Block

4.8K posts

Mining investor here.

The take-home is never own a mining ETF. Too many CEO's are scam artists and grift for a living. Just buy quality and sleep well at night.

If the insiders aren't buying, you shouldn't buy it either. Most important insider buy is CFO, second most is CEO.

SilverDegen@SilverDegen

Silver Mining investors won’t like this trend. Maybe your favorite influencer is lying to you or being paid to promote the stock.

English

@GavMcCracken @PraiseKek You can start a company on much less. Incrementally. Based on the phase of your product... But if you feel you need the full capital and bootstrap it then no one knows better than yourself

English

@theBestBlock @PraiseKek Until it hits 25,000x I won't be impressed with myself tbh. I'm just too far from being able to start a company

English

Unfortunately, I don't recognize Gavin anymore. What the hell happened to you? Why this delusional obsession with CAGR competition? Why pretend to know other people's returns? Why dismiss people who were in this sector before you even wore diapers? Why the hubristic ego? Why...

Gavin@GavMcCracken

Another snowflake with a sub 10% CAGR bites the dust.

English

@theBestBlock @PraiseKek It's closer to 3000x now I'm just too lazy to update it lol

English

@KashRamki @litigious_dulce @blackwalletfr If I full ported $NUAI when I bought in September I would've so much richer...

English

@litigious_dulce @blackwalletfr Caution: The Kelly Criterion only works when you have infinite bets. Life doesn’t work that way. The Kelly Criterion only works in theory and is a great way to lose your money on one bad bet.

English

@beavinvests @aleabitoreddit Both will need to make way for the new sheriff in town $NUAI

English

@aleabitoreddit So is $IREN the only company in this market that needs to spend money on data centers?

Is $NBIS just immune from capex?

$NVDA gave $NBIS $2B to be exact.

$2B is chump change if you want to build these projects to the scale the market is demanding.

English

As I said before $IREN is basically dogsht compared to $NBIS.

$NVDA didn’t give $IREN funding yet.

So IREN needs to figure out how to buy enough GPUs to monetize 5GW capacity through their 6B ATM and other means.

It’s an endless dilution machine just because they secured power.

I call $IREN holders 0 IQ because they just buy in it to get diluted without understanding nuances of financing.

Nvidia actually gave $NBIS funds.

While Nvidia got a free no-risk purchase agreement for allowing $IREN to use their logo.

$IREN is basically a marketing company at this point, while the other Neoclouds actually allow equity appreciation.

Serenity@aleabitoreddit

I still am bearish on $IREN. Algorithms/retail probably read $NVDA + $IREN partnership and bought it up. However, if you look at the realtity, it's just looks like brand agreement giving $NVDA risk-free convertible notes. So $IREN can continue selling their $6,000,000,000 ATM into retail investors. It's the equivalent of a startup using AWS and saying they have an Amazon partnership so give them $6B. This wasn't Nvidia directly funding $IREN yet, just a risk free option to. There's a "5 GW deployment" but I'd rather not be the one buying into the dilution to fund it.

English

@PraiseKek @GavMcCracken Honestly if I made 2000x in 7 years I would be worse than Gavin... Which is probably why I don't deserve it 😅

English

@GavMcCracken Avoid the path of the dark side, young buck. Reflect more often. Count to ten. No rush. Don't waste a good game. Cheers.

GIF

English

Block retweetledi

$ASPI I've been in and out since early 2024, always been following their progress. I wanna highlight a couple of X accounts to follow. Search $ASPI on their profiles for a deeper dive.

🔎 @AcctNo994 - Know what you hold.

Blunt conservative investor, very bullish on $ASPI since ~2022. Deep due dilligence on tech, history, science and people. Sees massive undervaluation with strong upside. South African nuclear talent moat (post-sanctions aerodynamic + laser enrichment expertise from Klydon team).

Frontrunner for commercial HALEU (2027 target) thanks to existing facilities and Pelindaba advantages.

Renergen helium/LNG acquisition as major catalyst: Phase 1 cash flow + Phase 2 helium potentially $200M+. Bullish 2026 EBITDA.

Diversified high-margin portfolio: medical isotopes (Yb-176), Si-28, C-14, tungsten, REE recycling.

Superior tech vs. centrifuge peers like $LEU. Praises CEO Paul Mann’s foresight (early TerraPower bet).

Tactical critiques on presentation, but core thesis remains strongly positive.

🔎 @piterloskot82 - Stay up to date!

Highly active advocate, $ASPI is his largest position. Deep dives in to everything ASPI, strong coverage and connecting the dots on what might be going on behind the curtain.

Sees an emerging leader in stable isotope enrichment (medical, quantum, semiconductors, HALEU/LEU+, Li-6/7, Ni-64, Si-28, Yb-176).

Quantum Enrichment tech offers strong scalability. $QLE spin-out will unlock value.

Current EV justified by existing plants alone; rest of portfolio at near-zero.

Rapid scaling (employees ~271), 2026 deliveries (Si-28 in Q2), TerraPower invoicing, strong partnerships.

$300M potential annual EBITDA from core ops. High conviction in management.

🔎 @matt_nealy - SEC forensic

Tracks confidential QLE S-1, board/HQ changes, and Pelindaba access rights as de-risking steps for spin-off and US funding.

Views risk disclosures (e.g. TerraPower concentration) as standard SEC transparency.

Monitors institutional accumulation (BlackRock, Vanguard) and filing timing for stronger prospectus.

Emphasizes management is “doing it right” with regulators.

🔎 @FinanceMajor_23 - The value?

Quantitative macro + supply-chain analyst. $ASPI/QLE as Western platform reducing isotope supply disruption risk (~26% VaR reduction).

Renergen adds near-term cash flow; strong HALEU contender for SMRs/data centers.

Multiple 2026 catalysts: commercial isotope shipments, helium ramp.

Volatility = buying opportunity in nuclear/AI tailwinds.

Overall Convergence: All highlight South African tech edge, HALEU/isotope leadership, Renergen catalyst, and strategic value in a supply-constrained nuclear boom, while noting execution risks. Conviction, research depth, filings, and modeling.

Thanks grok for summarizing, my man.

English

Block retweetledi

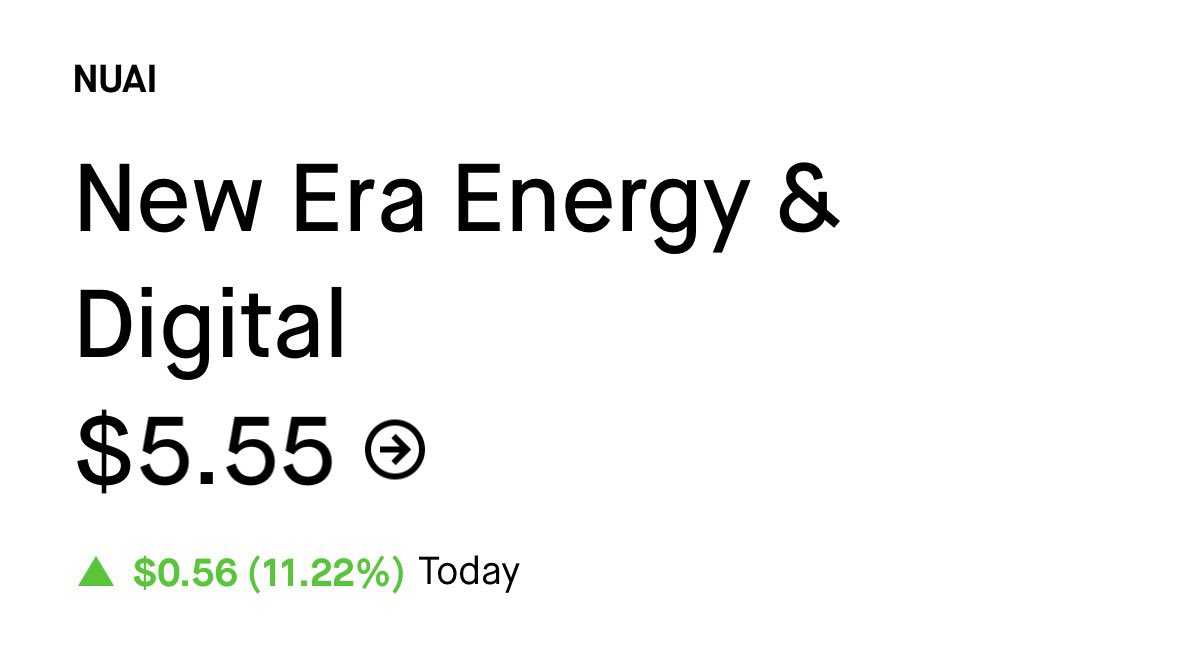

NUAI: An Asymmetric Pre-Deal Position in AI Infrastructure

Summary

Investors comfortable holding $IREN, $WULF, $CIFR, or $APLD before they announced their first hyperscaler deals should be comfortable holding $NUAI today. The structural setup is materially identical with less execution risk. NUAI is operating the validated playbook those names established in 2025, with Stream Data Centers (Apollo-backed at $40B) and Macquarie already on the cap table, four hyperscalers as the only credible counterparties, and a six-month Macquarie clock functioning as a forcing function for lease execution.

Position Overview

Eighteen months ago, AI infrastructure names like IREN, WULF, APLD, and CIFR traded as speculative microcaps. Each re-rated sharply once a hyperscaler signed. Multiples expanded, floats compressed relative to opportunity, and the market repriced the companies from "miner" to "AI infrastructure platform."

NUAI follows the same template. New Era Energy & Digital has 650 MW secured in Ector County, Texas — the flagship "TCDC" campus — and management has confirmed advanced commercial discussions with one of four hyperscalers: Alphabet, Amazon, Meta, or Microsoft. The joint venture was organized by the hyperscaler, who selected Stream Data Centers as development manager and an institutional capital partner (Northland believes Apollo) to provide equity and arrange approximately 80% project-level debt. Stream contributes hyperscaler relationships and operational execution. NUAI contributes site control. The structure was effectively delivered to the company.

Why the IREN/WULF/APLD Comparison Holds

The standard objection to any "early-stage X" pitch is that every microcap claims to be the next something. Four points distinguish NUAI from generic versions of that pitch:

1. Secured land. 650 MW in Ector County is owned outright, not optioned or under LOI. The recent equity raise eliminated the SharonAI overhang and consolidated full ownership of the TCDC site. Power-ready acreage is the binding constraint of the entire AI buildout and the single hardest piece to fabricate.

2. Institutional capital. Macquarie wrote a $290M project-level facility. Apollo acquired Stream Data Centers for $40B in November 2025 and is the implicit equity partner on TCDC. Both are among the most rigorous diligence shops in private capital, and both are staked.

3. Professional execution stack. Stream as developer/operator; RK Mission Critical for modular fabrication and supply chain; Thunderhead Energy for behind-the-meter power; Ramboll / EYP Mission Critical Facilities for engineering. Charles Nelson joined as President/COO in February 2026. Ted Warner — with nearly two decades of capital markets experience and over $7B in HPC-related financing — joined as CFO in March 2026.

4. Binary counterparty universe. Four hyperscalers, all investment grade, all capex-constrained on power, all publicly committed to multi-year buildouts. Whichever one signs represents top-tier credit on a 15-20 year colocation lease.

Behind-the-Meter Has Become the Industry Default

A year ago, the consensus view across the data center industry held that behind-the-meter (BTM) power solutions were unworkable at hyperscaler scale. Critics argued that hyperscalers required utility-grade reliability, regulatory complexity would prove insurmountable, and BTM would remain a niche workaround rather than a primary power strategy. That view was a real overhang on every developer pursuing BTM as a path to capacity.

The consensus has reversed in twelve months. CIFR, APLD, WULF, and CORZ are all now executing BTM-led power strategies, and hyperscalers — facing multi-year interconnection queues and structural grid constraints — have endorsed BTM as a viable route to GW-scale capacity. Thunderhead Energy's role on the NUAI execution stack should be read in this context. NUAI is executing a strategy the industry has at this point publicly validated, with a power partner whose model is de-risked by parallel deployments at peer companies.

This is a meaningful update to the underwriting. The power-delivery question that was an open risk on every pre-deal AI infrastructure name twelve months ago is now the operating assumption across the cohort.

Stream Data Centers as the Execution Catalyst

In November 2025, Apollo paid $40B for Stream — for a particular set of capabilities that map directly onto why a hyperscaler would select TCDC.

Build-to-performance spec, not build-to-suit. Stream pre-aggregates standardized MEP equipment and configures it on the fly to customer specifications. The company quadrupled its development team during COVID and has been procuring long-lead equipment up to a year ahead of demand. Standardization speeds development time materially in a market characterized by acute power constraints and capacity scarcity.

Configurable cooling that future-proofs the asset. Stream's proprietary cooling design supports air cooling and direct-liquid-cooling on the same footprint, scaling from 10-12 kW per rack to 400+ kW per rack. Customers can defer the air-vs-DLC decision until late in the build without extending the timeline, providing meaningful optionality across NVIDIA's roadmap from Blackwell to Rubin and beyond.

Pre-existing hyperscaler relationship. This element has been broadly overlooked. Because Stream has worked with this hyperscaler before, we can safely assume that a significant amount of work product can be leveraged for TCDC. Management's fall 2026 lease execution target is credible because contracts are likely being adapted, not drafted from scratch.

The distinction is between a startup negotiating with a hyperscaler from a blank page and the hyperscaler's preferred developer adapting an existing form to a new site. Execution risk lives in a different category.

Expected Value Framework

In my opinion, the probability of a deal with the current hyperscaler by August 2026 is 90%+. The hyperscaler organized the JV. They selected Stream. They directed the structuring. Engineering and permitting are progressing without observable friction. Negotiations leverage Stream's existing templates and shared counsel. The Macquarie facility requires lease execution within six months, aligning every party's incentives toward closing.

As for the probability of any deal eventually, I would say 99%+. If the current hyperscaler exits — for which there is no observable reason in a market structurally short on power-ready supply — the structural work is already complete. Site control, partner ecosystem, financing template, and engineering package are not counterparty-specific. Another publicly traded data center company recently demonstrated this dynamic: a hyperscaler counterparty exited, a replacement was secured, and the timeline extended by approximately one month.

Stress-tested at a deeply conservative 50% probability of a deal — well below what the structural setup supports:

50% × 4-5x upside ≈ 2.0-2.5x expected return

50% × 50% drawdown ≈ 0.25x expected loss

Net expected value: approximately 1.75-2.25x

At 90% probability, expected value approaches 3.5-4x. The asymmetry is wide enough that halving the upside and doubling the downside still produces a positive expected value.

Re-Rating Mechanics: Why a Deal Drives 200%+ From Here, Not 10%

A market-microstructure point underlies the upside case.

When mature AI infrastructure names — IREN, WULF, CIFR, APLD at current scale — announce hyperscaler deals, the stock typically moves around 10%. Optionality is already embedded, and announcements function as confirmation rather than revelation.

Smaller, less-followed names behave differently. DGXX has announced materially smaller deals than what NUAI is contemplating and moved 50%+. Expectations are not embedded, the float is small, and the announcement forces a re-rating from speculative microcap to credible AI infrastructure platform (Note that a deal cannot be priced in because many institutions are waiting to buy until after a deal is announced).

NUAI sits closer to the $DGXX end on market cap and visibility but closer to the IREN/WULF/APLD end on asset quality and counterparty caliber. That mismatch is the opportunity. A first hyperscaler deal at TCDC could plausibly drive an immediate 200%+ re-rating — not because steady-state fundamentals support that exact multiple, but because microcaps gap rather than incrementally re-price. Investors do not get to scale into the new range.

Downside is bounded by the existing balance sheet, which is clean post-Macquarie and post-equity raise with no SharonAI overhang. Upside is a non-linear re-rating event.

The Case for Data Center Exposure

A reasonable question, given the breadth of the AI investable universe — semis, photonics, custom silicon, robotics, model labs — is why allocate to data center developers at all.

Data center economics are durable in a way most AI-adjacent verticals are not. Hyperscaler colocation leases run 15-20 years. Counterparties are investment grade. Cash flows are recurring. Once a campus is leased, it produces something close to a bond. EQIX has compounded through every macro cycle of the past fifteen years on this dynamic, and the structural reason is simple: an AWS region does not get turned off because the economy slows. Compute demand is structurally inelastic at the margin, and existing infrastructure is locked into multi-decade obligations.

The asset class is also tractable for non-specialists. Underwriting reduces to power, land, customers, and contract terms. Many other AI-adjacent verticals — photonics, custom silicon, neuromorphic, edge inference — are genuinely interesting and likely lucrative, but the underlying technology evolves quickly enough that most investors cannot reliably assess winners. Data centers fit Buffett's "in pile" — comprehensible, durable, and underwritable on standard metrics.

The constraint is that asymmetric opportunities within the data center space are increasingly scarce. For WULF to 5x from current levels would require multiple gigawatts of new capacity, additional contracts, and substantial revenue growth — achievable but grinding. NUAI requires one announcement with one of four hyperscalers for Phase 1 of TCDC. The bull case condenses to a single press release.

For investors who participated in the 2025 IREN/WULF/HUT/APLD/CIFR cycle, NUAI offers the same trade structure with two improvements: the underlying thesis has been validated by the prior cohort's outcomes, and the macro evidence — exponential capex guides, tightening power constraints, structural undersupply — is materially stronger today than it was eighteen months ago.

Conclusion

NUAI is structurally identical to the IREN, WULF, and APLD trades in early-to-mid 2025, with three improvements. The thesis has been validated by the 2025 cohort's outcomes. The execution stack — Stream / Apollo / Macquarie / Ramboll on day one — is more institutional than what several of those names had at first announcement. And the forcing functions are tighter, with a six-month Macquarie clock combined with a hyperscaler-organized JV on 650 MW of secured Texas power.

The position reduces to a single proposition: one press release reprices the equity by triple digits. Downside is bounded by an institutional cap table and a clean post-raise balance sheet. The expected value math holds at 50% probability and compounds at the 90%+ probability the structural setup supports.

Simply put, this is a remix of the IREN/WULF/APLD trade.

English

I’m 60, and my son is 33. He still lives in my house, sleeping in the same room he grew up in and using the same closet I built for him when he was ten. He eats the food I prepare for him every day. He doesn’t work, doesn’t study, and doesn’t look for anything. He wakes up late, turns on the television or computer, and that’s how his day passes. If I don’t serve him breakfast, he skips it. If I don’t wash his clothes, he leaves them piled on a chair until he has nothing clean left to wear.

But it wasn’t always this obvious. It started years ago, little by little, and I allowed it all to happen.

When he was a child, I didn’t let him do anything on his own. I tied his shoes until he was twelve because he said it took too long. I did his homework for him “so he wouldn’t get stressed.” If there was a problem with a teacher at school, I went to speak on his behalf. If he argued with a friend, I stepped in. I always told myself, “He’ll have time to suffer when he’s an adult.” I never let him experience discomfort.

English

English

1. @BarakRavid falsely claimed a peace deal was imminent to crash the oil market >5 times

2. Always before @axios publishes the false claims, massive short positions are taken against oil: this is insider trading

3. He's world's worst journalist: what he says is debunked in hours

أحمد جعفر - Ahmed Jaafar@ahmjaf

This is the price top journalists pay for breaking major scoops.. When you become No.1 in the Middle East, the smear campaigns and antisemitic attacks follow. Decent people should speak out against this hate..

English

@pxue @refanatic69 He may or may not make that but his statement is correct. Salaries in Canada and CAD are compressed

English

this kind of comp in Toronto gets me excited.

$130k salary you can rent a $2.5k/m unit downtown for about 25% of your gross salary, so no commute time. comfortably saves if you want to, and get meaningful equity ~10k options vest over 4 years.

i'd like to see new grad out of Waterloo get this role role.

English

@GavMcCracken @invdiary Is this the aisc or geopolitics? Kinda like the nxe dnn vs pdn glo

English

@Jesse_Investing @SingularityRes Yes very possible. Nuai hit a low of 32c back in Sept. Once the tenant drops this will rip off faces

English

A $12,000 investment in $AXTI an year ago would be worth $1,036,800

Even better than San Disk $SNDK

English

I don't get why people think that I said a bear market is starting for gold? Can't they see my pinned post? This is a hypothetical situation about any bear market.

English

I think TRUE gold and silver stackers are a VERY rare bread.

If you are REALLY honest with yourself, there is SOME part of you that would PREFERABLY not hold through a decade long bear market.

Life is too SHORT for that.

English

@pinetree_cap Fair the volatility is nuts. But that's how generational wealth is made. Unless you're in SanDisk, in which case volatility is only upwards 😂

English

@theBestBlock I wish it is above 200 at end of year. I want to sleep with peace.

English

I sold IREN X minutes minutes ago. I am done with it. I will not talk about it, in any capacity. Good bye and wish everyone luck. I bought it at all time high last year and today, I get out at a few points above my costs basis plus 7k premium I received which was one time.

I hope they do better, I hope they do better than everyone but I am exiting it.

English

@darjv4barry @radog_77 They closed Hormuz for 2 months and you think oil is going back to $80?

English

@radog_77 Yes, oil is going lower

My fair value is $80 at this moment

$70 will be a buying opportunity

Too much demand destruction already occurring for oil to.continue higher

Hyperinflation is the only way oil goes to $200+ from here without pulling back to $80 first

English

@dandelion12234 The only way to realize massive gains from winners is to fall into a coma...

English

@theBestBlock yup. we are in the last leg of the marathon. just go in your room and play video games for a month like dulce and then we will have deal.

English

i'm gonna lose my shit if $nuai doesn't close a deal soon

English