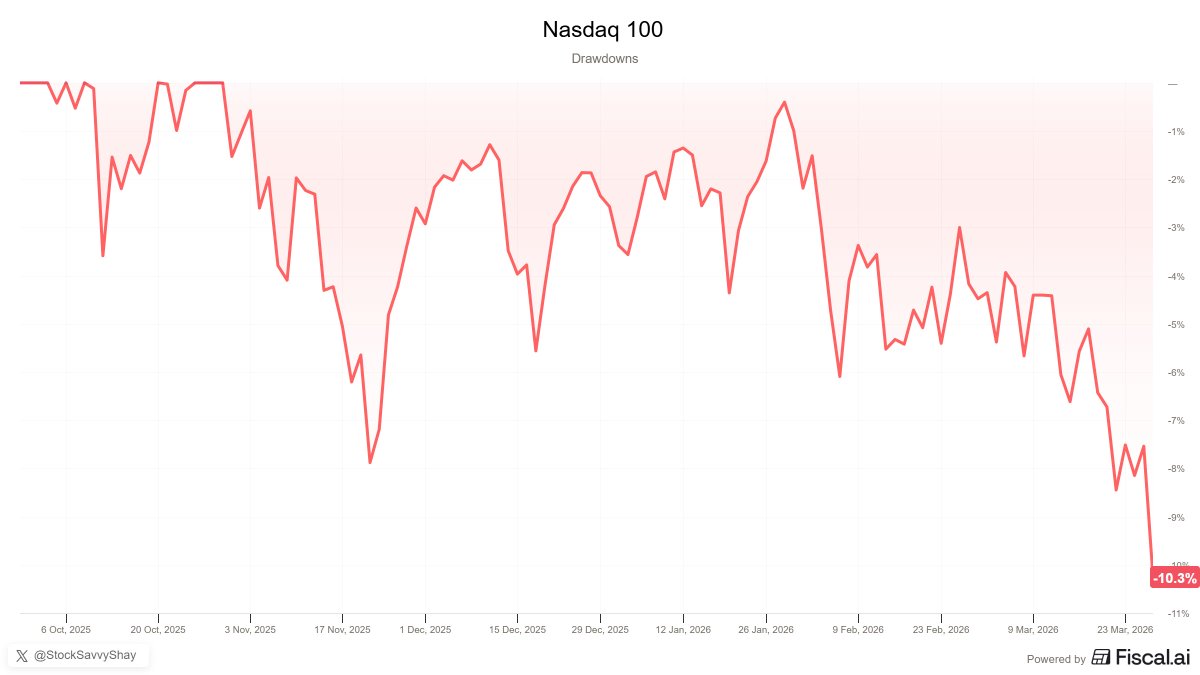

Sabitlenmiş Tweet

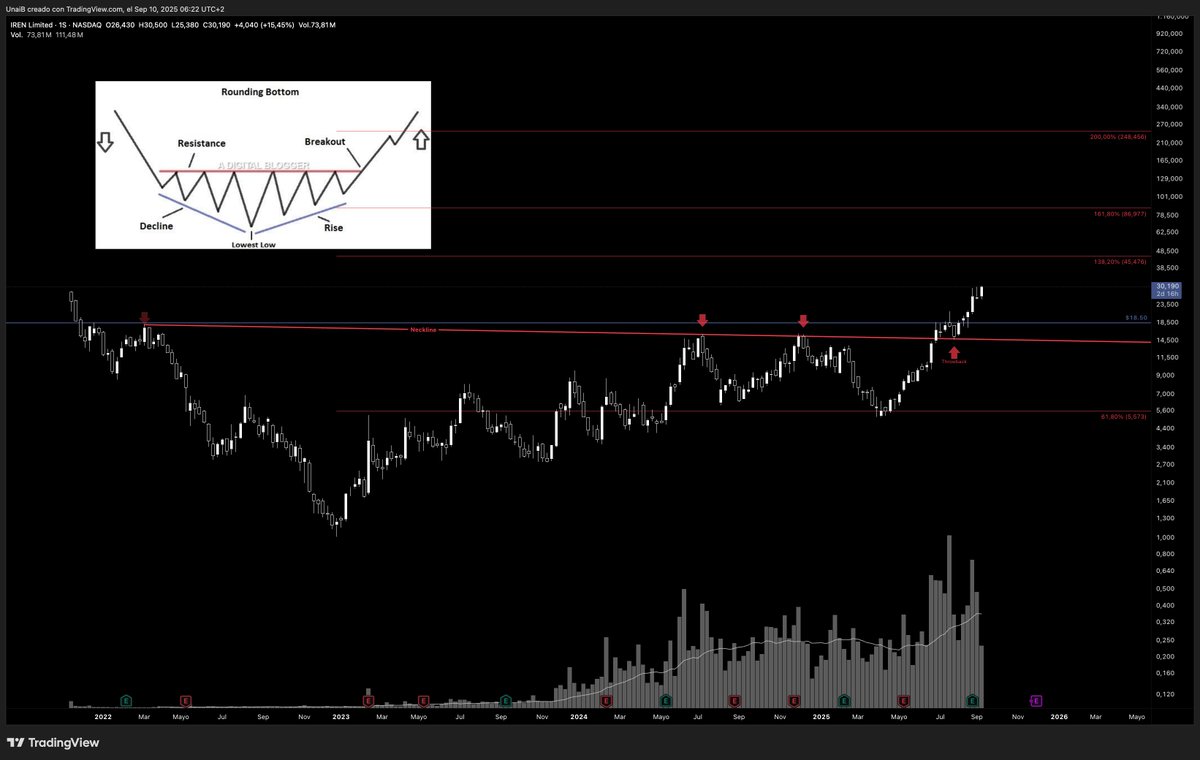

$IREN – Rounding Bottom Update

The breakout above $18.5 has confirmed the rounding bottom pattern I posted earlier.

Now the Fib extensions point to:

• 1.38x → ~$45

• 1.62x → ~$87

• 2.0x → ~$248 (long-term target)

This is no longer just “crypto miner” price action. The market is starting to re-rate $IREN as AI-native infrastructure.

Strong volume, strong breakout, strong thesis.

Unai@unaibld

$IREN Breakout in progress? The rounding bottom structure on the weekly chart is nearly complete after over 2 years of consolidation. - Key zone: $16.80–$18.50 - Rising volume - Precise rejection at $18.54 this week - Long-term bullish pattern close to triggering Technical target: $36 Parabolic (log scale) target at $335 👀 Pullback to $14.50–$15 could be a tactical opportunity.

English