English

Steve Crossan

1.1K posts

@stevecrossan

Solving Biochemistry @ Dayhoff Labs. Previously: DeepMind (AlphaFold), Google Maps, Gmail, Search.

Looking for a quantum chemist with experience in reaction mechanism and kinetic modeling for a well-funded project. Please RT. DM me if you’re interested in learning more!

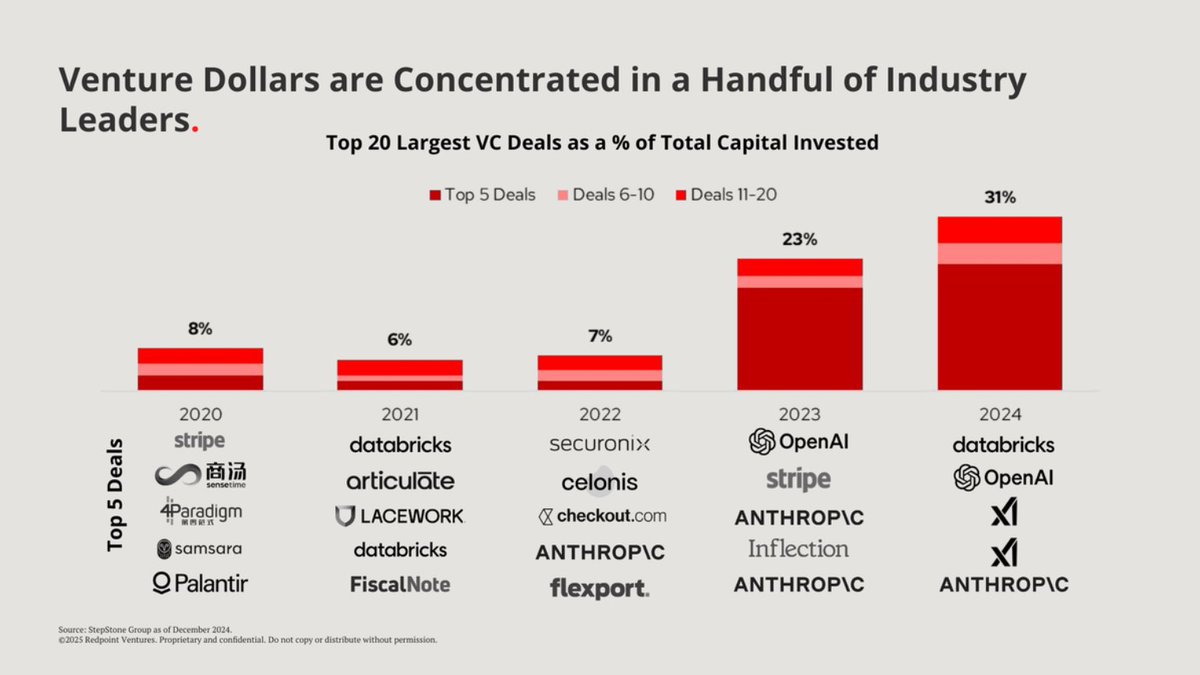

Early stage VCs should (probably, on average) make more investments. Lots of objections, some of them very valid. But the general disdain for "spray and pray" is pretty anti-math. Link to the full argument as laid out by @credistick in following post

We asked @credistick what VCs get wrong about risk management. "If you properly manage risk, you can take more risky bets." "According to Dave McClure, a seed stage fund should have 100 startups, because of the small % that some become unicorns or deca-corns."

@stevecrossan/engineering-for-science-c740dff839ca" target="_blank" rel="nofollow noopener">medium.com/@stevecrossan/…

on Engineering for Science