ResearchPulse@ResearchPulse1

Perspective that (re)moves the needle – a lot

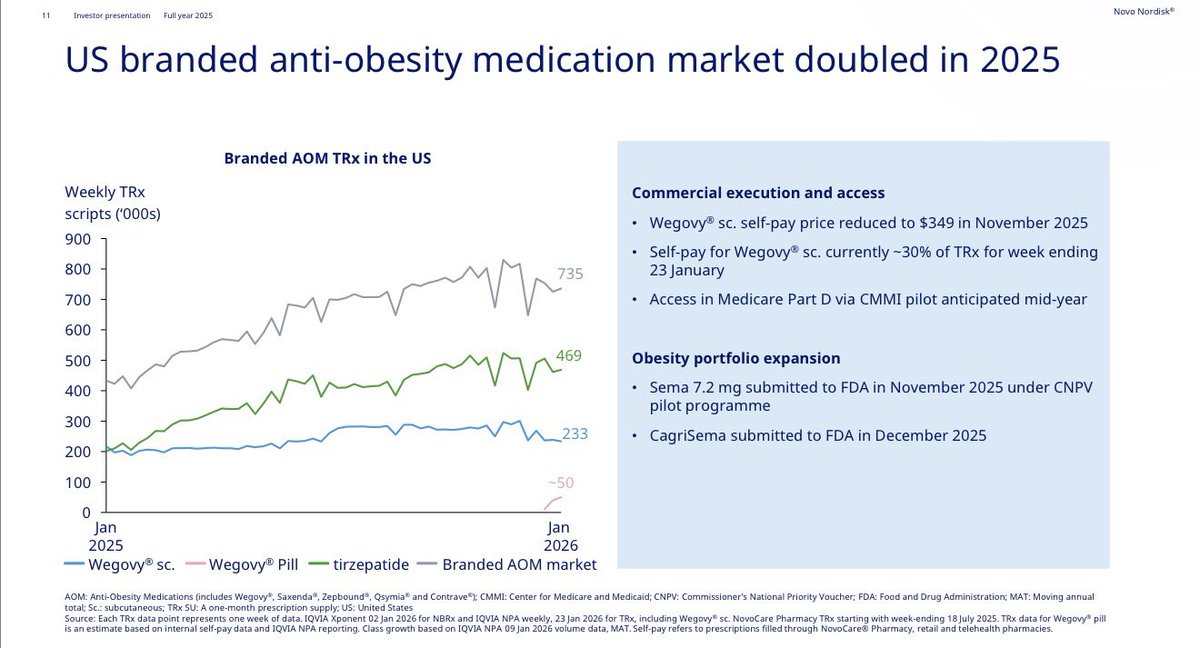

$NVO shocked the investing world yesterday by coming with a very low 2026 guidance. A negative growth at 5-13%. Both in revenue and operating profits. But they actually also came with some wegovy pill data that means the year will end better than that. Like $2.5B upgrades of wegovy pill sales during the year.

We have only seen TRx sales data from 3 weeks. In total 47,580 prescriptions with 26,109 from just week 3. But those numbers do not include sales through NovoCare and telehealth’s.

Yesterday NVO ceo Mike told Bloomberg that in the first 4-week total sales were TRx 170,000. Which means NovoCare and telehealth’s sales are larger than those IQVIA sales data that get published each Friday.

With that new 170,000 sales number for the first 4 weeks, we can fairly precise model how each week looks.

See below.

Green is IQVIA data from week 1-3 and the total sales TRx for the 4 weeks.

Orange is an estimate of IQVIA week 4. (we will get those this coming Friday)

Yellow is calculated with above data.

This means week 4 total were about 68,000. Remember that number

Now look at the two other pictures.

The first picture visualizes to the left how many new starters (NBRx)Zepbound (green) and Wegovy pen (blue) have had each week going back to 2023.

Zepbound has had 1 week with about 70,000 but have throughout 2025 hovered a lot around 50,000-55,000 new starters each week.

Now look too the chart to the right. Here we see the weekly IQVIA TRx for Zepbound with green. As can be seen there was only one direction. Steady up week for week. Here it ends at TRx 474,000. It even hit TRx 523,800 in the first week of December (not shown here)

Now look at the next picture showing diabetes sales in US.

With grey we see Tirzepatide/Mounjaro new starters per week. Throughout 2025 it has hovered around 45,000-50,000. Now see the chart to the right. It shows weekly IQVIA TRx 737,000 for Mounjaro

Wegovy pill recruited about TRx 70,000 in week 4 alone!

This coming Sunday, 125 million Americans will see Super Bowl. NVO has bought 2-6 commercials to air during the breaks. Introducing wegovy pill for about 50-60 million watchers with a BMI above 27. Most of those who have not yet heard about wegovy pill. How many of those will think hmm I can use $149 for trying this "diet". That’s a substantial number. And likely a 7-digit number.

Super Bowl will drive new weekly TRx above 100,000 for a number of weeks. Could we see 150,000 or even 200,000 new starters in 1 week? That seems plausible. But there’s a bottleneck with booking a time with a doctor. That might delay the full impact for 1-2 weeks.

TRx 68,000 for week 4. If we "only" set new starters at 100,000 in week 8 and week 12 (last week of the quarter) then week 12 will be around TRx 250,000. That’s the equivalent of 1 million Americans using wegovy pill.

1 million wegovy pill average for a year is about $2.4B. And NVO might reach a level in that neighborhood in Q1 alone. This is before including impact from MediCare that will see only $50 as co-pay per month.

Also, there’s only about 8% (about 5,500 in week 4) of current wegovy pill users through insurance. There’s weekly TRx 300,000 zepbound users and 160,000 wegovy pen users through insurance.

It should be fair to assume crossing weekly TRx 100,000 through insurance during the year

But wait a minute. If wegovy pill sales go through the roof like this, then why did NVO come with a horrible outlook for 2026?

For several reasons.

· First of all, there WILL be a big impact with the lower prices for ozempic and wegovy pen in US, plus some headwinds for loss of patent in some countries.

· But while the first 4 weeks of wegovy pill sales is beyond crazy, then there’s still a lot of unanswered questions.

· How many will drop out of treatment and how fast? Typically, we see a 20-30% dropout during the titration period.

· How many will titrate above 4mg?

o While the two lowest doses cost $149 per month, the two highest cost $299. How many of those that start at $149 can afford $299?

· We have a new CEO and a new chairman. They want on purposes to set the guidance extra conservative to make sure there can come several upgrades during the year.

Symphony data from week 3 shows 83% started at 1.5mg dose, 11% at 4mg dose and 6% at 9mg and 25mg. Only those 6% pay $299. The rest pays $149

If we model that to week 4 data with TRx 68,000, then revenue for that week would be just shy of $11 million. Then there’s a cut to telehealth partners and higher prices for those 8% coming through insurance.

Roughly week 4 runway for the whole year would be about $500 mil. Analysts’ consensus is about $700 mio for the year

According to my estimates NVO can handle above 3 million consumers as of now. Tthat number will cross 10 million during 2027.

Now remember those weekly new starters of “only” TRx 45,000 to 55,000 on Zepbound and Mounjaro. And that brings them to weekly TRx +460,000 and +700,000

I think we will get close to weekly TRx 250,000 by end of Q1 for wegovy pill. And that we also will see north of weekly TRx 500,000 this year. Giving revenue above $3.5B in 2026. And that’s less than half of their capacity this year. So its not even extremely BULL.

This would also mean upgrades to wegovy pill sales during the year above $2.5B. That would lift the revenue forecast by more than 6% and thereby bring the midpoint down to negative growth of 3%.

$LLY $VKTX