@mzuhair123 @insane_analyst Thx. In test he mentioned Rigaku via Onto. Have to reread to go over the most crucial.

English

Rob Ptrsn

21 posts

@robptrsn

Find the joy everyday. #GSP #LANDCRUISER100. 30 yr FA-retired. #NFAdvice just my opinions

How can I give back & help you guys more? Maybe if you drop some tickers under the comments to this post, I'll post some research in a few days for the most liked/commented one? Just genuinely want to help!

$AMPX nice report! Gross margins positive for first time. Starting to hit its stride. New fangled batteries... could be seen as a drone play in many ways as well. In Q2, over 90% of our revenue came from the aviation sector, driven by increased and ongoing strength in the drone market. GREAT shareholder letter, a lot of companies could learn its not just data it gives you a good overview d1io3yog0oux5.cloudfront.net/_03f0bc4b3d110… Revenue rose 350.4% to $15.07 million from a year ago; analysts expected $12.78 million. Amprius Technologies Inc's reported EPS for the quarter was a loss of 5 cents. The company reported a quarterly loss of $6.37 million. Amprius Technologies Inc shares had risen by 83.4% this quarter and gained 175.7% so far this year. ********************* In April, we introduced SA102 – the first SiCore cell to reach 450 Wh/kg, an energy density that is 73% higher than the typical 260 Wh/kg of conventional batteries used in electric vehicles and power tools. In Q2 we shipped batteries to 93 customers, 43 of whom are new to the Amprius platform. The remaining 50 are repeat customers Q2 revenue totaled $15.1 million, a 34% increase from the first quarter and up 350% from Q2 2024. This strong growth was primarily driven by a greater than 450% increase in SiCore shipments over Q2 2024. SiCore has a proprietary silicon anode that uses standard lithium-ion processing equipment and is gross margin positive, enabling us to report positive gross margin for the first time. In Q2, over 90% of our revenue came from the aviation sector, driven by increased and ongoing strength in the drone market. We are enjoying increased market adoption and a more favorable policy stance from the U.S. government that we believe creates new opportunities for innovation and deployment. The remainder of our Q2 revenue was primarily derived from the light-electric vehicle sector

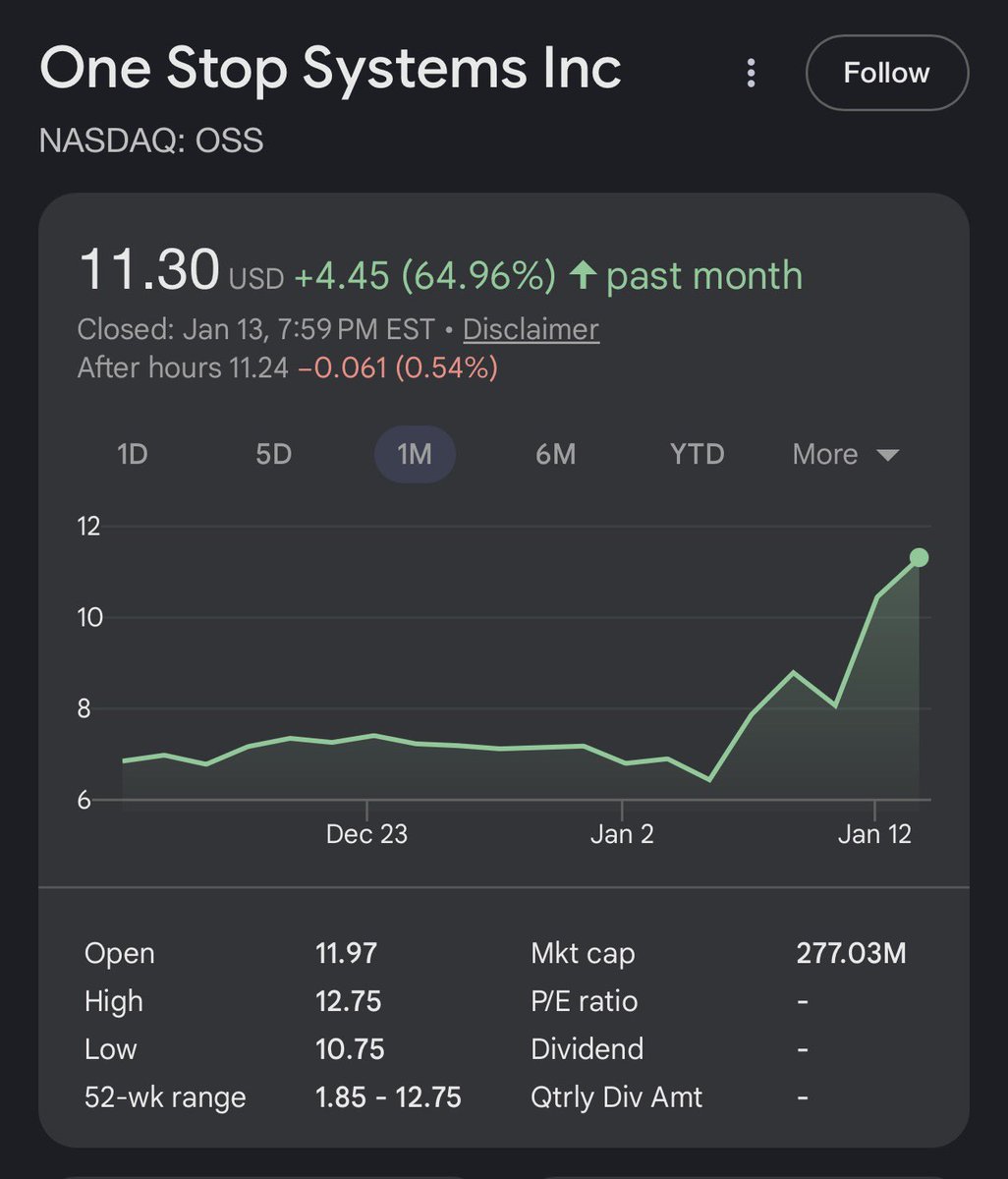

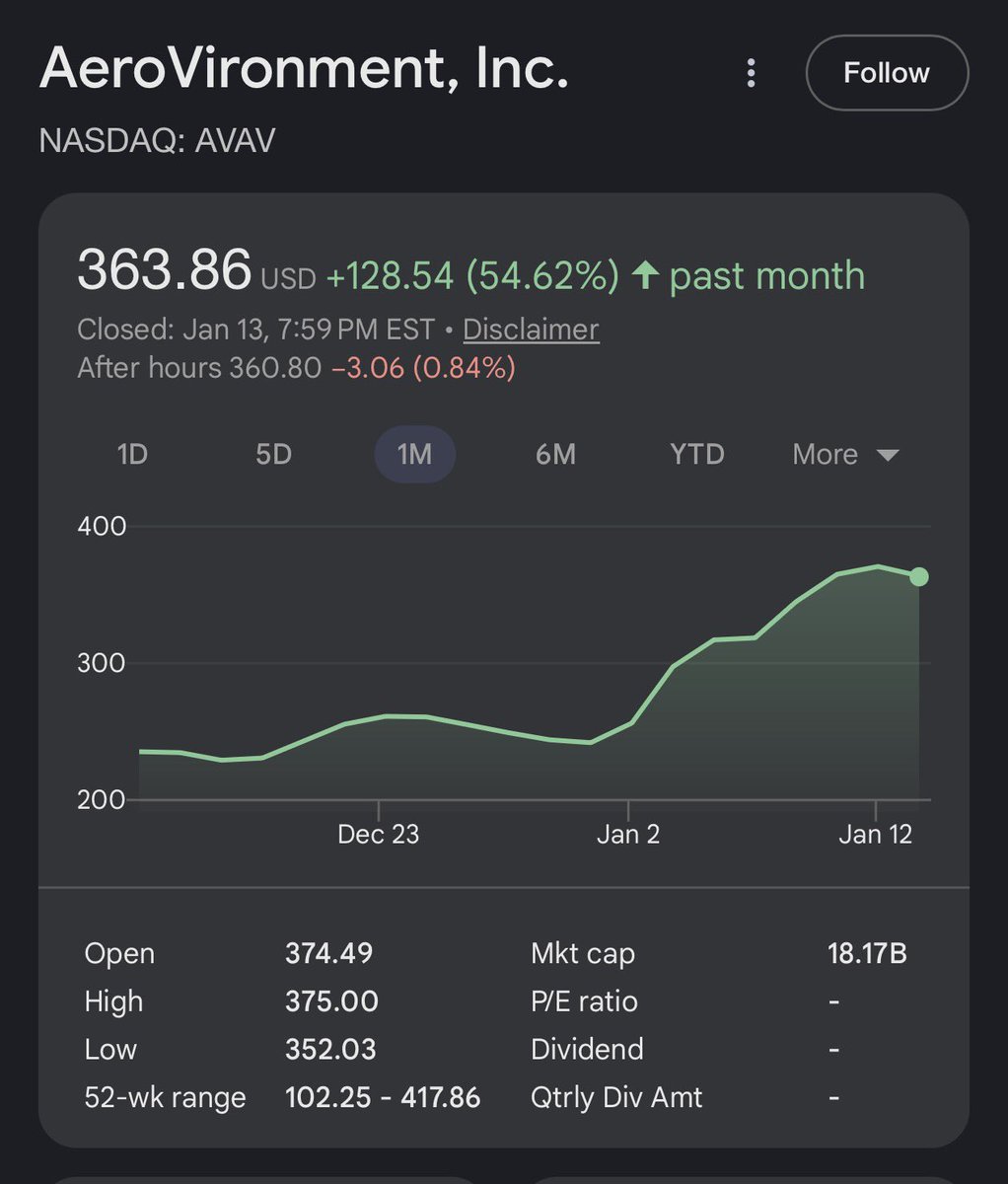

Why are all my picks up like 60% this week $OSS