Sabitlenmiş Tweet

Most traditional debit cards charge 2-3% on every foreign transaction. A handful of crypto cards do 0% FX and convert at mid-market rates. The savings add up faster than you'd think.

Where are you traveling next?

English

Michael | Sweepbase

513 posts

@sweepbaseHQ

Founder of Sweepbase. Indexed 141 crypto cards, audited every fee. DeFi farmer when the APR makes sense. Stablecoins + self-custody guy.

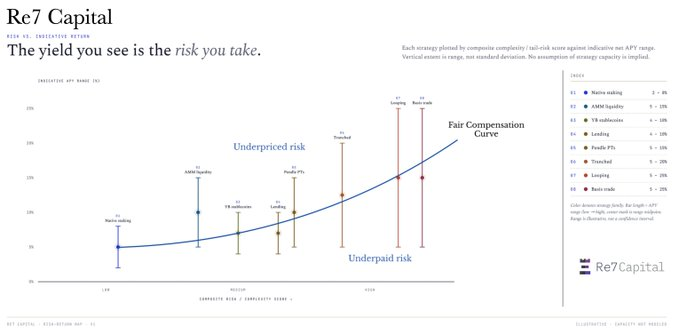

Across DeFi strategies, indicative yield tracks composite complexity remarkably tightly — a fair compensation curve emerges. The further a strategy sits from that curve, the more carefully you should ask whether you're being paid for the risk, or just taking it.