user

74 posts

I have a good buddy in SaaS land who built one of these:

6 people, $3 million in ARR - a VMS with a niche market and very legacy competition.

They never earned a profit, but he worked his ass off to cover an okay salary and try to grow enough to justify the capital he’d raised.

Making sales was hand-to-hand combat: most software does not sell itself. It takes labor and time and adaptability.

While my buddy ended up crushing it on a 10x ARR exit, if the idea is AI is going to cause a thousand software flowers to bloom, exit multiples will keep coming down as growth will be harder and more expensive, even as LTV declines from competitive churn.

And AI-based SaaS will have lower gross margins to cover other costs because tokens and models are very expensive.

Brutal.

That combination removes “crushing it on the exit” from the equation, which means these tiny ARR businesses that don’t generate a profit will be little more than okay paying jobs, but with entrepreneurial downside.

Todd Saunders@toddsaunders

I heard an incredible analogy from a VC friend that I can’t stop thinking about. “The moat in software was the cost of building software. And Claude Code just mass produced a bridge.” It’s wild when you think about the impact of this. The SaaS boom produced a few dozen billionaires and a bunch of zero sum winners. But the AI SaaS era will mass produce millionaires. There will be fewer ServiceTitans hitting $5B valuations, and instead there will be 50,000 companies doing $500K-$5M each, run by 1-3 people with deep expertise and huge margins. To be clear, I believe that the total value of software goes up, and the number of companies created goes up exponentially. But the number of people who capture the value also goes up 100x. I don’t believe in the “SaaS is dying” headline, I think it’s missing the point. It’s simply that the power of SaaS is changing hands.

English

Guys it's up to the board of $PYPL to choose what price to sell PayPal at.

Guess who is on the board? Enrique Lores the new CEO who left his million dollar a year job at HP for PayPal

His bonus starts at 60% $83.2 a share

The CEO is fully incentivized to sell PayPal $83+

English

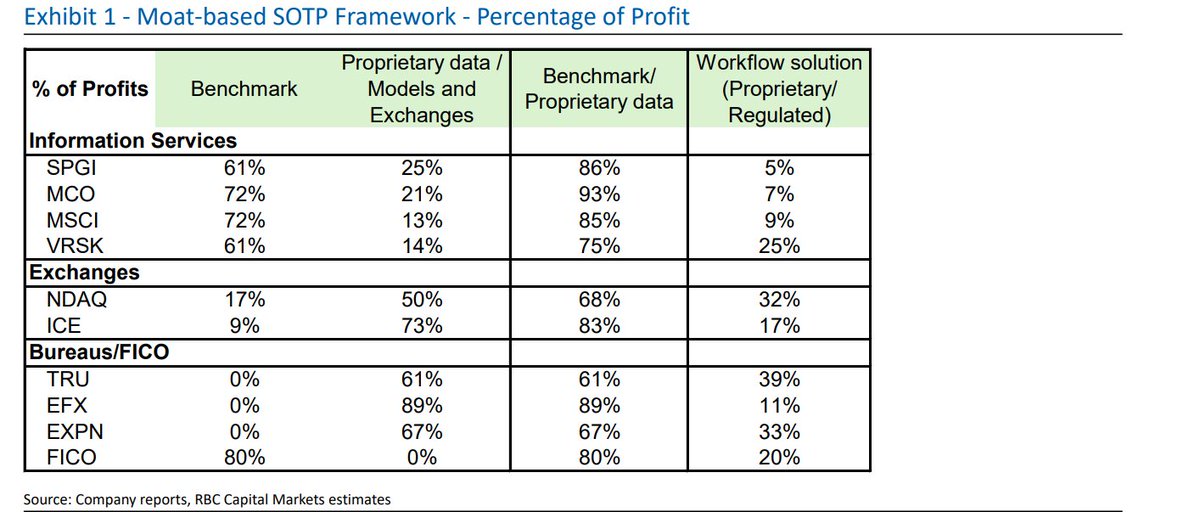

whats the probability that the ai labs/LLMs torch every corner of enterprise software (including security) except for the incumbent database vendors whom are left intact in perpetuity

Brad Gerstner@altcap

Databricks just crushed numbers bc of AI. Clickhouse is accelerating bc of AI. Snowflake likely the same. AI worklows being built on their data. But too many software companies become more at risk as AI improves. I want to own things positively correlated to intelligence. 🚀

English

@buccocapital Great read. I couldn’t help but notice the two companies with the highest risk going forward are the two he’s in competition with (or used to compete with). I agree with the assessment but quite ironic

English

isnt social media AI agents the same as lighting money on fire?

Derya Unutmaz, MD@DeryaTR_

As people know, I follow AI extremely closely, but this is shocking even to me! I didn’t expect a social media for AI agents like this to take off in 48 hours! Soon, they can form whole AI agent societies, and then an AI civilization may emerge? AI wierdness is getting wilder!

English

$CSGP finally about to give that all clear but they nuked their equity for another year instead.

13F investor@cloneinvestor

@JerryCap I bought a home 6 months ago and not once did I use homes.com. I tried because I love $CSGP but just couldn’t. I only used Zillow and I don’t know why other than I liked it.

English

@JerryCap @CapitalJurassic The core business trades at high teens forward ebitda and is a monopoly lol if they cut homes or it works out, this trades above 100

English

@CapitalJurassic it's getting cheap! think downside of 40 is as low as this could go. anything in 50s seems reasonable. core biz is amazing

English

@endowment_eddie Is the S&P500 really comparable to PE-backed companies? Strip out the Mag 7, or use the Russell, and the charts probably look more similar (especially if you looked at EBIT)

English

Here’s the trend—what do we think? Rev/earnings appear to be moving in the wrong direction versus public markets.

English

What is the state of PE-backed companies? Golub provides metrics for the 110-150 companies in its loan portfolio.

YoY numbers are not looking great. A better question, what’s the price/volume mix?

English

@endowment_eddie I’m sure there are some circumstances where an IPO is feasible.. there have been many down round IPOs recently. But most companies have late stage investors with a way of blocking a liquidity event

English

@user7397 True but things were heady during ZIRP and most of these businesses have straight 1x preferred sitting up top

English

Here’s a question. Why don’t more companies that don’t meet 30% growth/$300M ARR go public?

Let’s say a hypothetical company has $200M in rev, 15% growth and can trade in public markets at 5x. It last raised $250 in 1x pref valued at $2.5B.

You could sell to PE for $1B (5x rev) or go public. Management and early investors don’t want to sell with $250M of overhang. In the sale, late stage investors would get 25% of proceeds with $750 for common (simple 1x liq pref).

But if you IPO at $1B, and there is no ability to block, late stage investors get call it ~10% as converted and common has $900M.

So, do a small IPO, ignore limited liquidity, coverage etc. Do the IPO to clear the pref stack and you’re still worth $1B publicly or more to an acquirer. Or at least use threat of IPO to negotiate with those higher up the capital structure.

What am I missing?

English

@bgurley @jaminball Check out IPO performance 3-5 years later. Doesn’t seem like a bad deal for the vast majority of companies based on LT performance. Some great companies have been dead money for years

English

@jaminball You can just visit site.warrington.ufl.edu/ritter/ipo-dat…. Jay Ritter has all the data. What’s amazing is when you cut it by lead bank. Underpricing shoots from 18% to 30%. Across all IPOs. Also VC deals have way more underpricing than PE.

English

I was asked on the internet which is simpler, an IPO or a DL. Here is the answer and detail. Fewer steps in a DL. And more access for ALL investors.

Bill Gurley@bgurley

@Trace_Cohen @vishalkgupta @kaminskymethod The DL is much simpler than the IPO.

English

@bgurley VC play a similar game. Mark ups heading into a fundraise, raise a larger fund, collect more management fees, have your friends invest in next round to mark up the asset, etc. And most of the funds end up sucking anyways. I bet this HL fund has better net returns than avg VC fund

English

An all-private-all-the-time world will be a much messier world with even more opportunists and charlatans. Transparency is an investor’s friend. Darkness/obfuscation is not.

Leyla@LeylaKuni

Drop everything and read this article - @jasonzweigwsj describes how Hamilton Lane, in their new secondaries fund, buys assets at a discount, marks up the NAV *immediately* and earns their carry on *unrealized* (!!) gains. Let me translate via example: 1. you buy a house using OPM for $450K in cash (let's say you split profits with investors 50/50) 2. you say the market value is $500K the day after you bought the house (even though you just paid $450) 3. You pay yourself $25K on *unrealized* gains (years before you sell the house itself) 4. Next year you say the house is worth $540k. You pay yourself another $20K in *unrealized* gains - and so on... Democratization of private assets in full swing

English

The boring way to get rich:

1. Play the right game. Pick the right company and the right job

2. Work your ass off

3. Put yourself in as many positions as possible to get lucky

4. Save a lot, early

5. Don’t interrupt compounding

6. Live within your means

7. Don’t divorce

8. Wait

fapital@Fapital3

how do young people get rich besides crypto

English

Should All In launch an All In Fund of Funds that allows retail investors to leverage our collective access to startups, venture funds, hedge funds and PE funds?

If the size was big enough, we could negotiate some great access AND fee discounts.

English

might be why companies staying private longer...need extra years to get that MOIC up

Jack Altman@jaltma

There has been lots of talk recently about how the new cohort of mega funds might play out in venture. Josh had the most cogent analytical take I've heard, the "venture arrogance score".

English

@corry_wang There are some vendors that have networks effects, or are multi player with external participants, like Figma or Procore. That’s a moat that makes it different this time perhaps?

English

8/ To be clear, this is not a next 12 month event: I would be amazed if this were the case by 2027, much less 2025

But I do think recent progress on SWE-bench is actually measuring something real... and I don't feel like people have really thought through all the implications

English

1/ If you really believe LLMs will dramatically compress the cost of software development in 3-5 years, doesn't this obviate the reason for independent software vendors to exist?

This doesn't seem obviously crazy to me - it'd just be a return to the days of mainframes

English

@patrick_oshag you should read Uncommon Sense by Alan Cromer; it's on Munger's book list. Highly recommend and might change your prospective here.

English

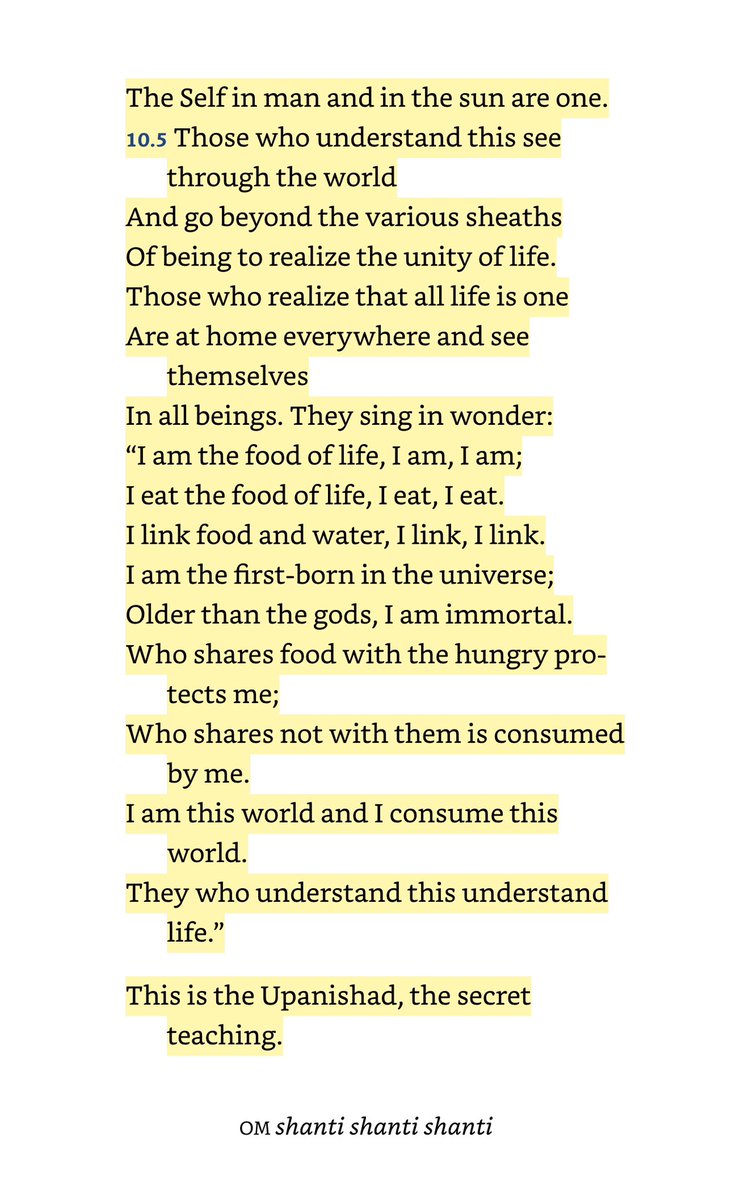

This knocked my socks off when I was 25

Read it most days since

Taittiriya Upanishad

English