Valelelelele

25 posts

Based on Master @zephyr_z9’s recent tweet, it might be a bullish article instead. Anyway I will buy back tomorrow when the uncertainty clears. I think “Unpopular” in Citrini’s tweet is ambiguous but most of the market interpret it as bearish.

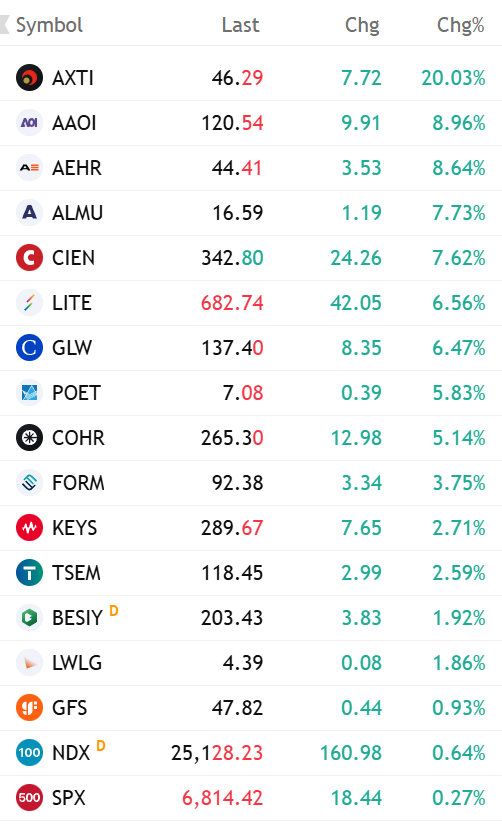

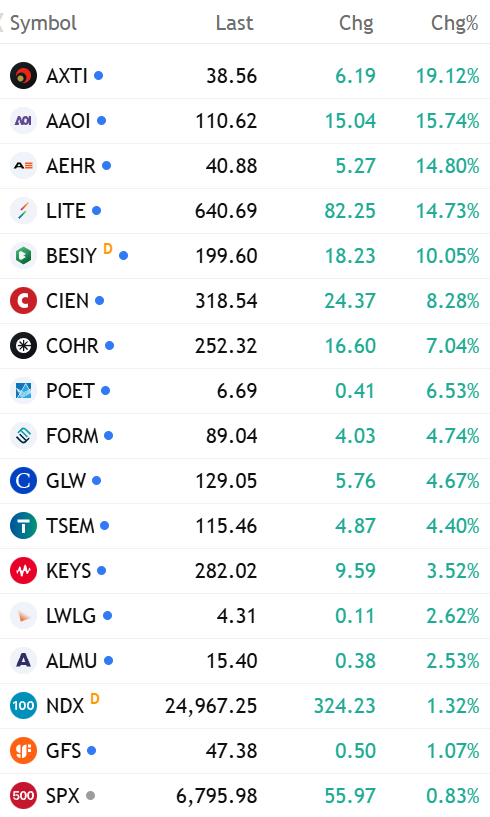

As of March 9, 2026 The Silicon Photonics and Optical Networking sector is showing strong bullish momentum, led by a massive surge in $AXTI. This follows renewed investor confidence regarding the company's progress on export permits and surging demand for its indium phosphide substrates used in AI optical infrastructure (simplywall.st/stocks/us/semi…). The explosive growth of AI data centers has created a massive bottleneck in data transfer speeds, shifting the industry focus from compute power to optical interconnects. This is driving a structural re-rating across the entire optical supply chain, from foundational materials to advanced packaging and testing, as hyper-scalers aggressively upgrade to 800G and 1.6T networking to support next-generation GPU clusters. $AXTI: 19.12% $AAOI: 15.74% $AEHR: 14.80% $LITE: 14.73% $BESIY: 10.05% $CIEN: 8.28% $COHR: 7.04% $POET: 6.53% $FORM: 4.74% $GLW: 4.67% $TSEM: 4.40% $KEYS: 3.52% $LWLG: 2.62% $ALMU: 2.53% $NDX: 1.32% $GFS: 1.07% $SPX: 0.83% 1. Optical Components and Foundational Materials $AXTI, $COHR, $GLW: These companies provide the essential raw materials, advanced lasers, and physical fiber-optic glass required for high-speed light transmission. $POET, $LWLG, $ALMU: Represents specialized, emerging bets on next-generation photonic integrated circuits and electro-optic polymers designed to lower power consumption. 2. AI Networking and Transceivers $AAOI, $LITE, $CIEN: These players are directly capitalizing on the data center upgrade cycle, supplying the critical optical transceivers and high-capacity routing equipment that link AI servers. 3. Advanced Packaging and Semiconductor Manufacturing $BESIY, $TSEM, $GFS: Foundries and equipment makers enabling the physical integration of optical and electrical components through hybrid bonding and specialized silicon photonics manufacturing. 4. Testing and Validation Equipment $AEHR, $FORM, $KEYS: The surge in complex silicon photonics demands rigorous wafer-level testing and signal measurement to ensure component reliability before deployment in mission-critical AI data centers.

$AXTI AXT Inc (AXTI) Q4 2025 Post-Earnings Debrief atlaspeakresearch.com/report/f04f05 AXT Inc reported Q4 2025 revenue of $23.0M, missing its own guidance range of $27–30M due entirely to China MOFCOM export permit delays — the company disclosed its first-ever permit denials (with resubmission instructions). Despite the revenue shortfall, InP backlog surged to a record $60M+ and management delivered the most emphatically bullish commentary in years, describing customer demand as growing "3, 4 or 5x over the next 4 or 5 years" with CEOs — not purchasing managers — personally engaging on capacity. The investment debate has shifted decisively from "is there demand?" to "can they get permits and build capacity fast enough?" — a structurally different risk profile that underpins the stock's 646% rally from its October 2025 low.

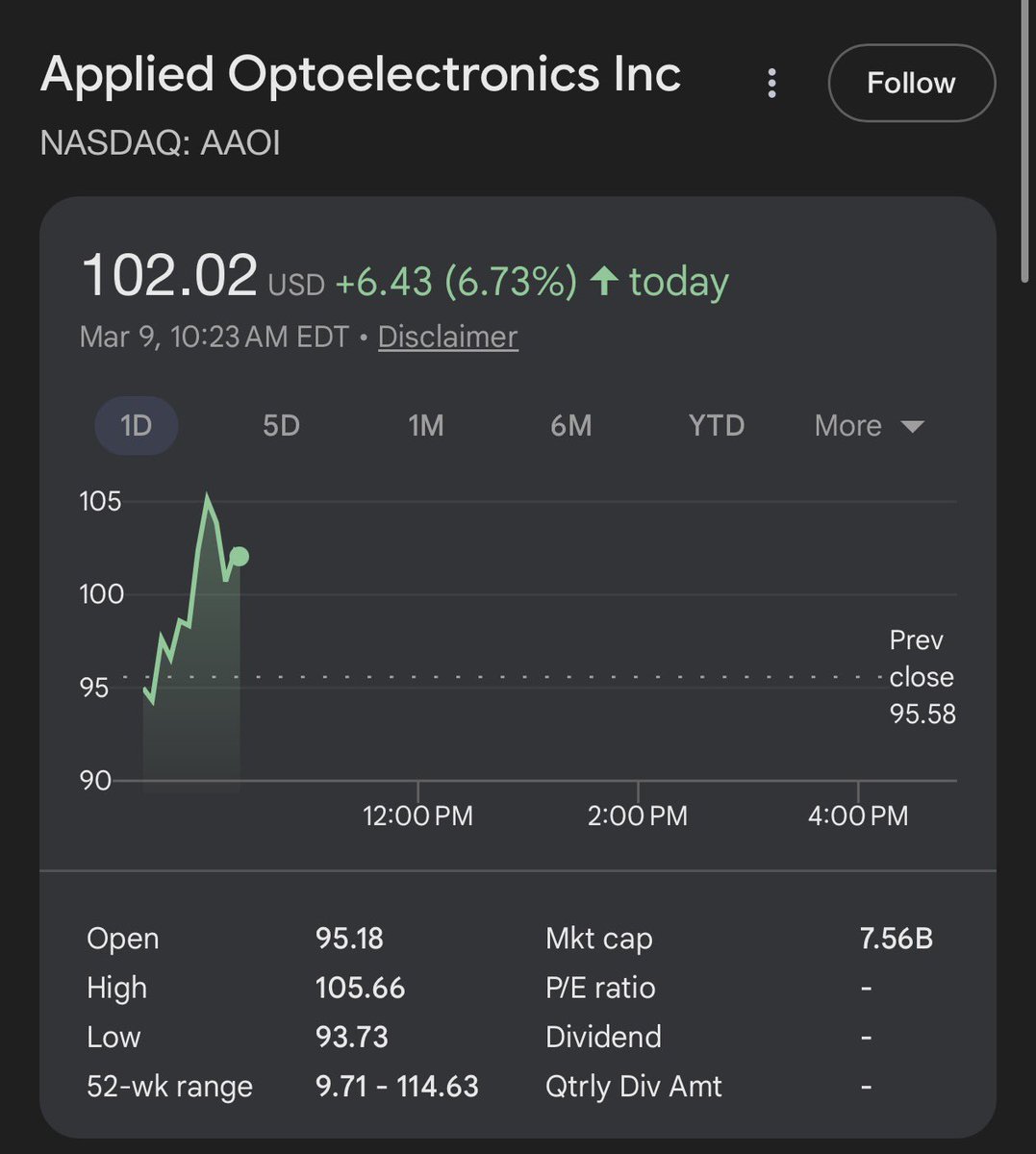

$AAOI is up 24% and $LITE is 5% since my thesis today. From BOM analysis, LITE ($27B) is levered toward TPU Ironwood due to OCS but benefits from NVDA + all ASICs. AAOI ($2.5B), is levered toward MSFT MAIA ramp and Amazon Trainium. InP like HBM, will be a bottleneck for 2026 as they’re the foundational materials used for lasers in these deployments. Similar to memory bottlenecks with Micron and SK Hynix, we’ll likely see attention drawn to InP fabs, such as $AAOI, which happens to be one of the sole ones in America (COHR,Macom) But compared to $LITE that is up 362% YTD due to the success of Google’s TPU (from Meta and Anthropic purchase orders), $AAOI is only up 7% YTD. We’re largely seeing this because there’s a lack of retail or media attention on the $AMZN Trainium or $MSFT Maia deployments, which are largely expected to ramp up in 2026-2027. However they’re all likely to succeed due to each hyperscaler wanting to lower costs of inference for their own cloud platform. If we see other hyperscalers adopt OCS for optimized performance that the TPU achieved, expect $LITE to re-rate more than they have now given their monopoly in that specific segment. However, if we see $MSFT Maia ramp up (given $AAOI is likely developing a new architecture for them), and $AMZN Trainium ramp up ($4B warrant + purchase orders), expect $AAOI to rerate. Photonics and InP will be the new bottleneck like memory. We’ll likely see investments pour down stream to players like $COHR, Innolight, $LITE, and hidden levered plays on specific hyperscaler ASICs like $AAOI as a theme in 2026. The market is currently rewarding the Google TPU supply chain but might be missing other hyperscaler ASIC ramps.

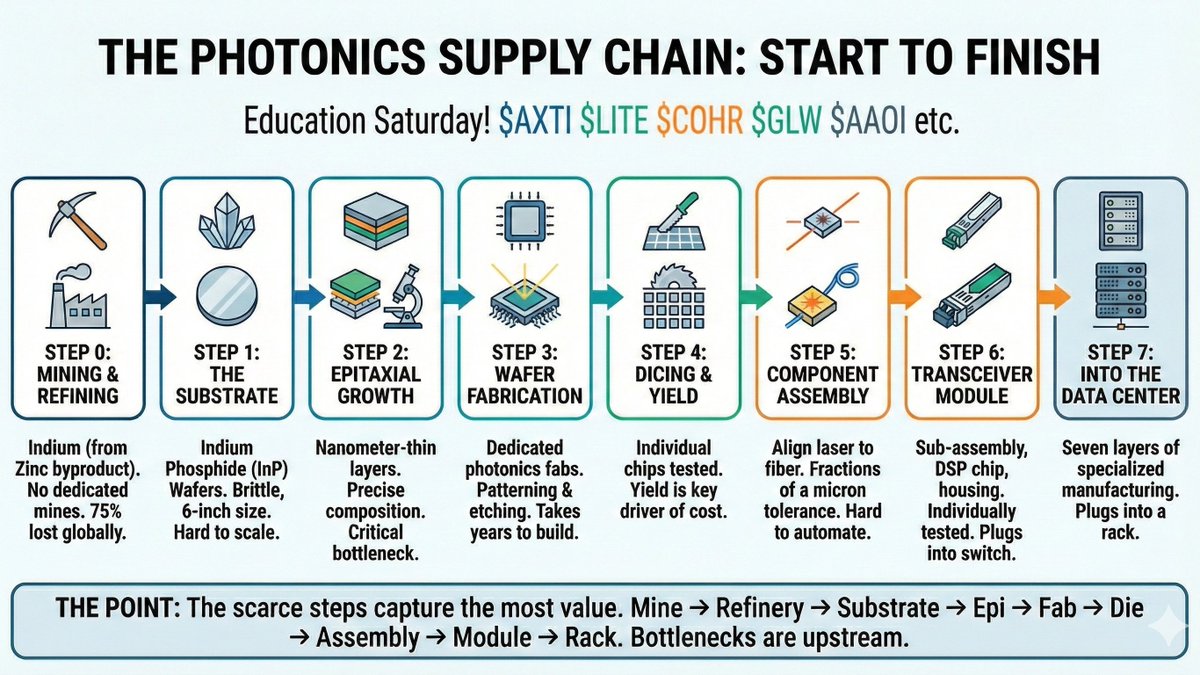

Education Saturday📓 Photonics Glossary and Key Terms If you follow $LITE, $COHR, $POET, $AAOI, $ALMU etc. these are some the terms that you should know that will show up on the calls Photonics Photonics is the use of light to move information instead of electricity. AI data centers are hitting physical limits in copper at higher speeds, so more of the network shifts to optical. Laser A laser is the light source that makes optical links possible. When laser supply is tight, the entire optical stack feels it because everything downstream depends on that photon supply. Indium Phosphide (InP) Indium Phosphide is the material used to make many high-performance lasers for data centers. Scaling InP capacity is hard, so shortages can translate into pricing power and better margins for the suppliers. EML (Electro-Absorption Modulated Laser) An EML is a laser where the modulation function is integrated on the chip. EMLs are a key workhorse for 800G and 1.6T links, and they tend to carry higher value because they solve harder signal and reach requirements. CW Laser (Continuous Wave) A CW laser is a laser that stays on continuously while modulation happens elsewhere in the system. CW lasers become more important as architectures move toward silicon photonics, co-packaged optics (CPO), and external light source designs (ELS) Transceiver A transceiver is the pluggable module that sends and receives data over fiber. Transceivers are where optics becomes a finished product, and the competitive set depends on whether a company sells the full module or supplies critical parts inside it. DCI (Data Center Interconnect) DCI refers to optical links between data center buildings or campuses. Longer reach usually means higher performance requirements, which increases the dollar content and the importance of specialized lasers and components. Coherent Optics Coherent optics is a more advanced way to encode data for very long distances like metro and long-haul networks. Cloud backbones keep upgrading, and that creates demand for specific laser types and high-end optical components. CPO (Co-Packaged Optics) Co-packaged optics places optical engines next to the switch chip instead of relying only on pluggable modules at the edge. It pulls optics deeper into AI systems and increases demand for ultra-high-power light sources. OCS (Optical Circuit Switch) An optical circuit switch uses optical paths to dynamically route connections inside AI clusters. It adds new optical hardware into data centers and can change how networks are built as clusters scale. ELS (External Light Source) An external light source centralizes lasers in a separate module and feeds light to many lanes through fiber. It can shift value toward shared light engines, increase total laser demand, and create a new packaging layer that multiple companies want to own. Optical scale-out Optical scale-out is the rack-to-rack network inside the data center, and it is already heavily optical today. This is where most current photonics revenue is concentrated. Optical scale-up Optical scale-up is the short-reach connectivity inside the rack, which is mostly copper today. As racks get denser and speeds rise, optics can move inward, expanding the photonics opportunity beyond traditional pluggables. Optical interposer An optical interposer is a packaging platform that integrates and aligns optical components inside a compact module. Photonics economics are heavily driven by manufacturing and test complexity, so packaging approaches that scale cleanly can change cost per lane. III-V on silicon III-V on silicon refers to putting compound semiconductor performance onto larger silicon wafer formats. It targets the long-term laser capacity bottleneck by aiming for larger wafers and lower cost manufacturing, even though it is still early. So think about it all like this. Photonics is a stack. Lasers sit upstream, packaging determines manufacturability, modules sell into volume, and new architectures like CPO, OCS, and ELS pull optics closer to compute. If you found this useful, please bookmark & share!

🥳 3000 Follower! 🥳 Mit freundlicher Unterstützung von @Stock_Bonvivant @ttt_financial @ball_hartwig. Vielen Dank! Wie immer möchte ich ein Special machen. Ask-Me-Anything wäre ein Klassiker, aber vielleicht habt ihr einen guten Vorschlag. Lasst es mich wissen!