@KevinLMak : I sold the last of my $SPHR, thanks! How are you thinking about $LKNCY at $30?

English

Ted Graham

64 posts

@tedgrahamdenver

@EmporiaEnergy’s Pro Charger avoids electrical panel upgrades and dynamically charges your EV with solar. Ex-futures & options trader.

Reiterate h/t to @deepvaluedude for pitching the trade. I genuinely like this better than $ASTS, although it may be too academic. if ASTS succeeds, SATCO should succeed, and VOD will accrue massive value from that. But there's lots of weird worlds where ASTS succeeds and the market is blind to the read-through to VOD (or it takes years to materialize, and the calls won't pay off) fyi I'm over half the OI on this, but the stock/mcap is plenty liquid, and these options positions aren't distortive given how big the company is.

$EVLV Most of the numbers known ahead of time. - EBITDA margin is very solid at 5%, better than expected. - Guidance is a little soft but it's probably because they're sandbagging. New mgmt team, they don't want to miss guidance on their first sets of numbers. Interested to hear what they have to say on the call. In terms of stock price reaction, EVLV has a pretty small following so it doesn't trade much AH. My expectation is that this will price in with volume/updwards trajectory tomorrow at 9:30AM when the institutional flows come in. Probably more short covering, and probably more long-buying. Similar to what we saw when they pre-released earnings.

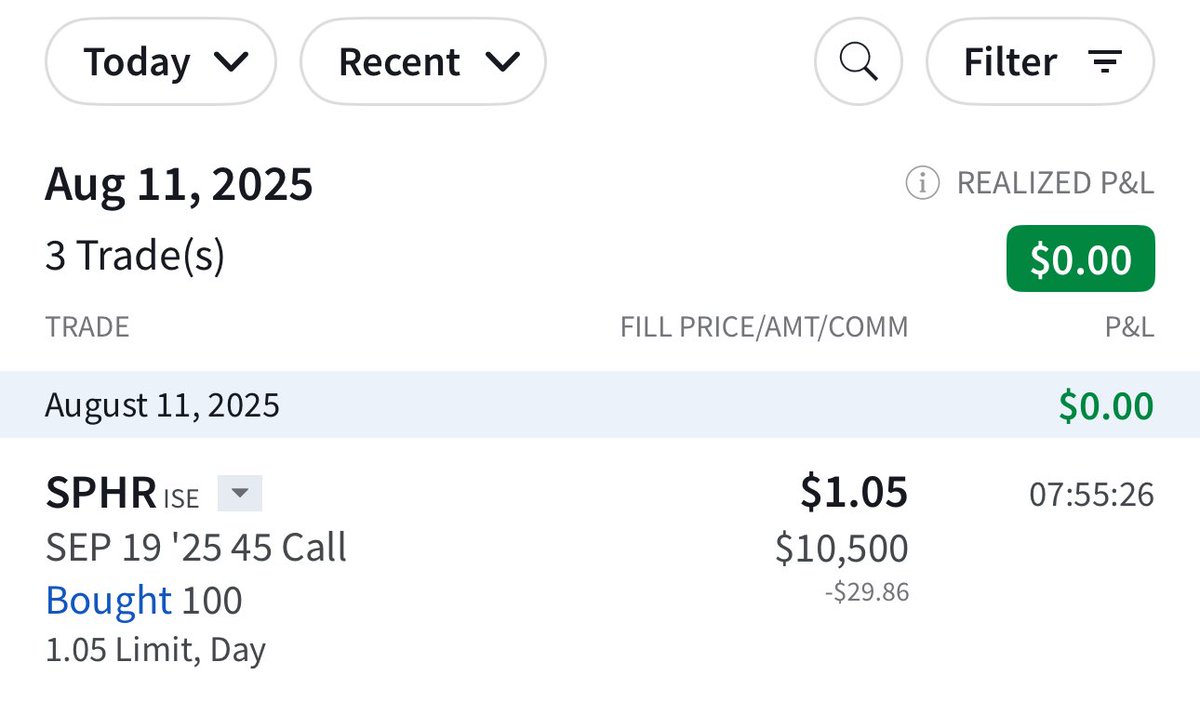

Wild trading in $SPHR this morning. Premarket loved the Q2 results and then it sold off hard at the open.