@SixSigmaCapital Great call! This genius investor level just posted his thesis on $IQE. He states that it has 10x potential but is honest with the risks associated. Would you share your views?

open.substack.com/pub/rmainvestm…

English

Retail Investor Rodri

76 posts

$POET This is the company that pays influencers to pump their stock, no? Poetic

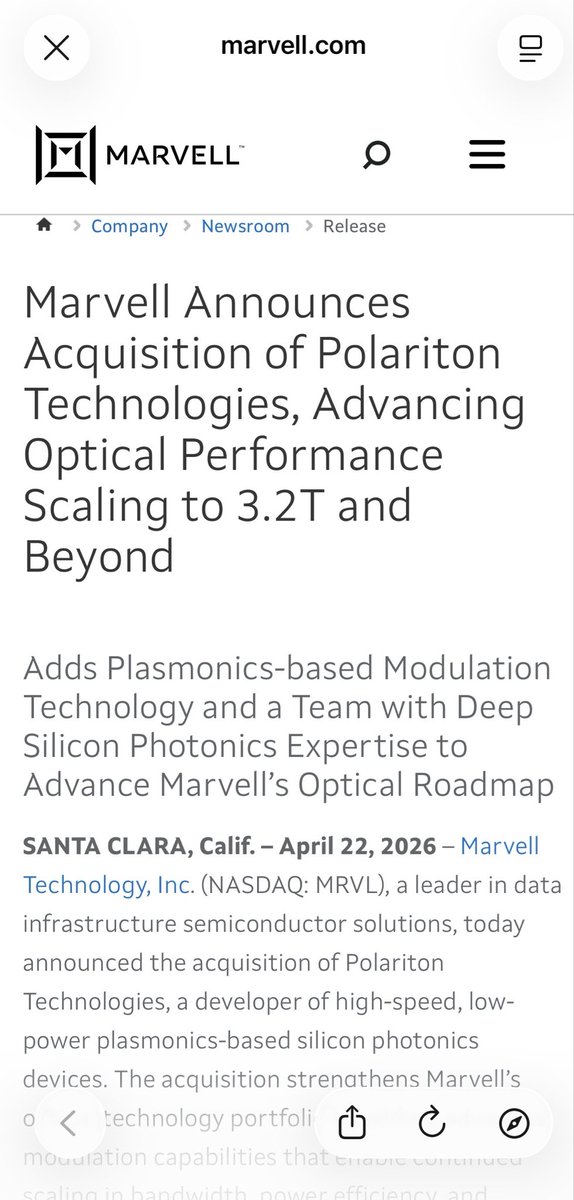

Why did $MRVL really walk away from $POET? Many investors believe today’s nearly 50% crash was triggered solely by a slip-up during a CFO interview. Let’s be realistic: in the semiconductor industry, you don't terminate Tier-1 partnerships over "chatter" if the product is indispensable. The NDA breach was merely a legal backdoor - a convenient excuse to exit a contract without massive penalties. The real reason lies in the events of the past week. 1⃣The Polariton Acquisition (April 22) Just one day before sending the termination notice to POET, Marvell announced the acquisition of Swiss-based Polariton Technologies. Polariton does not do what POET does, but it makes POET's role in Marvell’s stack redundant. ➡️ $POET (Optical Interposer): A packaging platform. It allows for the integration of various optical components (lasers, modulators) onto a single chip at scale. ➡️ Polariton (Plasmonics): The creators of the world’s fastest plasmonic modulators. These are 10x smaller and significantly faster than traditional silicon photonics. ⬇️The takeaway: Marvell no longer needs POET’s "motherboard" because they just bought the "engine." By acquiring Polariton, Marvell can now integrate optics directly into their own DSPs (Digital Signal Processors), bypassing POET’s architecture entirely. This is Vertical Integration at its finest - the giant prefers owning the IP over licensing it from a micro-cap player. 2⃣ The Governance Crisis As investors, we must call out the management's communication timeline: ➡️The termination notice was received on Thursday (April 23). ➡️The company remained silent throughout Friday (April 24), allowing the stock to pump 29% on false speculation. The news was only disclosed on Monday (April 27) before the bell. Failing to report a material event for four days is unacceptable and exposes the company to significant regulatory risk. This destroys trust far more than the loss of a single contract. 3⃣Validation vs. PR Spin Today’s mention of a new $5M order from another customer feels like desperate "damage control." Compared to the projected scale of the Marvell/Celestial AI partnership, $5 million is a drop in the bucket. It isn't market validation; it’s a PR distraction from the fire in the boardroom. ⬇️The Outlook: POET’s technology may still be brilliant, but the company has lost its primary leverage. Other Tier-1 players now know POET is backed into a corner, which drastically weakens their negotiating power. I am not making a "hot" decision today, but the investment thesis based on a "partnership with a giant" has officially evaporated. I will watch tomorrow’s session to gauge the level of capitulation, but my confidence in management is currently near zero.

Over the past few weeks, I've been taking a closer look at the company $POET. Almost no one on X is talking about the Canadian company. After years of research and development and restructuring, $POET is now close to entering production and could therefore be very interesting. A thread 🧵👇

That's interesting. $LWLG's Perkiomen material was featured in $NOK Nokia's ECOC 2023 paper. Upon examining the structure presented in the paper, it bears a resemblance to a plasmonic slot-based polariton modulator (acquired by $MRVL). Upon examining the paper, I found that Polaritons are indeed mentioned. Could this be hinting at a connection between $NOK and $MRVL? I also came across a post suggesting a potential link between $NOK and $SIVE. (x.com/PepInvestStock…) Nokia's paper: Q. Hu, R. Borkowski and G. Raybon, "Up to 256 GBd PAM transmission using plasmonic ring resonator modulator," 49th European Conference on Optical Communications (ECOC 2023), Hybrid Conference, Glasgow, UK, 2023, pp. 688-691, doi: 10.1049/icp.2023.2293. Polariton modulataor image was taken from: polariton.ch/resources/tech…

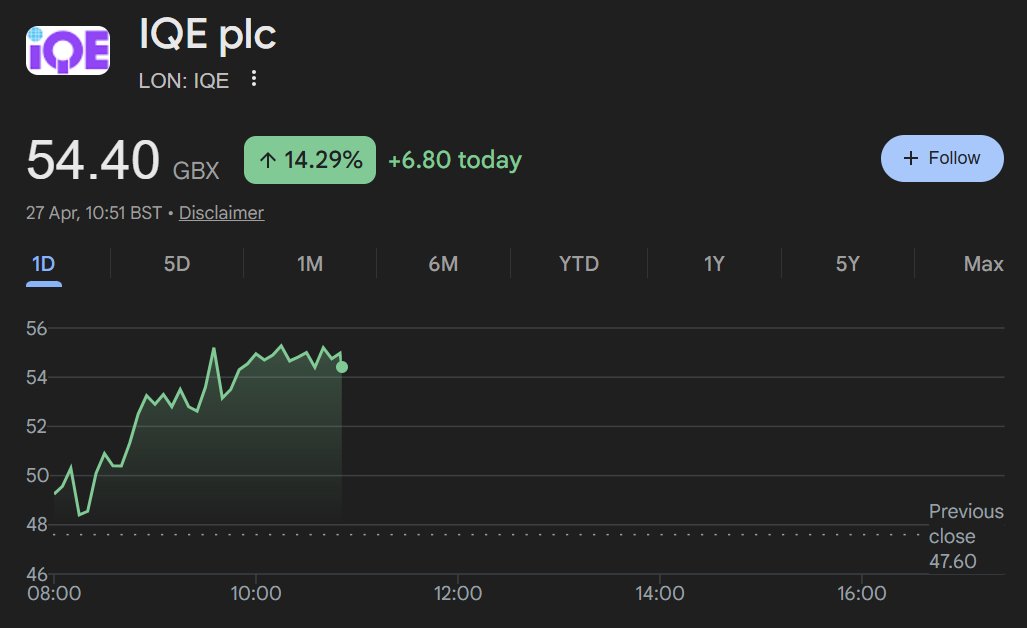

$IQE LandMark Optoelectronics’ latest Q1 results may be one of the clearest signals yet that the AI optical supply chain is hitting a real upstream bottleneck. Q1 after-tax profit reached NT$318M, up roughly 657% YoY, while EPS came in at NT$3.44 — nearly 74% of its full-year 2025 EPS in just one quarter. More importantly, during the recent conference call, the company indicated that Silicon Photonics / CW laser demand remains very strong and that supply capacity is not keeping up with customer demand. This suggests the bottleneck is moving deeper into Layer 1 of the optical supply chain: InP substrates, III-V epitaxy, MOCVD capacity, and laser source production. LandMark also announced 2026 CapEx of around NT$1.315B, roughly KRW 61.6B. A meaningful portion is expected to go toward MOCVD expansion. Based on typical MOCVD pricing, that could imply roughly 6–10 high-end production tools, depending on configuration and supporting infrastructure. To me, this strongly suggests LandMark is already running into real capacity limits. The read-through for $IQE is important. Compared with LandMark, VPEC, and IntelliEPI, $IQE’s current valuation still looks highly attractive, especially considering its exposure to III-V epitaxy, InP/GaAs materials, photonics, and potential Silicon Photonics-related demand. Given the current valuation gap versus other epitaxy names, LandMark’s results make $IQE’s upcoming earnings especially interesting. If demand is already overwhelming capacity at LandMark, then $IQE could potentially become one of the next names to benefit from concentrated near-term demand in the III-V / Silicon Photonics supply chain.

Photonics plays are the shiny new toy right now. This is a great starter list for investors to research. My favorite play out of these, which I will personally be adding to my portfolio tomorrow, is $COHR. Why? 1. $COHR and Tower Semiconductor just demonstrated 400 Gbps per lane data transmission using a silicon modulator in a production-ready process, targeting next-generation 3.2T optical transceivers. That announcement was made March 23rd and the market has not priced it in. 2. Revenue has gone from $1.58B to $1.69B in consecutive quarters, Q3 guidance comes in at $1.78B on May 6th, and Coherent became the first company to mass-produce 1.6T transceivers using 200G per lane technology. That is the exact product every AI data center needs right now. 3. The stock has run from $61 to $336 in under a year and revenue is growing 17% year over year, yet it still trades at a fraction of what Arista and Broadcom command for doing similar work in the same AI infrastructure buildout. The market has not caught up to what this business has become. Not financial advice. Do your own research.

“ $IQE dropped 20%. Shall I sell?! ” No. I added heavily to my position on last week's dip. Summary on why I'm adding to my $IQE position on any dip: 1. Upstream supply chain tailwinds: $IQE's photonics & GaAs segments rely on $AXTI's substrates. $AXTI guided “sequential revenue growth in Q1 2026, driven by growth in InP for the AI infrastructure build-out.” With InP backlog >$60M and plans to 2x capacity in 2026. Since InP substrates are crucial for 1.6T transceivers and CPO: $AXTI's capacity ramp directly removes any chokepoint for $IQE's photonics epi output. And still, $IQE has internal substrate manufacturing capabilities in UK/USA - which produces GaAs, InP, and GaN. 2. Downstream demand sold out: $LITE are $IQE's flagship customer (multi yr VCSEL/EML epi partner): - $LITE has its hyperscaler order book sold out through 2028. - $LITE CEO said “we’re falling further and further behind the demand” - With agreements locking multi yr visibility straight into $IQE's photonics segment. - $NVDA $2B+ investments in $LITE & $COHR signal hyperscalers are locking in capacity yrs ahead, with epi being a huge bottleneck. $LITE's VCSEL & EML epiwafers are exactly what $IQE grows on InP/GaAs. So, locked-in multi-yr volume + sold out book = multi-yr revenue for $IQE's photonics segment. Then you also have $QRVO + $SWKS as $IQE customers for GaAs/GaN epi. It’s less obvious, but $AVGO also source GaAs/GaN epiwafers from $IQE too for its RF business - even while maintaining captive InP epi capabilities for its photonics products. 3. $IQE are an irreplaceable foundry: - patents on epi wafer growth processes (GaAs, InP, GaN) - 35+ years of proprietary tuning for yield/defect control - $IQE Serves everyone ($LITE, $COHR, $AVGO, etc.) without competing downstream - Chinese players face Western export/qualification walls 4. $IQE is different to competitors (and superior): - Substrate specialists (e.g. $AXTI): Sell raw wafers and lack $IQE's IP. - Vertical integrators ( $COHR, $WOLF, Sumitomo): Do some in-house epi but still outsource for flexibility. $IQE is purely neutral foundry - broader access, no channel conflict. - Asian players (e.g. IntelliEPI): Cost-competitive in GaAs but lack Western defence quals + geopolitical risk. $IQE wins on yield, reliability, and secure supply. $IQE's differentiation is pure-play scale + IP + global compliance = “safe” supplier for customers ----- MC forecast: I personally forecast $IQE to >2x until end of 2026 to ~£1.1B MC. Driven by photonics tailwinds materialising + strong execution - $LITE's 2028 sell-out + $AXTI's capacity doubling signal sustained (and accelerating) epi demand. Then any sale of their Taiwan ops would carry a further premium on top (Board are already encouraging bids). Imo, the 20%+ drop last week was just noise r.e. Iran, and nothing to do with fundamentals.

$POET Interesting points from the CFO Interview that has been overshadowed by the Marvell focus: Transcribed in quotes 1. "We’re also in the light source business, which addresses the market for the very advanced companies that are dealing with the issue of converting all of that electrical communication between a GPU and memory device into a light-based communication. And that market is more blue ocean for us. We’ve got fewer competitors in it. We’ve got really unique products in it, and it’s potentially a much larger market than even the high-speed transceiver market is." 2. They are sitting on almost a 1/2 billion in cash - so they don't need to do any offerings but most importantly... "It gives us capacity, which we have to build to demonstrate that we can manufacture tens of thousands of devices per month, up to hundreds of thousands of devices per month. It gives us capability, which is the ability to bring in our own employees, add to our employee base, which we’ve been doing very rapidly in the past quarter. And it gives us credibility. It’s really important for our customers to know that we’re going to be there for the long term. And with a lower amount of cash, they might conclude otherwise. So we’re happy with deploying the cash for both organic growth and for inorganic growth. And in terms of a moat, we already have a moat. It’s our technology itself. So we don’t need acquisitions to do that. What we are interested in doing with our capital for acquisitions or our currency in our stock is to bring in capability and to own components." 3. The market is finally getting it... "what we have to offer in that light source market isn’t fully reflected in our market cap. I mean, we showed what we call the blazar back in OFC, the optical fiber conference in San Francisco back in 2025 – nobody got it. This time around in Los Angeles, we were visited by several laser companies who now understand that they need an approach to a laser development that’s very similar to what ours is. And I’d be getting into some very deep technical details."

Markets are looking at CPUs right now and kinda forgot about memory. But... there's increased capex spend with Sk Hynix, $MU, Samsung around now, with Samsung starting HMB4 production recently. $TSM also signaled record capex across the board. But just like $LPK in glass core substrates... There's a decent amount of structural monopolies over in the HBM camp markets that I'm thinking about in places like Japan. That markets may have forgotten? They would largely benefit from current HBM4 capex cycles. Over in Korea, things like Hanmi Semi (KRX: 042700) have been taking off, up 27.6%+ today, so I'd guess the other companies around the world might play catchup soon.