Sabitlenmiş Tweet

Wade

15K posts

Wade

@wsenti

Gator Grad, President at AML 🇺🇸🧲 . Opinions are my own not advice/endorsements by employer or investment advice.

Melbourne, FL Katılım Ağustos 2013

1.3K Takip Edilen661 Takipçiler

🧲⚗️ The Step Nobody Talks About — But Everything Depends On

Between a barrel of rare earth oxide and a working magnet sits the most strategically critical — and most geopolitically controlled — step in the entire chain.

Metallisation. REO → Metal. It's where China wins.

China controls 91–95% of global rare earth metallisation capacity. It's not geology. It's 30 years of state-backed industrial scale, cheap energy, and deliberately suppressed competition.

Here's why it splits into two completely different processes — and why you can't just pick one: 🧵

⚡ PROCESS 1 — Molten Salt Electrolysis (MSE)

🔬The Heavy Lifter for Light REEs: Nd, Pr, NdPr

REO dissolves into a fluoride salt bath at ~1,050°C.

Apply direct current. Nd³⁺ ions reduce at the cathode. Liquid neodymium pools at the base. Gravity separates it from the slag.

That's the Nd going into your EV motor magnet.

Light Rare Earths (LREEs)Neodymium (Nd), Praseodymium (Pr), Cerium (Ce), Lanthanum (La),

⚗️Molten Salt Electrolysis (MSE)

Low elemental melting points; total absence of stable RE^{2+} redox cycling; high Faradaic current efficiency.

Western reality check:

🇬🇧 LCM (Ellesmere Port, UK) — the only non-Chinese-owned commercial MSE facility in the Western world. Expanding from 2 cells → 6 cells → 330 tpa NdPr.

🇺🇸 Phoenix Tailings (Woburn, MA) — proprietary mixed halide bath at ~700°C (vs 1,050°C standard). Zero PFCs. Zero toxic byproducts. 35–45% less energy. Fed by mining waste tailings. Targeting 3,000+ tonnes by 2026.

🔥 PROCESS 2 — Metallothermic Reduction

🔬The Precision Tool for Heavy REEs: Dy, Tb, Sm

You cannot electrolyse dysprosium. Or terbium. Or samarium.

Their chemistry breaks the electrolytic cell — stable 2+ oxidation states cycle ions back to the anode without depositing metal. Faradaic efficiency collapses to near zero.

So instead: fluoride the oxide → load anhydrous fluoride + calcium metal into a tantalum crucible → seal in vacuum induction furnace → heat to ~1,500°C → calcium strips fluorine → liquid Dy/Tb metal sinks, CaF₂ slag floats → separate → vacuum purify to >99.9%.

For samarium: lanthanum reduction-distillation — Sm vaporises under vacuum and condenses as pure crystalline metal on water-cooled baffles. Every gram of SmCo magnet in every defence platform in the world was made this way.

Heavy Rare Earths (HREEs)

Terbium (Tb), Dysprosium (Dy), Gadolinium (Gd), Yttrium (Y)

⚗️Calciothermic Reduction

High elemental melting points; strict requirement for high purity in magnetostrictive and high-coercivity applications.

High Vapor Pressure & Variable Valence Rare Earths,

Samarium (Sm), Europium (Eu), Ytterbium (Yb), Thulium (Tm)Lanthanothermic

Reduction (Reduction-Distillation)

Western reality check:

🇬🇧 LCM — added DyFe and Tb commercial production in 2023. Also the only company worldwide operating solid-state SmCo co-reduction commercially.

🇺🇸 REalloys (Euclid, Ohio) — scaling the largest HREE metallisation facility outside China, targeting 30t Dy + 15t Tb pa from SRC Saskatchewan feed.

🗺️ Why This Is the Strategic Chokepoint

Japan has 50%+ of Western NdFeB patents.

But without Dy and Tb — which flow through Chinese metallisation — those patents cannot be exercised at premium performance.

The West has mines. It's building separation.

But metallisation — REO to metal — is the missing link that still runs 91–95% through China.

LCM and Phoenix Tailings are the West's real answer. Small now. Scaling fast. Every tonne they produce is a tonne that doesn't need a Beijing licence.

📊 See infographic for full process comparison. Video from LCM in the thread, coming soon

l

🇬🇧🇦🇺🇺🇸🧲

@LCM_Metals @PhoenixTailings @realloys

#RareEarths #Metallisation #NdFeB #Dysprosium #Terbium #Samarium #MoltenSaltElectrolysis #MetallothermicReduction #LCM #LessCommonMetals #PhoenixTailings #REalloys #CriticalMinerals #SupplyChain #WesternSupplyChain #DFARS #NationalSecurity #EV #EVMagnets #DefenceMagnets #SmCo #NdPr #HREE #LREE #MagnetMetallisation #LCM #MagnetRecycling #AdvancedMagnetLab 🔬⚗️🧲🌏

English

@robert_ivanhoe @washingtonpost We have a major overhaul needed in the United States..

English

As we have highlighted before, U.S. mining schools collectively graduated about 300 mining engineers last year, according to @washingtonpost. China, by contrast, is home to about 45 mining engineering programs and churns out about 3,000 graduates every year, according to 2024 estimates.

Rapid upskilling and training is needed to catch up and this a good step in the right direction.

whitehouse.gov/presidential-a…

English

Miss Alice-Faye's owner wouldn't change her litter box so she went on the floor. The owner was going to euthanize. Luckily earth angels swept & she's starting a better life in NY. Captain Alyssa says she's the sweetest passenger & it's Co Pilot Amanda's 1st PNP Freedom Flight

English

Wade retweetledi

Not a single application so far for the sweet boy who was set on fire, Cinder.

He's been at PetSmart for a week, seen by 100s of people, and no one has been able to look past his scar...

Cinder loves to be picked up. He gives hugs and kisses. And they still turn away...

English

@ErnestScheyder @JarrettRenshaw It’s just as much ‘The War Above’ these days

English

What are rare earths?

Why should you care about lithium?

How did China come to dominate the critical minerals industry?

What does this mean for our world?

Get answers in my book and read about the people and places behind this global battle to power our lives:

English

@roblun1 We at @AMLInnovation are prepared to deliver before deadline, many tons, not 10,000 tons, but a lot! 🧲🇺🇸🤷🏼♂️

English

🚨 The smoke and mirrors are clearing in the U.S. rare earth sector — and what's underneath is a crisis hiding behind a calendar.

8 months to the DFARS deadline. Zero compliant product from any of the heavily funded new entrants. And the U.S. Government Accountability Office says defence procurement has "little visibility" into where any of this is actually being made. 🧵👇

x.com/roblun1/status…

Followup from Yesterday's Story, $700M committed. 8 months to the DFARS deadline. Only two licensed REO separation facilities in the entire country. Zero commercial Dy/Tb output from any of the newly funded entrants.

The Legal Clock Is Ticking ⏱️

Let's be precise about what January 1, 2027 actually requires — because this is being consistently misrepresented.

The final DFARS rule (published May 30, 2024) prohibits the use and acquisition of magnets containing rare earths mined, melted or produced in China across the entire U.S. defence industrial base.

Lockheed Martin, RTX, Northrop Grumman and every defence contractor must source certified, China-free, fully traceable rare earth alloys — verified to the smelting and separation stage — by that date.

This isn't just a sourcing change. It requires full material traceability audits down to the separation stage for every alloy batch. And the U.S. Geological Survey confirmed that as of 2025, only two U.S.-based facilities are licensed for rare earth oxide separation — and neither operates at scale for high-purity NdFeB magnet alloys.

1. The CSIS Warning Nobody Acted On

In April 2026, the Centre for Strategic and International Studies issued a blunt assessment:

"Unless significantly more capacity comes online in the next eight months, adhering to the 2027 deadline may not be feasible."

That's not a fringe view. That's the top U.S. defence think tank telling Congress: the domestic rare earth magnet supply chain you funded — isn't ready.

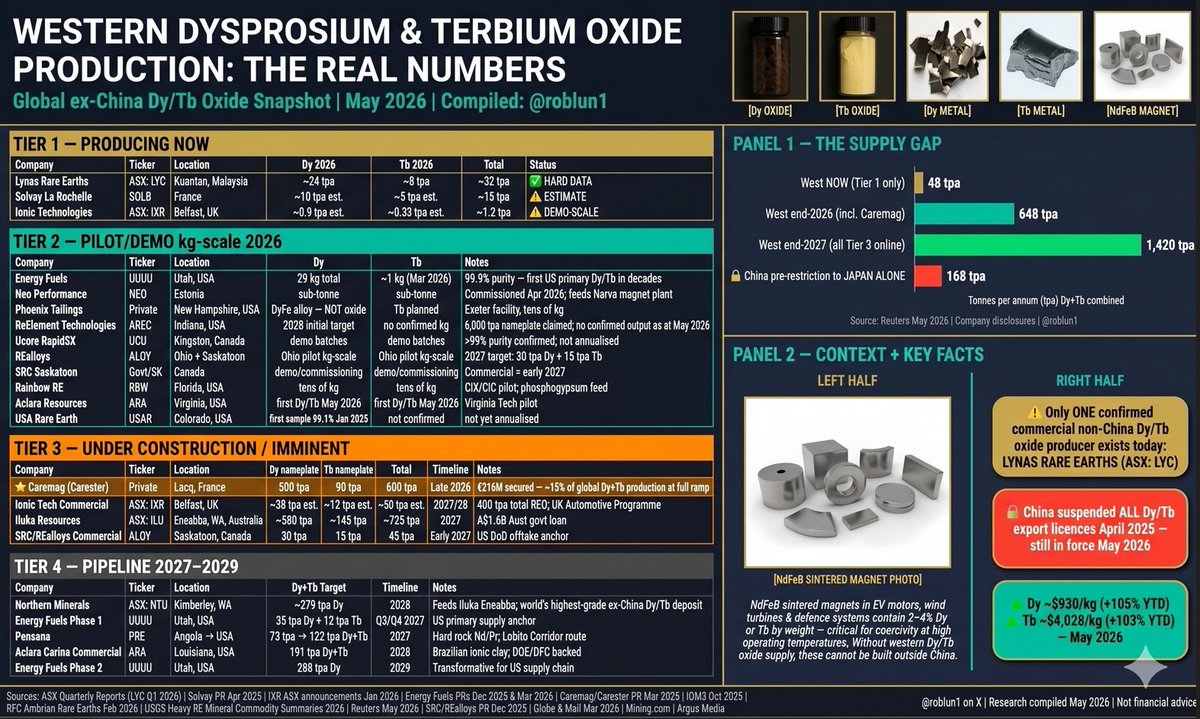

Some magnet production exists outside China — Germany, South Korea and the U.S. But separated, defence-grade dysprosium and terbium oxides at commercial scale?

The West currently produces ~48 tpa combined — from exactly three sources. Lynas at ~32 tpa (the only confirmed commercial producer), Solvay La Rochelle at ~15 tpa estimated, and IXR Belfast at demo-scale with binding defence sales already delivered.

China exports 168 tpa to Japan alone. A handful of companies are in pilot or construction phase —

Caremag in France (600 tpa nameplate, late 2026), Iluka's Eneabba refinery (~725 tpa, 2027), SRC/REAlloys (45 tpa, early 2027) and IXR's commercial Belfast scale-up (~50 tpa, 2027/28).

ReElement — despite its prominent U.S. government backing — has no confirmed Dy/Tb output as at May 2026, with its initial target dated 2028. By end-2027 if all Tier 3 projects commission on time, the West could reach ~1,420 tpa. That's still less than 15% of estimated global demand. The CSIS warning wasn't alarmist. It was arithmetic.

2. The GAO's Inconvenient Truth

The U.S. Government Accountability Office warned last year that more than 200,000 defence department suppliers help produce advanced weapons systems — but there is "little visibility into where these goods are manufactured."

Efforts to map supply chain risks were described as "un-coordinated and limited in scope."

Think about what that means in practice. Defence contractors don't always know where the rare earth content in their subcontractors' components comes from. Some procurement is done three or four tiers deep. Chinese rare earth content is embedded in weapons systems right now and nobody can fully account for it.

"Defence companies not doing a thing for eight years and then going to Congress looking for relief is unconscionable," said lobbyist Jeff Green, whose clients include U.S. magnet and rare earth companies. "I don't think they're going to find a lot of sympathy for the lack of proactivity on the issue."

3. The Waiver Trap

So what happens when January 1, 2027 arrives and the supply chain isn't ready?

Two options are on the table:

A delay via the National Defence Authorisation Act

Waivers granted by the administration for non-compliant items — if companies can show they've mapped their supply chains and made "efforts" toward compliance

Here's why the waiver option is dangerous: it rewards the companies that announced the most and built the least. If you can show a conditional loan letter, an MOU, a signed JV document and a PowerPoint roadmap — you may qualify for a waiver even if you haven't shipped a single gram of separated Dy or Tb.

The compliance pathway becomes a documentation exercise rather than a production reality. And China stays embedded in U.S. weapons systems for another 2-3 years while the sector catches up — if it does.

4. What's Actually Happening Behind the Scenes 🔍

Let me tell you what the press releases aren't saying.

🚩 ReElement Technologies — announced 16,000 tpa Marion Supersite, March 2026, with initial production targeted Q3 2026. Simultaneously, the POSCO JV document (May 2026) — managed by a $70B+ industrial conglomerate — confirms the actual programme targets 3,000 tpa pilot (Q4 2027), scaling to 6,000 tpa by 2030.

The conservative industrial partner is building a fraction of what the press release claims. Pentagon engineers reportedly couldn't validate the scale-up pathway. The $80M conditional loan is under review.

war.gov/News/Releases/…

🚩 Ucore RapidSX — CEO's own website quote: "production scaling up from 2,000 tpa in Q4-2025 to upwards of 5,000 tpa in 2026." Reality as of May 2026: Louisiana SMC is targeting H2-2026 "Early Production" at a single ~600 tpa line.

Genuinely promising technology — but original timeline commitments have not been met, and full commercial scale remains years away.

metaltechnews.com/story/2026/06/…

🚩 Cyclic Materials — positioned as a U.S. recycling solution. Reality: South Carolina campus (operations 2028) produces Mixed Rare Earth Oxides — not separated individual REOs.

It requires a further full SX separation step before becoming DFARS-usable — exactly the bottleneck the whole sector is trying to solve. Cyclic's own Solvay supply agreement sends MREO to France for further separation. It is a feedstock preparation business, not a finished REO producer.

autorecyclingworld.com/cyclic-materia…

🚩 Vulcan Elements — $620M Pentagon conditional loan + $50M CHIPS Act = $670M in government commitments. Verified production base at time of funding: a 10-metric-tonne pilot facility in Durham.

Trump Jr.'s venture fund took an undisclosed stake in August 2025 — three months before the Pentagon loan was announced. White House directed Pentagon staff to close the deal in weeks, not the normal months-long vetting. A 2023-founded startup, entirely dependent on ReElement for every gram of REO feedstock it needs to make a single magnet.

cato.org/blog/white-hou…

🚩 The funding pattern — billions in government capital committed to companies that could not yet demonstrate the core industrial capability they were funded to build.

Private capital crowded in on those government signals. The signals are now publicly contested, timelines revised, and the technical due diligence that should have happened in 2024 is being done in 2026 — eight months before the deadline.

5. The Recycler Behind-the-Scenes Reality ♻️

The magnet recycling space specifically is where the gap between narrative and reality is widest.

♻️ Feedstock doesn't scale the way the models assumed. Every company building a multi-thousand tpa recycling plant needs guaranteed, contracted, high-quality end-of-life magnet swarf.

That feedstock — from wind turbines, EVs, industrial motors — is not yet available in the volumes needed. IDTechEx projects recycled REE supply will reach only 10% of global demand by 2036 even in an optimistic scenario. Companies are building 2,000–5,000 tpa plants before the feedstock base to fill them exists at Western scale.

♻️ Mixed REO vs. separated REO. Almost every Western recycler produces mixed or alloy output requiring further processing. Cyclic Materials' own Solvay supply agreement explicitly sends rMREO to La Rochelle, France "for further separation and purification" — confirming a second-stage step is required before individual REOs are produced.

HyProMag's HPMS process produces re-sinterable NdFeB alloy powder — valuable for short-loop re-manufacture but not individual separated oxides.

REEtec in Norway separates NdPr at commercial scale but has not confirmed Dy/Tb separation from recycled feedstock. Solvay La Rochelle separates downstream mixed concentrates — in France, not domestically — primarily producing NdPr.

IXR Belfast's MAIL platform is the only confirmed Western recycler simultaneously separating all four individual magnet REOs (Nd, Pr, Dy, Tb) — including the critical heavy rare earths Dy and Tb — from recycled Western magnets at >99.9% purity, with binding defence sales already delivered.

Every other pathway either stops at mixed output, produces NdPr only, or routes through a non-U.S. processor — none of which satisfies DFARS domestic supply chain requirements on their own.

♻️ IP claims vs. commercial verification. Several platforms with strong lab or pilot-scale results have attracted significant capital on the promise of commercial scale-up.

The chromatographic and ion-exchange platforms sound compelling in a pitch deck. At 200 tpa verified (Noblesville) vs. 16,000 tpa announced (Marion) — the gap between IP and industrial reality is where capital is disappearing.

discoveryalert.com.au/rare-earth-mag…

♻️ The feedstock dependency chain. Cyclic needs contracted OEM swarf (VAC Sumter SC — still under construction) → to produce MREO → which needs Solvay La Rochelle (France) or a domestic separator to produce individual REOs → which would feed Vulcan magnets → which needs DLA defence qualification → which needs DFARS compliance by January 2027.

Every single link in that chain is either unverified at scale, delayed past the deadline, or routes through a non-U.S. processor. One failure cascades through the entire Western recycling thesis — and the Solvay route never produces a domestically separated U.S. oxide regardless of when it scales.

6. Who's Actually Delivering Heavy REOs ✅

While the sector debates timelines and revises announcements, a very short list of organisations are actually shipping product:

✅ Lynas Rare Earths — 10,500 tpa NdPr. World's only commercial Dy and Tb separation outside China. Operating. Delivering. Profitable.

magneticsmag.com/lynas-separate…

✅ IXR Belfast (Ionic Technologies) — All four magnet REOs separated simultaneously at >99.9% purity at Demonstration Scale, Binding sales of (NdPr)₂O₃ and Dy₂O₃ to AML under the DLA defence contract.

Second binding sale executing. £12M UK Government grant secured for 400 tpa scale-up.

✅ MP Materials — NdPr oxide at Mountain Pass scaling. Light REE only, but genuinely operational.

Stockpiling SEG+ which needs further Separation

That's it. That's the list of Western operators with verified, separated, individual rare earth oxides in the hands of customers right now.

Everything else is a timeline. And timelines, in this sector, have a consistent recent track record of being revised — downward.

discoveryalert.com.au/domestic-hree-…

The Final Verdict ⏳

The CSIS said it plainly: 8 months may not be enough.

The GAO said it plainly: nobody knows where the rare earths in U.S. weapons actually come from.

The lobbyist said it plainly: "Unconscionable."

The recycler funding trail says it loudly: billions spent, timelines slipping, promises revised, and the two organisations actually separating defence-grade heavy rare earths outside China are the ones that built infrastructure before the headlines.

The numbers tell the story no press release can spin.

$700M committed → 10-tonne pilot + 200 tpa verified

16,000 tpa announced → 3,000 tpa pilot confirmed by POSCO in 2027

Two licensed U.S. separation facilities → neither at scale for NdFeB defence alloys

200,000+ defence suppliers → "little visibility" into rare earth provenance

8 months to DFARS deadline → zero Dy/Tb output from any newly funded U.S. entrant

The smoke is clearing. What's left isn't a supply chain. It's a series of revised timelines dressed as national security progress — while China remains embedded in the weapons systems of every NATO ally.

The companies that will matter when the waivers run out and the deadline is finally enforced are the ones already shipping product.

Not the ones still announcing it. ⏳👀

@ReElementTech @ucore @CyclicMaterials @IONICTECH_UK @MPMaterials @LynasRareEarths @SolvayGroup #VAC #HyProMag @VulcanElements

#RareEarths #CriticalMinerals #DFARS @realloys #WesternSupplyChain #NationalSecurity @RE_Exchanges @DiscoveryAlert #NdFeB #Dysprosium #Terbium #HeavyRareEarths #ReElement #VulcanElements #Ucore #CyclicMaterials #Lynas #IXR #MREO #IonicRareEarths #CSIS #GAO #NDAA #POSCO #DefenceSupplyChain #SovereignCapability #CriticalMineralsPolicy #MagnetRecycling #SupplyChainSecurity #OSC #FEOC #Pentagon #DoD 🇺🇸🧲⚡

English

Trump has signed a memo allowing federal agencies to hire 400 experts to boost the federal government's critical minerals investments.

Top pay for these experts will be set at $400,000 annually, "consistent with market comparability and national security urgency."

English

Wade retweetledi

Ionic Rare Earths, AML ink MoU for US permanent magnet supply dlvr.it/TSlXPP

English

Defense-driven demand powers surge in U.S. listings by mining firms reuters.com/business/defen…

English

We had a tenant move out of one of our rental properties and leave behind a mountain of trash.

As awful as that was, it got worse.

They also left behind two cats… to die.

One was locked in the garage with no food and no water.

The other was trapped in the house with no food and had water only because the toilet seat had been left up.

If we hadn’t gone back into that garage for another week or two, that cat would’ve been dead.

I genuinely can’t understand how someone could do that to an animal.

The crazy part?

These cats are unbelievably sweet.

We brought them out to the farm and we’re working to acclimate them into becoming farm cats now. Hopefully they’ll have a much better life ahead of them than the one they came from.

People can leave trash behind.

That can be cleaned up.

Leaving living animals behind to suffer is something entirely different.

English

It is this feldercarb that drives me looney. The US government has had a long standing policy that they generally will not pay someone to just dig around in the dirt, but they will pay for the metals, refined products and downstream materials.

That is why modern projects proposed today increasingly couple upstream processing with the mining operation itself. This shift started years ago and has only accelerated with the push for domestic critical mineral supply chains.

Even the article indirectly acknowledges this when it talks about Canada linking mining projects to battery and EV manufacturing, Australia incentivizing domestic mineral processing, and the US funding processing facilities and industrial partnerships. The direction is clearly toward vertically integrated supply chains rather than standalone extraction.

Projects are no longer being pitched as simply having a deposit in the ground. They are being pitched as integrated supply chains that move material from extraction into refining.

That is also why you rarely see standalone raw material projects anymore unless they already have a third party processing or refining agreement lined up. Investors and governments both want to know where the material is going, how it will be processed, and whether the final product can actually enter the domestic industrial supply chain.

While it is true that America as a whole kinda forgot how to mine, it is not ignoring nor is lacking in the expertise needed to create projects that are a all in one solution. The matter is more about capital and markets than expertise.

I do think however that adding CAM production at DLE sites is just inane, that has nothing to do directly to this post, but it did remind me of it, and that is trying to go a bit to far with the all in one solution.

FXHedge@Fxhedgers

THE MISSING LINK IN AMERICA’S CRITICAL MINERALS PUSH ISN’T MINING – IT’S PROCESSING EXPERTISE The United States is spending billions of dollars to secure access to critical minerals – minerals and metals that are essential to modern technology, from electric vehicles to smartphones and military systems. But amid the push to dig more, one question gets far too little attention: Who will actually process what comes out of the ground? Full article: msn.com/en-us/news/us/…

English

Wade retweetledi

@IONIC_RE is expanding its US presence with an agreement to supply @AMLInnovation with magnet rare earth oxides for US permanent magnets, supporting US defence needs. Read more: wcsecure.weblink.com.au/pdf/IXR/030932…

English

Wade retweetledi

Compact Caulk Gun

$22.09 each

4843N11

This is the weirdest caulking gun I've ever seen. I might have to get one to try out...

English

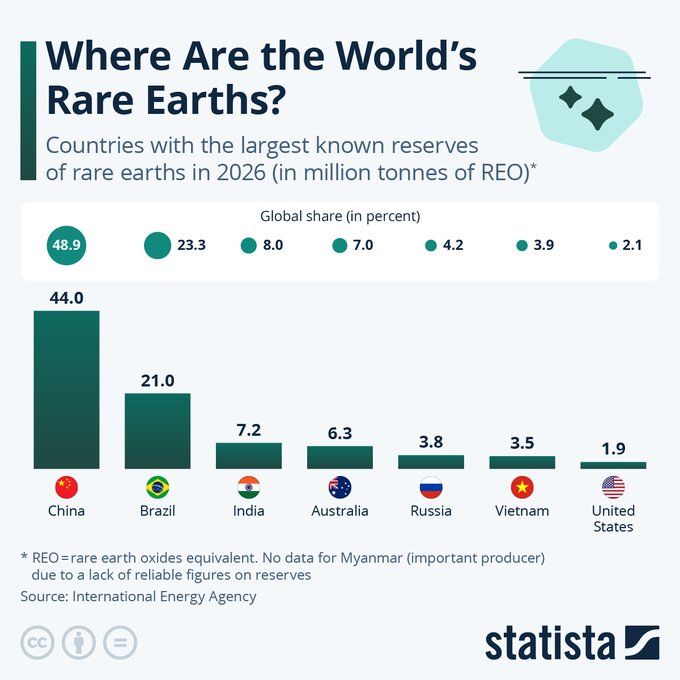

@paola_rojas @IEA Not many other concentrated regions with that much rare earth reserves. You’re hodgepodge looking elsewhere. Let’s hope the goal is to use these resources wisely.

English

Brazil and Australia have a stellar opportunity in rare earths.

Combined, they'd be nearly reaching 30MT REO, having a real shot at challenging China. What an opportunity.

📊 @IEA $LYC $SGQ $MP

English

Wade retweetledi