KaneCap

35.4K posts

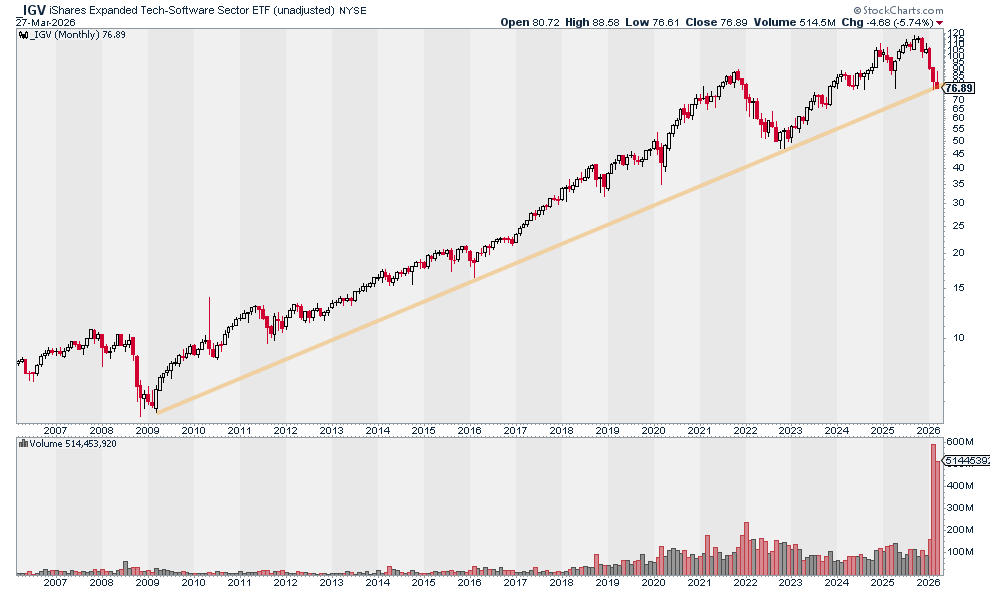

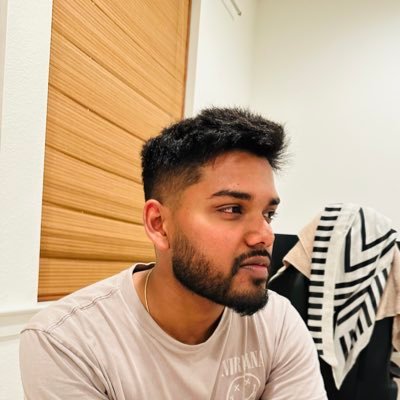

$AKAM might be one of the most mispriced stocks right now. Revenue went from $238M → $4.5B since 2005 - 20x growth Yet the stock is still around its IPO price $110. Two decades of execution. No re-rating. Market is missing something.

My goal with the TWIFT Index was to create a super simple index that helps track how public fintech companies are performing. It consists of just 15 stocks and is price-weighted. The TWIFT Index is doing its job: it captured the strong run fintech had in 2024, showed the stress early in 2025, and clearly shows how ugly 2026 is shaping up so far.

We're not the good guys...

I started looking at Western Union because I thought stablecoins would kill it. Then I realized WU is better positioned than almost anyone to leverage them. Brand, distribution, 200+ countries, $923M in EBITDA. The key risk was management. They had been skeptical of stablecoins. I placed the bet in November. Since then WU has not only outperformed Solana but the broader market: WU +2.14% / SPX -6.76% / Nasdaq -11.66% / SOL -56.15% WU is a $2.8B market cap business trading at 6x earnings with a 10% dividend yield. Remitly trades at 50x on a 2.3% operating margin. Wise at 23x. The discount exists because WU revenue is declining 3.8% while both are growing 25%+. I am not fighting that. But at 6x earnings you are paying for zero recovery, zero tech adoption, zero optionality. That is the margin of safety. I was at the @blockworksDAS this week. The WU CEO was on the same stage. Very different energy from the one I had been following. Clear on the stablecoin strategy, talking about flipping negative float into positive float. They have since announced USDPT, their own stablecoin on Solana. For a 175-year-old company to go from skepticism to launching on Solana in under a year is a meaningful shift. Of course, there is plenty of execution risk. The bear case was always that they would not act. They are acting - and that alone warrants a repricing. The math I ran back in November when I placed the bet was: lose ~20-30%, cushioned by $500M in net income and a 10% dividend. Re-rate to Wise multiples and it is 4 to 5x. I am not betting on convergence. I am betting the market prices zero probability of it, and I will get paid for getting a free option. WU is part of a broader thesis that led me to start @inversion_cap: acquiring businesses with distribution at attractive prices. There is a lot of embedded optionality in those businesses. Not all will act in time. Some will die. But the ones that do will meaningfully outperform, and those gains will more than outweigh the losses. You reduce that risk meaningfully when you control that business. The greatest beneficiaries of cost-reducing technology like AI and crypto are not the startups building it. They are the incumbents with distribution that adopt it. WU is one of many. Full piece on Substack: open.substack.com/pub/obviously/… @HadickM double or nothing? Market settles November 1, 2026. DISCL: Long WU. Long SOL. NFA.

Can’t stop, won’t stop

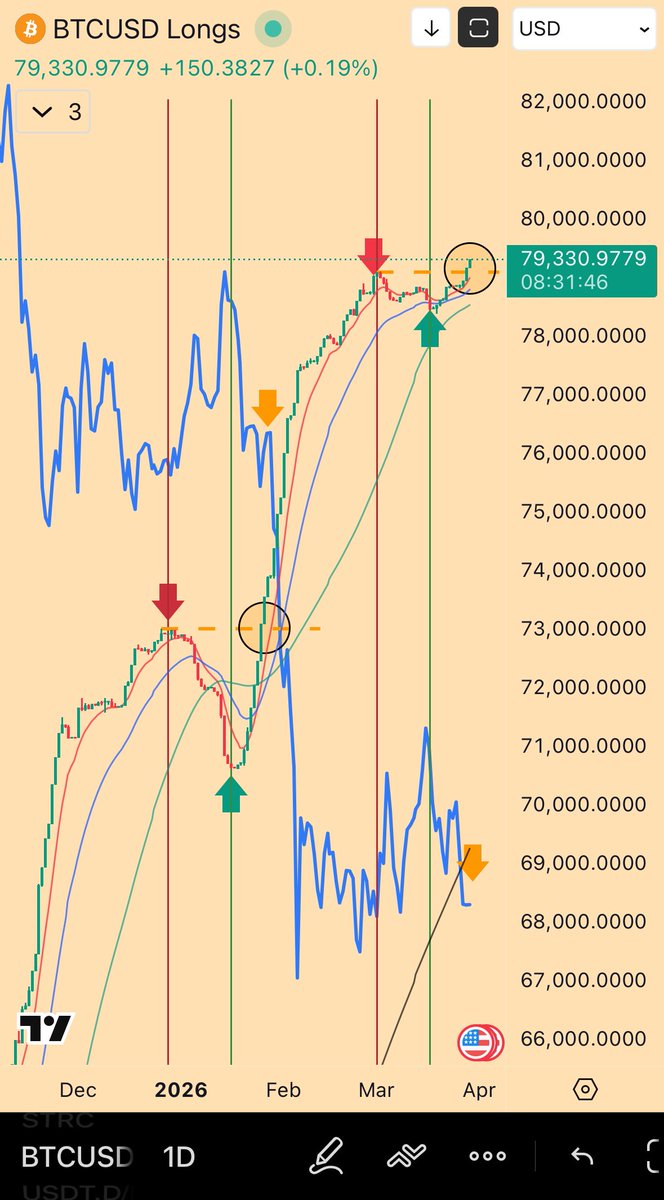

I shorted $SMH Let the bull market begin!

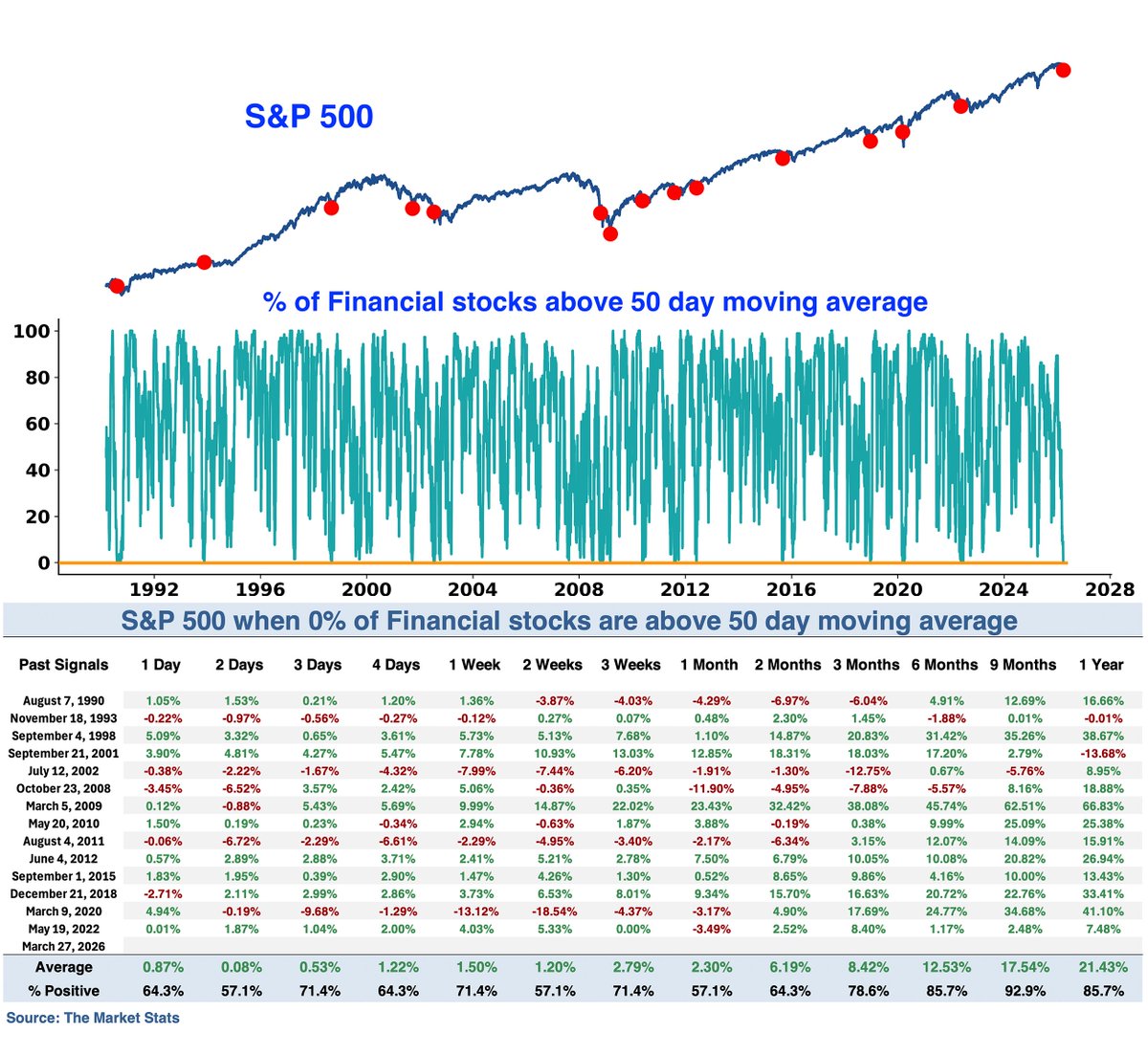

The S&P 500 is on track for its worst month since 2022.

the california propaganda will continue