: what are the odds that the bears sitting on the sidelines have a better read on optimal data center spend than Andy Jassy, Mark Zuckerberg, Sundar Pichai, and Satya Nadella?

The valuation puzzle

If this really were a full-blown bubble, you’d expect the core AI infrastructure names to be trading at nosebleed valuations that imply perfection for a decade. That’s not what the market is actually pricing.

Based on forward EPS estimates, META, GOOGL, MSFT, $NVDA, AMZN, $AVGO, and $AAPL do not look wildly expensive relative to high-quality non-tech staples. In fact, when you look at the 2027 estimates, many of these AI leaders trade at lower forward P/Es than retailers like $WMT and $COST.

The market is comfortable assigning more than 30x earnings to companies like COST and WMT, while assigning under 25x 2027 earnings to companies like META, GOOGL, MSFT, NVDA, and AMZN that are sitting at the center of the AI and cloud build-out. You can reasonably argue about whether all those earnings estimates will be hit but calling that setup a “bubble” stretches the word beyond meaning.

For instance, AMZN is expected to generate $7.17 of EPS in 2025 and $9.53 in 2027 which is an increase of 32.91% over the next 2-years and trades at 24.63 times 2027 earnings. Does that seem unreasonable considering WMT has 25.67% EPS growth and COST has 21.24% EPS growth over the same period yet trade at 31.24 and 37.87 times 2027 earnings? NVDA has 78.98% of projected EPS growth over the same period and trades at 23.61 times 2027 earnings. When I look at the projections from The street the argument that we are in an AI bubble loses credibility.

Where the real bubble risk actually is

There are absolutely pockets of the market which that look and feel expensive. We are seeing companies with tiny revenue bases, no profits, enormous TAM slides receiving sky-high valuations as investors pile into them. Some of those names are going to experience brutal round-trips. But that’s very than the AI cycle being equivalent of a dot-com bubble. Most of these speculative names are not in major indices. Those that are often have such small weights that even a 50–90% drawdown in their share prices would barely move the S&P 500 or the Nasdaq. Traders and speculators in those names will feel real pain if and when the air comes out.

What it won’t do is suddenly erase Microsoft’s $400 billion cloud backlog, or Amazon’s $200 billion AWS backlog, or Alphabet’s $155 billion cloud backlog. It won’t retroactively make Meta’s $60+ billion AI ad run rate a mirage. And it won’t stop these companies from continuing to build out infrastructure as long as they see durable demand and attractive returns on capital.

The Bottom Line

If your entire bear case rests on “this looks like 1999 again,” you may be anchored to the wrong historical analogy. Dot-com was a story of fragile, cash-burning business models financed by an endless chain of new investors. Today’s AI cycle is a story of cash-rich incumbents reinvesting enormous free cash flow into infrastructure to meet committed demand.

None of that means AI is risk-free as Capex cycles have the ability to overshoot while competition intensifies. Multiples can compress even if earnings grow. There will be individual winners and losers, and owning the wrong high-flyer at the wrong time will still hurt.

If you’re waiting for a 2000-style wipeout in mega-cap tech as your entry point, you might be waiting for a crash that belongs to a different era. Today’s market is one where the world’s most profitable businesses are trading at reasonable forward multiples while funding one of the largest infrastructure build-outs in history from their own cash flow. That’s not the dot-com bubble 2.0. and to put it nicely, the bears are wrong trying to correlate the AI revolution to the dot-com bubble.

@amitisinvesting @KrisPatel99 @RealMattMoney @Futurenvesting @FunOfInvesting @dhurstell @_financeken @DanIvesprivate @fundstrat @Kross_Roads @StockMarketNerd @sam_badawi

English

Nicholas Kosinski retweetledi

Nicholas Kosinski retweetledi

History shows us that having too much debt during an economic downturn leads to a classic, self-reinforcing cycle where:

1) The empire can no longer borrow the money to repay its debts

2) It prints a lot of new money, which devalues the currency and raises inflation

3) Living standards decline, leading to the rise of political extremism

4) Turbulent economic conditions undermine productivity and there is conflict about how to divide the shrinking resources

5) Populist leaders emerge pledging to take control and bring about order

English

Nicholas Kosinski retweetledi

A guy just used @AnthropicAI Claude to turn a $195,000 hospital bill into $33,000.

Not with a lawyer. Not with a hospital admin insider.

With a $20/month Claude Plus subscription.

He uploaded the itemized bill. Claude spotted duplicate procedure codes, illegal “double billing,” and charges that Medicare rules explicitly forbid. Then it helped him write a letter citing every violation.

The hospital dropped their demand by 83%.

This isn’t just a feel-good story. It’s a preview of what AI will really do next: flatten systems built on opacity.

Hospitals, insurance companies, legal firms—all rely on asymmetry. They win because you don’t have access to the same data, code books, or language.

Claude gave one person the same leverage as a compliance department. That’s a revolution.

We thought AI would replace jobs. Turns out, it’s replacing excuses.

English

Nicholas Kosinski retweetledi

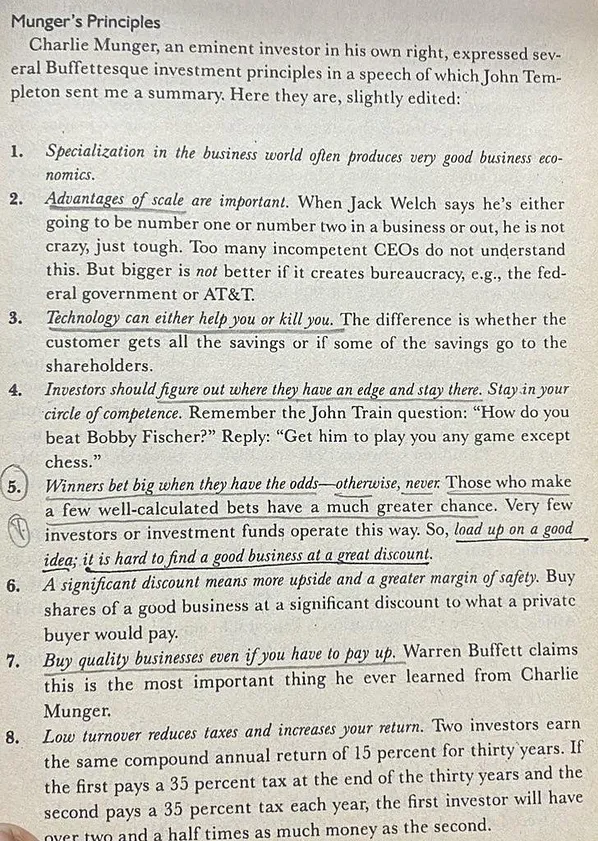

I think this is superb advice. Worth a careful read:

Michael Milken – Lessons on Money, Family, and Success

(Forum for Family Asset Management, Milken Conference, Mexico City –

paraphrased notes)

Spend time with your kids — you’ll pay for it (for better or worse) either now or

later.

Think about how you measure meaning and success in your children and

grandchildren. Give them purpose.

For children raised in very successful households, it’s often hard to emulate

success — especially financial success.

Most successful people are too busy to see their kids and grandkids. That

absence shows up later in life.

The center of success is the ability to dream.

Real success is the freedom to live your life.

The financial media is obsessed with lists. Forbes today is mostly about

ranking wealth by dollars.

There are countless stories of wealthy people who never had a good day with

their kids.

You’re only as happy as your least happy child — think about that often.

He shared a story about a wealthy Chicago family whose fortune was divided into 1/13th shares after one heir demanded his part. That decision ended up dividing the entire family.

Be careful not to do something that provides financially but destroys the

family.

The most important thing to teach children is financial literacy.

The greatest failure among wealthy families is not providing financial literacy to their members.

Example: an extremely wealthy Latin American family where the

great-grandfather is still alive — his mindset is completely different from that of his great-grandchildren.

In Asia, inheritance traditionally went only to men — that has changed in

recent decades.

Recommended reading: Economic Mobility Program – Invest in America.

Example: Apollo bought the Venetian Hotel and gave all 7,000 employees

stock. They paid a dividend the first year through a recap — everyone saw it as a “Christmas bonus.” The next year, when there was no dividend,

employees were upset. No one had explained the difference between a

dividend and a bonus.

The biggest mistake over the last 50 years has been financial illiteracy — not understanding the business or the source of wealth. Families and employees both need to learn this.

Best example of a united family: an Austrian family that’s 11 generations old. They own a resort used only by the five branches of the family. Ownership

rotates every three years. To be invited when your branch isn’t in charge, you

must get along with the others.

No matter how much you build or earn, what truly matters in the long run is

your relationship with your kids and grandkids.

Define what success means to you — it’s what makes you happy.

Entrepreneurs don’t just build companies; they can build nations or religions.

One of the most successful entrepreneurs in history is Lee Kuan Yew.

It’s not about how many things you own.

If you’ve never been responsible for making payroll, your view of the world is very different.

Hug your kids and grandkids. Let everyone find their own path.

Children growing up around success feel enormous pressure. Remind them

how valuable they are.

Let kids make mistakes when the stakes are low — not high.

English

Nicholas Kosinski retweetledi

I've been wondering for a while: Where is Costco for Software?

There is something honest about Costco. For decades they have delivered high quality product for low prices. They don't sell "brand" or hype- they sell quality in mass. That's why it is one of my all-time favorite companies, both as an admirer of the business and also as a customer. It's probably also why Costco is approaching half-a-trillion dollars in market cap.

It name says it all: Costco is the "Co" all about "Cost." For decades, Costco has committed to keeping their margins low. Very low. In fact, they have an unofficial cap of 15% gross margin on most products. Compare that with the 70-90% gross margins we've come to expect in software and you may know where I am going here.

The 15% margin cap is a powerful principal. Here's a story from Costco lore: Costco bought 2 million designer jeans for an all-in price of $22 per pair. This was $10 less than the firm had sold the same jeans for in the past (about $32). This meant they could keep the $32 price and enjoy a ~50% mark-up on the jeans and no customer would no the difference. Plus, they could feel morally good because they were still selling the jeans for half the cost of other retailers. An exec at the company recommended they keep the $32 price tag. But Costco’s founder James Sinegal would have none of it. He intervened and insisted that they mark up the jeans just 14% to $25. His was that the "contract" with the customer - very low prices and an unofficial 15% margin cap - must never be broken.

This is in large part why customers love the company. Costco's Net Promoter Score (NPS, a metric that measures customer loyalty and satisfaction) leaves other retailers in the dust and even exceeds that of Amazon in most surveys:

There are many NPS scores for Costco, but Comparably for example shows Costco as #1 globally and ahead of all it's retail competitors.

Where is this DNA in our software industry? Software margins are usually 70-90%. No margin stays at 70-90% forever. Who is building the Costco of software?

My guess is that this might be part of the vision with X.com, starting with social and then bundling the "everything app" consistent with Elon's 25-year vision. Driving down costs until it is the low cost provider- now that's a huge competitive advantage.

Google is also well positioned to do this and launches software products at a fast clip with low prices. They have a deep cost advantage, but they may already be hooked on their insanely good margins as a public company.

On the startup side, I'm pretty inspired by Odoo. They seem to have a Costco-esque approach.

Curious what you think?

English

Nicholas Kosinski retweetledi

Exactly right. ALL government spending is taxation.

The government either taxes you directly or, by increasing the money supply, taxes you through inflation.

That means the spending bill IS the taxation bill. Very important concept to understand.

@RepThomasMassie

Natalie F Danelishen@Chesschick01

🎯🎯🎯🎯🎯🎯 It's also a way for the government to grow in power and gain control over individual citizens' lives.

English

Nicholas Kosinski retweetledi

Marc Andreessen about Elon Musk $TSLA

“Elon identifies the biggest problem that the company is having that week, and he fixes it, and then he does that every week for 52 weeks in a row

And then each of his companies has solved the 52 biggest problems that year, and you know, most other large companies are still having the planning meeting for the pre-planning meeting for the board meeting, for the presentation”

English

Nicholas Kosinski retweetledi

Banks in the United States are inherently intertwined with and dependent on the government via the Federal Reserve’s discount window. As such they are quasi-governmental entities. They need to act like it, or they need to have their government funding pulled, and go under.

English

Nicholas Kosinski retweetledi

Nicholas Kosinski retweetledi

Student loan forgiveness sounds great for borrowers overburdened with high interest rate debts they cannot repay. The problem is that the subsidy appears to go principally to more affluent families at the cost of burdening those who didn’t attend college or whose parents saved to send their kids to school.

It should be illegal for a president to buy votes by transferring funds from certain citizens to others he believes are more likely to support him in an election.

Phil Kerpen@kerpen

Penn-Wharton: Biden's new student loan plan will cost taxpayers another $84B, bringing total to $559B. The biggest winners are 750,000 people with 20 years in repayment. Their average debt relief is $25,500+ and average household income is $312,000+. static1.squarespace.com/static/55693d6…

English

Nicholas Kosinski retweetledi

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

English

Nicholas Kosinski retweetledi

Taylor swift has burned almost 150 TONS of jet fuel visiting her boyfriend…

STFU about climate change.

English

Nicholas Kosinski retweetledi

👀🤡🌎 ... is anyone really surprised that the social media platform controlled by the FBI and CIA would do this?

English

Nicholas Kosinski retweetledi

On Nov 22nd, Nancy Pelosi and her husband bought Nvidia, $NVDA calls, a leveraged bet Nvidia would go up.

Since then, Nvidia is up 77%. Her calls have made her $1.3 million, over SIX times her salary in 78 days.

I want to give you the history of Pelosi, her $NVDA trading, and show the conflicts of Congress:

Let’s start in December 2021. After a history of unusual trading, from Visa, trading during the GFC, and buying before stimulus bills, Nancy Pelosi was asked if she thinks US Congress members should trade despite legislative conflicts by Bryan Metzger.

She said, "We are a free market economy. Congress should be able to participate in that". Insane.

In Jan 2022 Unusual Whales releases their most famous trading report, showing Congress beat the market. Nancy Pelosi is listed as the fifth best trader in Congress.

That report creates a flurry of media and outrage, while the report continues to go viral. Within seven days of publishing, five new bills banning members of Congress from trading are proposed.

In the summer of 2022, it is revealed that Nancy Pelosi was trading millions of dollars of $NVDA, Nvidia before voting on a US semiconductor bill by the Biden administration.

We reported on her trading to outrage by the public. Interestingly, for the first time in history, a few days later Nancy Pelosi disclosed trades made on the same day they were made. This is likely the fastest disclosure in history of US Congress. She reported that she sold out of her Nvidia position, the first time she divested from conflicts in her portfolio. Despite taking 45 days for every other disclosure, she made this one instantly. Hilarious.

One month later Nancy Pelosi proposed alongside Representative Lofgren her own Congressional trading ban, a bill which was incredibly weak and filled with loopholes.

And then, Pelosi stopped trading. Well, until her $NVDA leveraged bet.

One week after Chinese President Xi visits her home state of California, and before Biden announces new US semiconductor focuses, her husband decided to buy two million dollars of deep in-the-money Nvidia calls, the same company she divested from due to conflicts a year earlier.

What’s worse On Dec 11th, before she bought in November, U.S. Commerce Secretary Raimondo said that Nvidia could sell slower AI chips to China to comply with US export controls. And then, on Dec 28th, NVDA launched a modified version of an advanced chip precisely to get around US restrictions.

Nvidia now has released new US chips, and has hit all time highs. Of course, none of this is insider trading, but it does seem unusual, especially given scrutiny of Nvida by the government.

Why does she trade ITM tech calls, you may ask? It allows for one to be bullish with less capital upfront, and the contracts move 1 delta to the stock. We wrote more about it on our research site, which you can find in our bio.

One terrible thing about this trade is that it was done when Congress was in session!!!!!! You can use Unusual Whales to find the exact price she paid for her options and leveraged bets.

If you think that one of the most powerful politicians in the US can, or even should, have leveraged bets over an incredibly important company to US infrastructure, that is okay. But there might be something worthwhile in understanding how members of Congress trade, and the data suggests as such. Pelosi herself has lost a ton on trades, including when she divested from $NVDA last year, and yet despite that she decided to enter into it again.

And so we will keep reporting on Pelosi, and Congress, and the history of unusual trading. Pelosi's portfolio itself is up around 88% over twelve months. If you want to find and follow her portfolio, you can do so on Unusual Whales in our Portfolio tab.

Pelosi has made likely ten million this year alone off her tech portfolio, with a networth close to likely a quarter of billion. No matter what trade or conflict though, I will report on it. If you believe this is an important issue, I ask you share this tweet with your friends, and family.

Congress cannot hide from me, I will continue to report on the data, and I will not stop until Congress is banned from trading.

English

Nicholas Kosinski retweetledi

JUST IN: Tucker Carlson reportedly interviewed Ed Snowden in Russia and will release this next.

LFG! 🔥

English

Nicholas Kosinski retweetledi

Putin's 30 minute account of Russia's history was incredibly interesting, not just because of its current political relevance, but especially because it directly highlights the fact that not a single Western leader today could give such a detailed historical account of their own nation the way Putin did.

We in the West no longer have any idea who we are. We have no idea of our own history. Why would we? It's been actively suppressed and rejected. In fact, the only thing our current political ''leadership'' prides itself on, is the rejection of our ''backwards history''. When asked what The West is about, most people will repeat some type of cliché narrative that we've evolved past our nationalistic barbarism into enlightened ''liberal democratic societies''.

It's ironic because as the Putin interview confirmed once again on multiple accounts, ''liberal democracy'' in the West is an illusion. With the current President of the United States being undeniably senile, it couldn't possibly be more in our face. Our government leaders -let alone our parliamentary representatives - aren't actually the ones pulling the strings, but that obvious fact isn't causing the outrage you'd expect. Most people simply play along, even though they know the emperor has no clothes on. For some it might be because they don't know where to start or there's a level of cognitive dissonance and they aren't willing to face the truth, but there are many who are so brainwashed that they actually don't realize they're pawns in a globalist play.

In the latter case the brainwashing has been so successful that anybody who tries to tell them they're being lied to is automatically labelled a conspiracy theorist. It's almost like an immune response: The threat is immediately and automatically located and neutralized. These pawns are the most useful. As Goethe said: The best slave is one who thinks he's free.

To get back to the Russia-Ukraine war: You can dislike Putin all you want, but there is no denying that he is in it for his own people. He's in it for Russia and he has a clear idea of what Russia is and what it stands for. And the real question is, who are the ones really perpertuating this war if the CIA was behind the Ukrainian regime change in 2014 and a peace deal was reached in 2022, but rejected at the last minute because of Boris Johnson's interference? Is Russia really the expansionist aggressor its been made out to be, or has the bear just been poked too often?

One thing is for sure: this was a historical interview, which will be talked about for many many years to come and will hopefully contribute to the de-escalation of this conflict. Thank you, @TuckerCarlson.

English