nilay dalal

402 posts

@SayNoToTrading They need to pacify the dividend value investors, sadly

English

$NVDA dividend increase from 1 penny to 25 is unwanted.

Do buybacks instead please.

English

@SayNoToTrading You will have to unload those $180 cost lots if you are buying here at $161 ans hopefully lower. This is another solid name that will resume upwards by end of year in my opinion

English

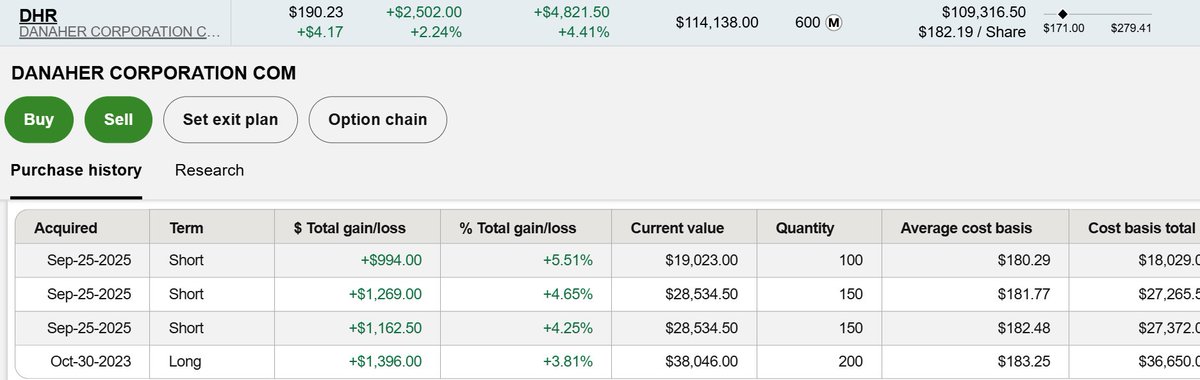

5 days ago was buying Danaher $DHR pretty heavy, as you can see from that post. Today I unloaded all the highest cost lots once in green and these 600 shares are what I'm left with.

Tax loss selling season can be a great time to cycle through shares to lower cost basis on existing shares, plus make a little money in the process.

Say No To Trading@SayNoToTrading

@SeonghyonI No time to post all my buys but yes, $DHR among today for sure:

English

Messed up big time with my $SPGI buy.

Was trying for $344.44 average cost.

English

@SayNoToTrading You can cut and paste your same message and replace wcn with pgr.

English

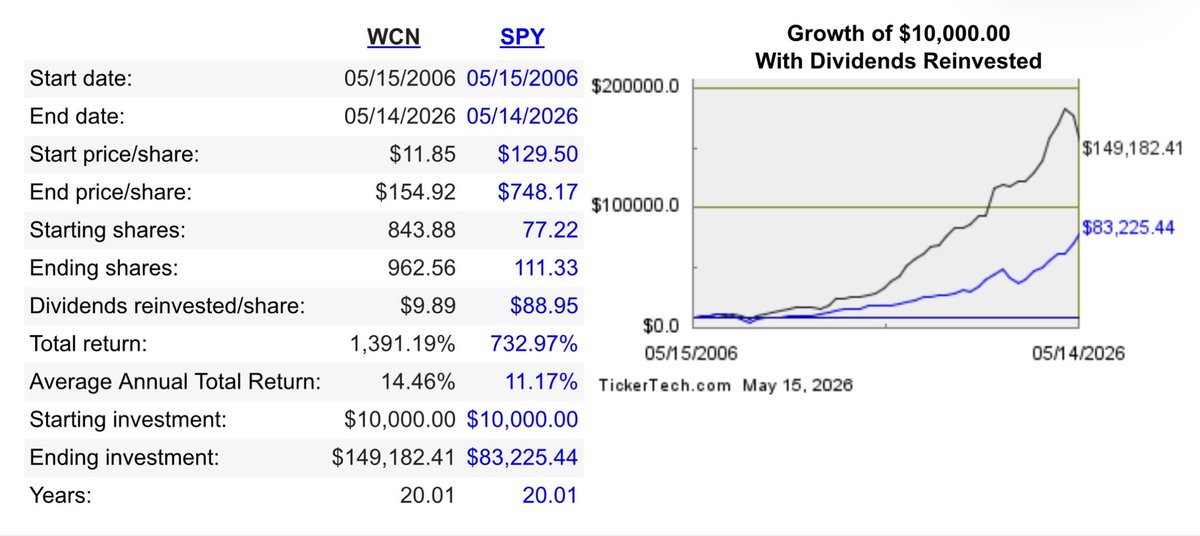

Don’t know when it will be, but a time will come when everyone wishes they bought Waste Connections $WCN rather than chase every chip stock.

Beats the S&P and is the ultimate safety stock when times go bad, but today everyone acts like it’s garbage.

English

A sober valuation analysis on $ACN 🧘🏽♂️

•NTM P/E Ratio: 23.04x

•10-Year Mean: 24.03x

•NTM FCF Yield: 5.78%

•10-Year Mean: 5.18%

As you can see, $ACN appears to be trading slightly below fair value

Going forward, investors can expect to receive ~4% MORE in earnings per share & ~11% MORE in FCF per share🧠***

Before we get into valuation, let’s take a look at why $ACN is a quality business

BALANCE SHEET✅

•Cash & Equivalents: $5.12B

•Long-Term Debt: $71.64M

$ACN has an excellent balance sheet, an AA- S&P Credit Rating & 174x FFO Interest Coverage Ratio

RETURN ON CAPITAL✅

•2019: 42.1%

•2020: 30.8%

•2021: 32.0%

•2022: 38.2%

•2023: 33.8%

•LTM: 32.3%

RETURN ON EQUITY✅

•2019: 37.9%

•2020: 32.1%

•2021: 31.9%

•2022: 32.6%

•2023: 28.5%

•LTM: 27.4%

$ACN has great return metrics, highlighting the financial efficiency of the business

REVENUES✅

•2013: $28.56B

•2023: $64.11B

•CAGR: 8.42%

FREE CASH FLOW✅

•2013: $2.93B

•2023: $8.99B

•CAGR: 11.86%

NORMALIZED EPS✅

•2013: $4.21

•2023: $11.67

•CAGR: 10.73%

SHARE BUYBACKS✅

•2013 Shares Outstanding: 713.34M

•LTM Shares Outstanding: 637.95M

By reducing its shares outstanding ~10.5%, $ACN increased its EPS by ~11.7% (assuming 0 growth)

PAID DIVIDENDS✅

•2013: $1.62

•2023: $4.65

•CAGR: 11.12%

MARGINS✅

•LTM Gross Margins: 32.6%

•LTM Operating Margins: 15.8%

•LTM Net Income Margins: 10.9%

***NOW TO VALUATION 🧠

As stated above, investors can expect to receive ~4% MORE in EPS & ~11% MORE FCF per share

Using Benjamin Graham’s 2G rule of thumb, $ACN has to grow earnings at a 11.52% CAGR over the next several years to justify its valuation

Today, analysts anticipate 2024 - 2026 EPS growth over the next few years to be less than the (11.52%) required growth rate:

2024E: $12.15 (4.1% YoY) *FY August

2025E: $13.19 (8.6% YoY)

2026E: $14.80 (12.2% YoY)

$ACN has an excellent track record of meeting analyst estimates ~2 years out, so let’s assume $ACN ends 2026 with $14.80 in EPS & see its CAGR potential assuming different multiples

25x P/E: $370.00💵 … ~14.2% CAGR

24x P/E: $355.20💵 … ~12.2% CAGR

23x P/E: $340.40💵 … ~10.2% CAGR

22x P/E: $325.26💵 … ~8.0% CAGR

21x P/E: $310.80💵 … ~5.9% CAGR

As you can see, we’d have to assume >23x earnings for $ACN to have double digit CAGR potential (~10-year average multiple, yet arguably a bit rich given its growth rate)

Today at $284💵 it appears that $ACN valuation is being re-rated due to AI-related competitive pressures & it’s growth slowdown, among other things

To ensure some margin of safety, I’d reconsider $ACN closer to $258💵 or at ~21.00x forward estimates (~9% below today’s price) where I can possibly expect near double digit return potential assuming a 21x end multiple in 2026

#stocks #investing

___

𝐃𝐈𝐒𝐂𝐋𝐎𝐒𝐔𝐑𝐄‼️: 𝐓𝐡𝐢𝐬 𝐢𝐬 𝐍𝐎𝐓 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐀𝐝𝐯𝐢𝐜𝐞. 𝐁𝐚𝐛𝐲𝐥𝐨𝐧 𝐂𝐚𝐩𝐢𝐭𝐚𝐥® 𝐚𝐧𝐝 𝐢𝐭𝐬 𝐫𝐞𝐩𝐫𝐞𝐬𝐞𝐧𝐭𝐚𝐭𝐢𝐯𝐞𝐬 𝐦𝐚𝐲 𝐡𝐚𝐯𝐞 𝐩𝐨𝐬𝐢𝐭𝐢𝐨𝐧𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐬𝐞𝐜𝐮𝐫𝐢𝐭𝐢𝐞𝐬 𝐝𝐢𝐬𝐜𝐮𝐬𝐬𝐞𝐝 𝐢𝐧 𝐭𝐡𝐢𝐬 𝐭𝐰𝐞𝐞𝐭.

𝐓𝐡𝐞 𝐢𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐜𝐨𝐧𝐭𝐚𝐢𝐧𝐞𝐝 𝐢𝐧 𝐭𝐡𝐢𝐬 𝐭𝐰𝐞𝐞𝐭 𝐢𝐬 𝐢𝐧𝐭𝐞𝐧𝐝𝐞𝐝 𝐟𝐨𝐫 𝐢𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐩𝐮𝐫𝐩𝐨𝐬𝐞𝐬 𝐨𝐧𝐥𝐲 𝐚𝐧𝐝 𝐬𝐡𝐨𝐮𝐥𝐝 𝐧𝐨𝐭 𝐛𝐞 𝐜𝐨𝐧𝐬𝐭𝐫𝐮𝐞𝐝 𝐚𝐬 𝐢𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐚𝐝𝐯𝐢𝐜𝐞 𝐭𝐨 𝐦𝐞𝐞𝐭 𝐭𝐡𝐞 𝐬𝐩𝐞𝐜𝐢𝐟𝐢𝐜 𝐧𝐞𝐞𝐝𝐬 𝐨𝐟 𝐚𝐧𝐲 𝐢𝐧𝐝𝐢𝐯𝐢𝐝𝐮𝐚𝐥 𝐨𝐫 𝐬𝐢𝐭𝐮𝐚𝐭𝐢𝐨𝐧. 𝐏𝐚𝐬𝐭 𝐩𝐞𝐫𝐟𝐨𝐫𝐦𝐚𝐧𝐜𝐞 𝐢𝐬 𝐧𝐨 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞 𝐨𝐟 𝐟𝐮𝐭𝐮𝐫𝐞 𝐫𝐞𝐬𝐮𝐥𝐭𝐬.

𝐈𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐜𝐨𝐧𝐭𝐚𝐢𝐧𝐞𝐝 𝐢𝐧 𝐭𝐡𝐢𝐬 𝐭𝐰𝐞𝐞𝐭 𝐡𝐚𝐬 𝐛𝐞𝐞𝐧 𝐨𝐛𝐭𝐚𝐢𝐧𝐞𝐝 𝐟𝐫𝐨𝐦 𝐬𝐨𝐮𝐫𝐜𝐞𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞𝐝 𝐭𝐨 𝐛𝐞 𝐫𝐞𝐥𝐢𝐚𝐛𝐥𝐞, 𝐛𝐮𝐭 𝐢𝐬 𝐧𝐨𝐭 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞𝐝 𝐚𝐬 𝐭𝐨 𝐜𝐨𝐦𝐩𝐥𝐞𝐭𝐞𝐧𝐞𝐬𝐬 𝐨𝐫 𝐚𝐜𝐜𝐮𝐫𝐚𝐜𝐲.

English

@TheStockBro $JNJ the time for me to buy more was a year ago, which I did.

$DHR I understand the organic growth concerns but I feel the harshest criticisms of that are failing to respect the Covid boom-bust, which was almost guaranteed to happen.

English

Are you underweight semis?

As of Friday, they are 16.1% weight in the S&P.

A lot of people keep telling me they are chasing because they are underweight $NVDA, $MU, $AMD, $INTC, $AMAT, and on and on.

Know that $SMH is now over 5x its 2022 bottom.

You don't get alpha chasing.

You get alpha waiting for the next good opportunity to average up.

I'm underweight chips too and am not the least bit concerned.

I was super underweight and brought it up big in 2022.

Then did another huge increase in April 2025.

That's how you do it - for sectors you're underweight, you wait until they go on sale, then you increase your weight with the highest quality stocks in them suitable for buying and holding (not trading).

Over the cycles of each sector, it works.

Right now you should be focusing on healthcare and others no one wants, before they become the next race.

You won't win a marathon if you start your 1st mile when others are on their 20th. That's the equivalence of paying any price for semis here.

Say No To Trading@SayNoToTrading

The scariest thing about the surge in semis is that people have totally lost touch with what's actually investable. It's already the most cyclical of cyclical industries, so even the highest quality, with decades of proven endurance, will have ugly boom-busts in their charts. Far uglier than most industries. The difference though with say, $AMAT, $LRCX, $KLAC, $MPWR, $ASML is that even with the boom-busts, the charts are up and to the right over the cycles. Same cannot really be said about most of the chip stocks you see X talking about lately, for those names which have been around long term. For many (most?) you would have lagged the S&P owning them last 10 to 25+ years. Take $AEHR as example. Super small-cap. Compare their long term chart to $TER. Both very boom-bust but one much worse than other, which is why - if you're going to buy Aehr Test - you need to get it super cheap. Its long term CAGR only calculates out favorably at present because of the insane vertical chart. And no, their full-wafer + high-power burn-in is not enough of a selling point. Would rather stick with Teradyne and Advantest as proven buy and hold names, because when these all go down, they should go down less. Even at last April's tariff lows, I preferred TER and broader peers for testing and metrology like KLAC, $ONTO, and Tokyo Electron. Onto was about as low as I would go in terms of quality and small size. It's also not that I'm against small cap. However, $CAMT and $NVMI higher quality, which I did buy. Though I guess their market caps are more mid-cap now. To be clear it's not that I dislike $AEHR but rather, the risk reward of buying here. You need to be thinking of downside risks, first. Not potential upside. I prefer not to own stocks where, the largest catalyst for them, is X subs pumping them hard. If my stocks happen to have that happen later, fine. Though, I want nothing to do with initiating a position during that chase. With the exception of some analog and a few others, pretty much all chips are up hundreds of percent in 12 months. First screenshot is chips stock sorted by lowest market value, first. Note that lowest $IONQ, $INFQ, $XNDU, $P all from past few weeks so lower percentages. Some also show lower percent gains due to recent adds, averaging them up. Second screenshot is opposite, from highest to lowest market value, with obvious emphasis towards quality. Fab 5 are my favorite but also some $NVDA, etc. $SNPS and $CDNS are about the only high quality still reasonably priced, because of their software categorization. As you know I added 400 $NVDA at 160s a few weeks ago, but would not buy now. That doesn't mean it's not going to $240 or $260. I'm not thinking of that. I'm thinking, what are odds it goes to $180? The other ~1/3rd of stocks in the middle are not shown, but weightings in-between. Everything way too green. Also I have some international chip stocks like $BESVF, $TOELF, and $LSRCF which I couldn't move to Robinhood but they are up hundreds of percent in just one year, too. I really like Tokyo Electron. Plus have one private company. I am intentionally writing this post on a big red day for this sector because on green day, no one wants to hear the truth. The time to buy chip stocks is when it seems like the cycle is over, or may be approaching such point earlier than expected. Not when it seems like it has a long runway ahead and there's nothing that can stop it. You've been warned.

English

A DISTURBANCE IN THE FORCE?

Interestingly the indicator flipped to ‘Risk Off’ this morning.

The avg regime duration is 5 days.

So, some consolidation is likely in order, and the signal can flip to Risk On if dip buying turns profitable.

Also, we saw some weakness in earnings results today and semis that reported stopped popping see $ARM for example.

So, there is a disturbace in the force.

Also, note (2) that the spread between high vol and low vol names is very wide.

The (3) funding side for owning semis - the capex payers like $MSFT - rallied today.

Let’s see how this indicator does. It was correctly bearish in the SoH conflict, and flipped bullish in early April.

I do think there are so many bargains out there from the liquidity moving into semis, that fishing in other pastures makes sense.

Remember (4) The $NVDA meltup in May thru July which is my comp for Semis current euphoria.

Study that.

and (5) some names in crypto like Z cash appear extended in the short run.

It’s still a bull market, but rotations looking likely here.

GIF

Ram Ahluwalia CFA, Lumida@ramahluwalia

BUY THE DIP? We added the ‘Should You Buy the Dip?’ regime indicator on the Lumida Invest app. It successfully navigated the Feb / March correction and turned risk on in early April. That is its first Forward Test. The indicator is accessible by clicking thr new Market Color feature. Then scroll down. All you really need to do is see if it says Risk On or Risk Off to keep it simple. The system has been on Risk On since early April. All of the data is point in time, as reported. I use it as a tool. I have also attached the Market Color ‘Morning Brief’ at the top… This morning it said ‘Markets Are Unambiguously Risk On’ It’s a great way to understand what is driving markets.

English

@SayNoToTrading @Gabsterisim @DvdndDiplomats I assume you are averaging down to get this $153 or lower?

English

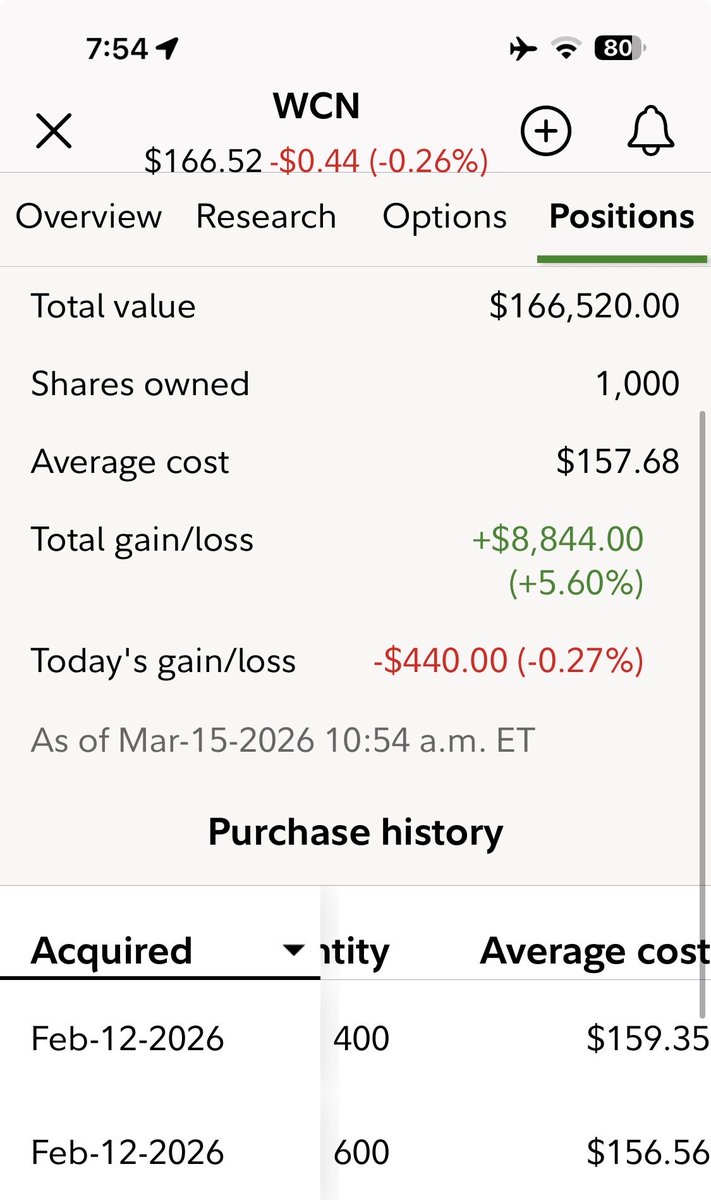

Haha search my feed for $WCN history, as it’s very similar to $FICO.

Many, many dozens of buys and sells on both stocks each year, for at least the past 1-2 years.

Never lost money on single transaction.

Yet on both, the money I make on each transaction is peanuts.

However, eventually they will rebound and I’ll have the lowest cost possible as permanent holds. Or at least, that’s the hope/delusion!

English

The hottest dividend duo right now:

Waste Management & Microsoft

$WM and $MSFT are two favorites of X right now 🔥

English

@SayNoToTrading Solid name. Competent leadership. Set it and forget it

English

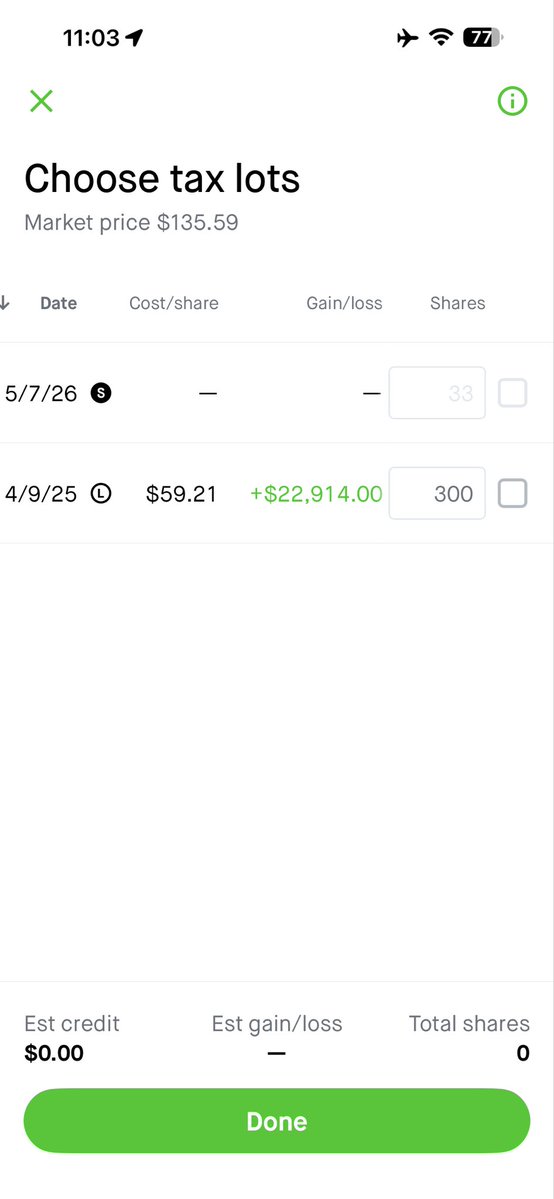

Similar to $ANET earnings dip, which I already made work (see that post’s replies) I decided I should not neglect the next A ticker after it, $APH.

So I just added 33, bringing my average to 333 shares at 66.77.

Amphenol was another one of those stocks I bought at exact tariff low of April 9th morning, 20 or so mins before TACO and the biggest 1-day rally in 20 years.

English

@WMangan1190 2.0x peg seems.. fine. I don't find them particularly compelling no. Prob do the 10-12% that earnings gives you and thats it. Why would they re rate to 30x?

English

Lots of these big name fund managers squatted on $MCO and the likes at 45-50x earnings cause of "business quality"

Yea but at that price you essentially are just holding a pile of duration and rates went from 0 to 4.5%

English

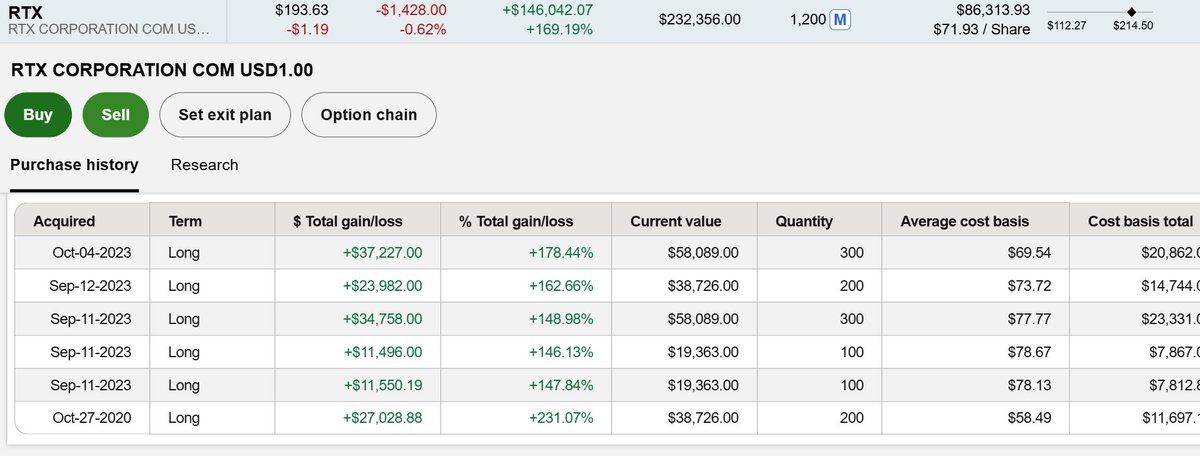

@SayNoToTrading What do you think of RTX here in 170s or a possible dip to 160s? Looking for quality compounders on sale…

English

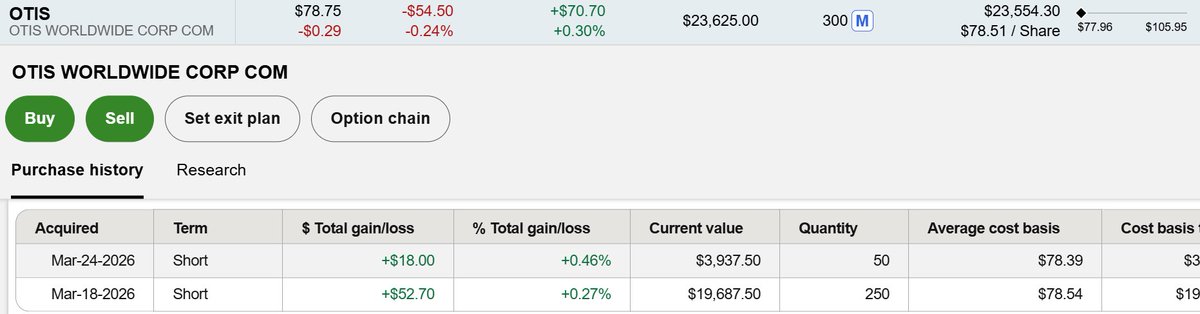

As much as I hate elevators and escalators, I've decided to recreate United Technologies 6 years later, almost to the day.

$RTX + $CARR + $OTIS

Otis (one of the "Big 4" with KONE, Schindler, TK Elevator) together are around 70% of the North American market because:

- Our elevator codes (ASME A17.1) make certification expensive vs. rest of world, so most global players skip it entirely since we are <5% of new installs. Not worth the hassle.

- Moats are proprietary parts + exclusive long-term service contracts, blocking smaller competitors (unlike Europe/Asia where midsize firms force the Big 4 to compete).

This is why elevators are 3x more expensive in the US and Canada, plus have horribly slow speeds, service, and antiquated features vs. elsewhere.

EV/EBIT screenshot from @gurufocus. Forward is 14.5x which places it under 2022 low and places it at all-time low, similar to very lowest point during Covid. Keep in mind the spinoff date for $OTIS and $CARR stocks were within 2 days of Covid low.

I hate elevators because they breed laziness.

If you are blessed enough to be non-paralyzed and have even semi-operable legs, use them. Those in a wheelchair would give anything for such ability that you take for granted.

Aside from pre-purchase inspection, I have never once used the elevator in my current house. Didn't use it in last place either, despite being a 5 floor iceberg house. I don't even care if you live on the 10th floor, use your damn legs, that you are blessed to have, you lazy glutton.

English

@nsdalal Not one where quarterly matters. Just noise.

English

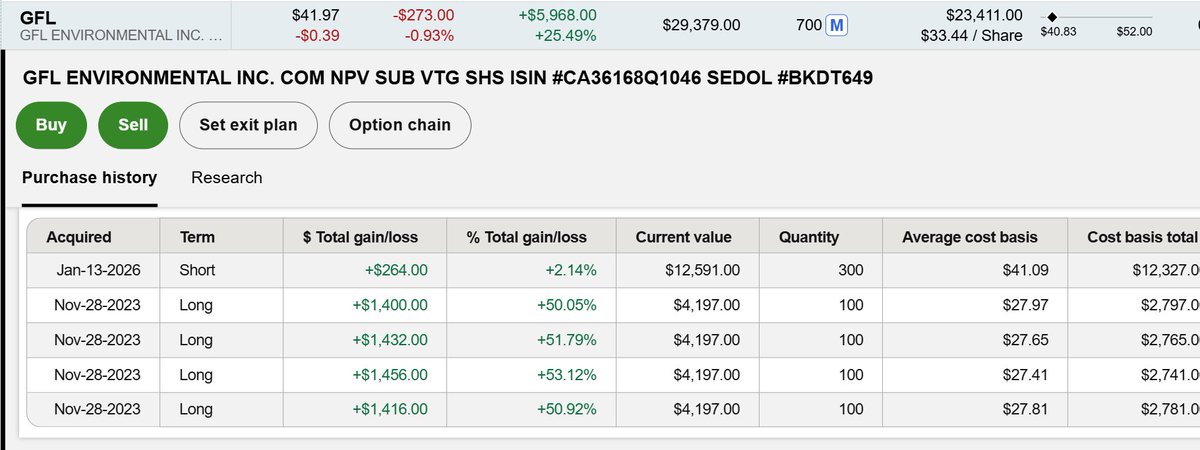

Canadian domiciled garbage stocks $WCN $GFL $SES.TO $SECYF experiencing much greater weakness past few days than US $WM $RSG $CWST $CLH. Casella is the strong outlier.

As mentioned multiple times last year, $GFL never got cheap enough for me to add more.

It finally did.

Remember last year, GFL sold their Environmental Services division (soil remediation, liquid waste, etc.) for $8B CAD to Apollo and BC Partners. $GFL retains a 44% stake.

Keep this in mind when looking at year over year numbers. Charts from Gurufocus.

English

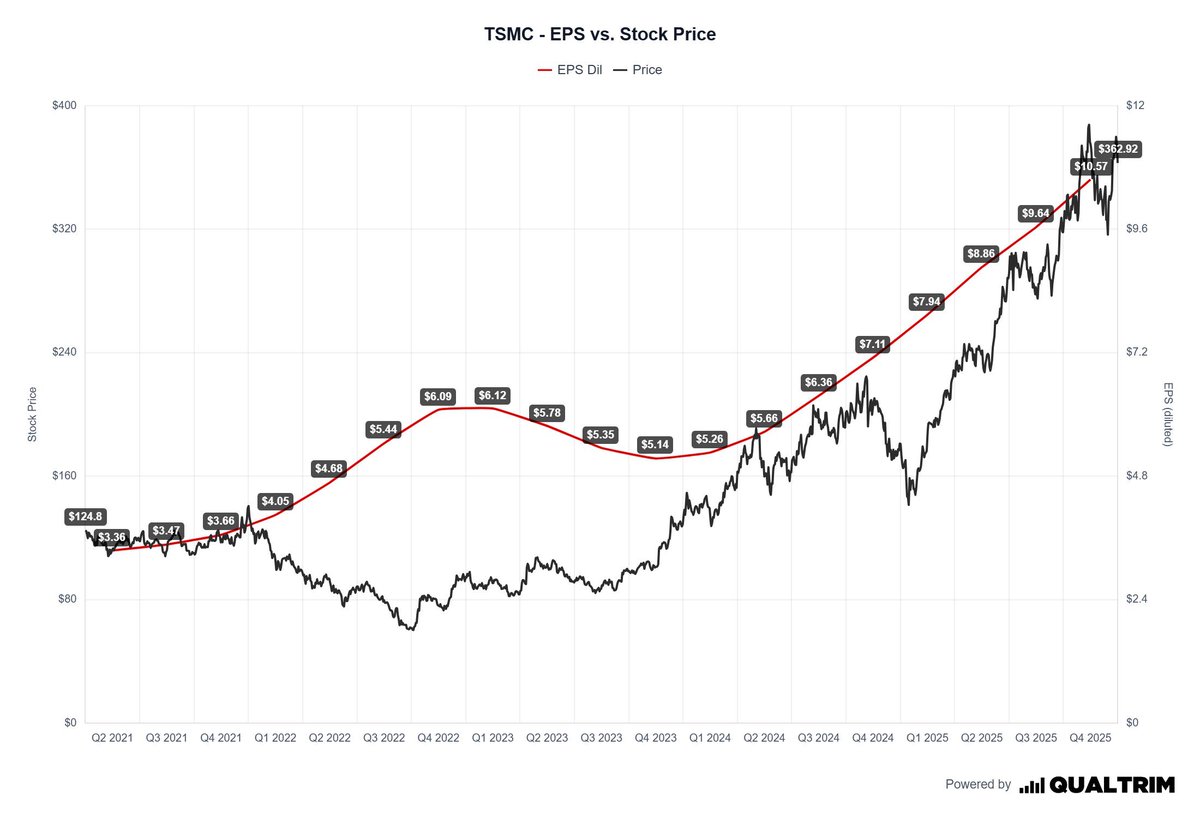

I’m considering a position I’m $TSM eventually.

With $TSM, you gain exposure to a monopoly.

- Supplies $AMD

- Supplies $NVDA

- Supplies $AVGO

- Supplies $AMZN

- Supplies $GOOGL

Without $TSM - this AI ecosystem collapses.

- They’re guiding for +30% YoY.

- Massive insider buying.

- FWD P/E 22x

$TSM

Wealthmatica@wealthmatica

Here are SIX wide-MOAT businesses that I wouldn't mind owning for the next 10-years... 1. $TSM - Taiwan Semiconductor Manufacturer - Forward Guidance: ~32% YoY

English

@anni_sen That’s also a viable approach. I feel comfortable owning more msft as a SWAN name for 7-10 years,

but know it wont 10x like nbis. I treat my nbis as spec as i have 1/10th the dollar value in nbis compared to msft. I rather just own the top 10 names in qqq..

English

@anni_sen Tomorrow AM on a gap down, could see $360-370 which is insane.

English