ทวีตที่ปักหมุด

Tree

3.2K posts

Tree

@Tree75769

Investor | Early $IREN & Ripple | also hold $GOOGL

New York, USA เข้าร่วม Mart 2020

1K กำลังติดตาม584 ผู้ติดตาม

@theallinpod @mikehilliervb @nvidia @mikehilliervb I think we’re both in VB. As members in OF thought would be cool

To connect. My wife works at mythics so knew the name. Tried sending a dm but won’t let me unless you follow. Small world

English

🚨MAJOR INTERVIEW: Jensen Huang joins the Besties!

The @nvidia CEO joins to discuss:

-- Nvidia's future, roadmap to $1T revenue

-- Physical AI's $50T market

-- Rise of the agent, OpenClaw's inflection moment

-- Inference explosion, Groq deal

-- AI PR Crisis, Anthropic's comms mistakes

-- Token allocation for employees

++ much more!

(0:00) Jensen Huang joins the show!

(0:26) Acquiring Groq and the inference explosion

(8:53) Decision making at the world's most valuable company

(10:47) Physical AI's $50T market, OpenClaw's future, the new operating system for modern AI computing

(16:38) AI's PR crisis, refuting doomer narratives, Anthropic's comms mistakes

(20:48) Revenue capacity, token allocation for employees, Karpathy's autoresearch, agentic future

(30:50) Open source, global diffusion, Iran/Taiwan supply chain impact

(39:45) Self-driving platform, facing competition from active customers, responding to growth slowdown predictions

(47:32) Datacenters in space, AI healthcare, Robotics

(56:10) OpenAI/Anthropic revenue potential, how to build an AI moat

(59:04) Advice to young people on excelling in the AI era

English

Tree รีทวีตแล้ว

It’s always funny to see Wall Street completely fumble hyper-growth stocks.

The street is expecting $IREN to make ~$8.4b in revenues by FY 2030, with EBITDA margins of just ~68%.

Analysts are completely mispricing $IREN's 4.5 GW site-portfolio and multi-GW pipeline beyond that.

I went ahead and modelled out my own near-term projections for the coming 2 years, using the following assumptions:

Childress:

300 MW: MSFT Deal

450 MW: air-cooled (B300), fully ramped by Q3 2027

British Columbia:

160 MW: Mostly air-cooled, fully ramped by Q1 2027

Sweetwater 1:

600 MW: Vera Rubin (VR200) fully ramped by Q1 2028

Results:

👉 2027 = ~$8.3b (Rev) / ~$6.6b (EBITDA)

👉 2028 = ~$12.7b (Rev) / ~$10.3b (EBITDA)

One of Wall Street’s problems is that they only price what’s directly in front of them.

My 2027 revenue estimates are basically Wall Street’s 2030 projections. 🤦🏻♂️

And to be honest, my assumptions are actually very sensible. For the air-cooled deployments across Childress & BC, I used revenues BELOW management’s guidance.

For exact modelling inputs and FCF / net income projections up to 2030, refer to my new $IREN deep dive on Substack.

To be clear, I’m much more confident in my 2028 projection, since Sweetwater’s ramp could be more heavily skewed toward H2 2027 and H1 2028 instead of the simplified linear ramp approach I used.

However, the point remains: Wall Street is completely dropping the ball on this one.

What do you think will happen once $IREN announces its next hyperscaler deals at Childress and Sweetwater?

→ Massive re-rate incoming, as Wall Street scrambles to upgrade their idiotic projections.

English

Tree รีทวีตแล้ว

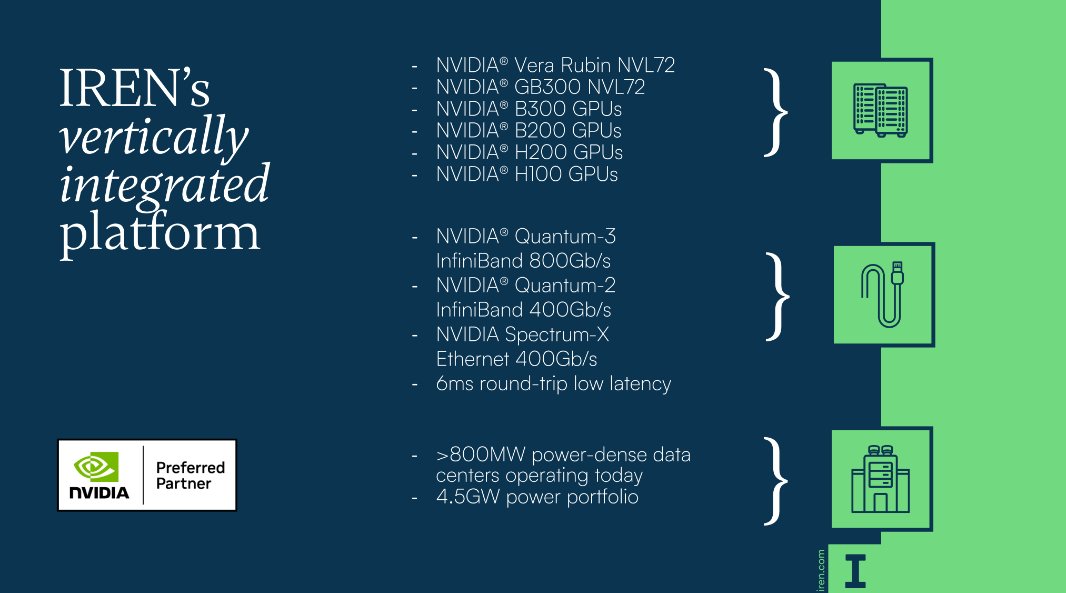

$IREN 's latest presentation at @NVIDIAGTC teases the Vera Rubin 👀

Is something cooking at Sweetwater?

English

Meant a pussy not dumb at the end. He doesn’t have the time for everyone to just come at him aimlessly so he’s blocking makes sense. You all are a bunch of flies buzzing around with no use. When someone finally provides a good debate I’ll have respect for the avg Nebius retail holder again.

English

That’s bc none of you say anything remotely useful! Literally not one of you can point by point say why he is wrong. I need evidence. He put the time and effort in and did so very respectfully yet you idiots see it as hate. Is constructive criticism. I love when people point out risks of iren and then we go through each point to understand the true underlying factors. You dumb mfers just chirp non stop. I don’t have any problem with Nebius I just personally can’t find a good reason to invest in it at these prices. I’m happy for you all you’re making money. I have done great as an iren holder too. Let’s just keep the dialogue to useful analysis and debate vs calling one of the few people who actually puts the work in dumb.

English

I am giving you the opportunity to convert me into a Nebius investor with a sizable amount to potentially add yet you are incapable of saying anything remotely coherent to disprove @Agrippa_Inv ‘s analysis. Knowing Nebius attracts people like you is exactly why I stay far away. Best of luck

English

Thank you Daniel for a great reply. As an Iren holder I genuinely wish you the best of luck. Totally agree with the tailwinds. I think at the end of the day people can be different types of investors and each of these companies just attracts people looking for different things. Both sides need to silence the aggravators throwing names out without providing any substantive dialogue. At the end of the day I’m here on x to learn about companies and try and find some edge with the sharing of knowledge. I, just like I’m sure you, have put a ton of research into IREN and my only conclusion is it has an extremely skewed risk/reward tradeoff to the reward side. Nebius has been fortunate enough to already achieve this reward and thus the risk/reward is skewed back towards risk (in my opinion only). If Iren hit $80 in a month I would feel the same way.

English

A few thoughts:

1. I don't know who @Agrippa_Inv is, but they strike me as someone who puts in the work, does the research, and forms a thesis grounded in conviction and a strong internal world model. This is the right way to invest, in my view, if you do it full-time and have the bandwidth. More people should share their thinking like this. X is better for it.

2. Unsurprisingly, as a $NBIS investor, I disagree with several of the points made.

3. That said, I genuinely enjoyed reading this post. It was well articulated and I appreciated hearing a thoughtful opposing perspective.

4. What I find deeply frustrating, and frankly embarrassing for both investor communities, is that every reasonable take like this one attracts only two types of responses: "yeaaaaah you're sooooo smart" from those who own the same stock, and "you're an idiot, have fun staying poor" from those who don't. The problem was never disagreement. Disagreement is healthy. The problem is the complete absence of decency and taste in how people engage. And that is exactly why arguing in the comments with those people is pointless. I will block anyone in my replies who resorts to insults simply because they disagree.

Now, regarding the substance: no, I won't be writing a 10 page long, combative rebuttal. I don't have the time right now. For those who need constant reassurance, I will share my simplistic view though:

My view is straightforward. I believe inference demand will be staggering. I believe we'll be dramatically short AI compute sooner than most expect. Many companies are positioned to benefit, but as a stock picker, I want the one best positioned to capture that value.

I don't believe owning physical infrastructure or having grid-secured energy contracts is the key differentiator long term, though I absolutely recognize these are valuable, strategic assets that can accelerate timelines.

What I do believe is this: Nebius is building an ecosystem with multiple layers of value-adding services. They get mischaracterized as only a software company that secretly does Bare Metal deals. No, they are a full stack company that truly does it all. Infrastructure, software and much more. In my view, they are the only potential next hyperscaler with true full-stack expertise, world-class across every dimension. And I have very high confidence in their management to deliver, based on past execution against promises, skillset, and track record. I don't have that same level of trust in other companies.

Can $IREN outperform? Absolutely. I'd characterize it as higher risk, higher reward.

I could write 40 pages on this, but I don't see the point. I don't have a Substack to sell right now, and I know most people would just read an AI summary of it anyway.

At some point in the future, these companies will both trade based on execution. Right now the reality is they don't. Currently they trade together like twins. Love it or hate it, that's the reality today.

𝐀𝐠𝐫𝐢𝐩𝐩𝐚 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭𝐬@Agrippa_Inv

Why I’m Not Invested in $NBIS First of all, let me make one thing clear: contrary to what you might think, I’m not an $NBIS bear. But then again, I’m not invested either… and for good reason. Nebius positions itself as a holistic cloud platform with superior software technology that caters to AI-native start-ups and enterprise clients. That in and of itself isn’t a problem, but it means they're directly competing against the largest hyperscalers in the world, who are also targeting that exact cohort with their own set of software solutions (Google Cloud, Microsoft, etc.). Nonetheless, if $NBIS can successfully differentiate itself with its core offerings, it could gain some pricing power, which is the company’s best shot at one day becoming profitable. The problem is, $NBIS is VERY far away from that… Looking at the last quarterly filing, the company’s gross expenses + depreciation equaled ~110% of its revenues. In other words, these two cost categories exceeded the value of the underlying revenues ($249.2m vs. revenue of $227.7m). To be fair, last quarter Nebius still used a 4 year depreciation schedule on GPUs, which is rather short and overstates depreciation. Adjusting for a 5 year depreciation schedule (industry standard) leads us to $144.6m of depreciation. Then, adding gross expenses of $68.5m on top gets you to $213.1m, which equals 93.5% of revenues. And keep in mind, this figure does NOT include the hundreds of millions in costs spent on SG&A, R&D, and financing (interest). So what’s my point with this? The problem is, these are STRUCTURAL costs, the kind that scale with revenue, meaning you can’t easily grow out of them through sheer scale. My point is that $NBIS' pricing power is nowhere to be seen, at least not relative to its costs. Now, most $NBIS investors would probably argue that we are still "early" and that pricing power will show up eventually. My problem with that argument is that the company seems to be allocating a very large chunk of its pipeline towards servicing hyperscalers through bare metal offerings, the kind of “bulk” service that does NOT command significant pricing power. That means, fundamentally speaking, $NBIS is likely very far away from actually becoming profitable. And while right now everyone is focused on headline figures like ARR, the market’s patience will run out eventually... it ALWAYS does for every company. One day, the market will demand to see real profits flow down to the bottom line, and I’m not sure if $NBIS is structurally positioned to deliver on that any time soon. To make matters worse, investors can’t even model out the economics of these large hyperscaler deals, because management provides absolutely 0 information on anything except headline figures. We don’t even know the CapEx associated with these deals, or at the very least, the number of GPUs they have to purchase to fulfill their end of the bargain. Contrast that with a company like $IREN, which gives you all the necessary information to build an entire P&L and cash flow model over the full course of the contract length, which is exactly what I’ve done extensively for our subscribers on Substack. I have a VERY good idea of how much actual post-tax net income $IREN is making in every year of their hyperscaler contract. There are other reasons that further point in the same direction, but I won’t get into them right now. If they fix their cost structure one day, I’m happy to reconsider my stance. But as of today, their “black box” approach to publishing details on their largest deals makes them uninvestable for me.

English

lol you sound like a complete idiot 😂 "the language of business" just because you can spell comparative profitability analysis doesn’t mean you know shit about business. Your ai slop replies are more than indicative that you know nothing and your reliance on announcements over fundamental analysis of nebius financials is more than enough proof too. You have yet to pull any reliable info to back what you are saying. Just vague nothings about economic life> accounting life. Agrippa (and myself) agree that Nebius had been using too short of a depreciation schedule on the GPUs and he still provides the math that DOESNT WORK. Sure you’re software stack sounds cool, but if it was as important as you say the why are they making bare metal deals with hypers who have their own software stack. The answer is that none of the hypers give a shit about your software and it’s not a moat.

English

@Tree75769 @Agrippa_Inv I understand that not all can speak the language of business so you won’t know. Only those who studied and actually did it can like me. Once $IREN actually has AI revenues and related cost, we’ll compare it to $NBIS if you want an apple to Apple comparative profitability analysis

English

Why I’m Not Invested in $NBIS

First of all, let me make one thing clear: contrary to what you might think, I’m not an $NBIS bear. But then again, I’m not invested either… and for good reason.

Nebius positions itself as a holistic cloud platform with superior software technology that caters to AI-native start-ups and enterprise clients.

That in and of itself isn’t a problem, but it means they're directly competing against the largest hyperscalers in the world, who are also targeting that exact cohort with their own set of software solutions (Google Cloud, Microsoft, etc.).

Nonetheless, if $NBIS can successfully differentiate itself with its core offerings, it could gain some pricing power, which is the company’s best shot at one day becoming profitable.

The problem is, $NBIS is VERY far away from that…

Looking at the last quarterly filing, the company’s gross expenses + depreciation equaled ~110% of its revenues. In other words, these two cost categories exceeded the value of the underlying revenues ($249.2m vs. revenue of $227.7m).

To be fair, last quarter Nebius still used a 4 year depreciation schedule on GPUs, which is rather short and overstates depreciation.

Adjusting for a 5 year depreciation schedule (industry standard) leads us to $144.6m of depreciation. Then, adding gross expenses of $68.5m on top gets you to $213.1m, which equals 93.5% of revenues.

And keep in mind, this figure does NOT include the hundreds of millions in costs spent on SG&A, R&D, and financing (interest).

So what’s my point with this?

The problem is, these are STRUCTURAL costs, the kind that scale with revenue, meaning you can’t easily grow out of them through sheer scale.

My point is that $NBIS' pricing power is nowhere to be seen, at least not relative to its costs.

Now, most $NBIS investors would probably argue that we are still "early" and that pricing power will show up eventually.

My problem with that argument is that the company seems to be allocating a very large chunk of its pipeline towards servicing hyperscalers through bare metal offerings, the kind of “bulk” service that does NOT command significant pricing power.

That means, fundamentally speaking, $NBIS is likely very far away from actually becoming profitable.

And while right now everyone is focused on headline figures like ARR, the market’s patience will run out eventually... it ALWAYS does for every company.

One day, the market will demand to see real profits flow down to the bottom line, and I’m not sure if $NBIS is structurally positioned to deliver on that any time soon.

To make matters worse, investors can’t even model out the economics of these large hyperscaler deals, because management provides absolutely 0 information on anything except headline figures.

We don’t even know the CapEx associated with these deals, or at the very least, the number of GPUs they have to purchase to fulfill their end of the bargain.

Contrast that with a company like $IREN, which gives you all the necessary information to build an entire P&L and cash flow model over the full course of the contract length, which is exactly what I’ve done extensively for our subscribers on Substack.

I have a VERY good idea of how much actual post-tax net income $IREN is making in every year of their hyperscaler contract.

There are other reasons that further point in the same direction, but I won’t get into them right now.

If they fix their cost structure one day, I’m happy to reconsider my stance.

But as of today, their “black box” approach to publishing details on their largest deals makes them uninvestable for me.

English

@jtaquino002 @Agrippa_Inv After reading this I realize you are not worth my time lol. Best of luck

English

@Tree75769 @Agrippa_Inv Post suggests the author doesn’t have a good blend of accounting and finance knowledge. The claim that cost of revenue items are purely “structural” ignores that depreciation and many infrastructure costs have strong operating leverage. Economic life > accounting life acctg 101

English

Pod will be a banger. All Jensen all the time - from GTC!

Up soon…

English

I stand by what I said:

Nebius will be one of the hottest cybersecurity investments.

I'm not surprised to see the Nebius x CrowdStrike partnership.

I expect MUCH more of that going forward.

This will soon happen:

1. Investors will be desperate to find the hottest AI cybersecurity play, as the world realizes AI is a cybersecurity nightmare (everyone already knows, we just need some big scandals to happen first as a catalyst).

2. They will learn it's actually Nebius.

Why?

AI multiplies how much data companies generate, buy, store, etc.

AI also multiplies the attack vectors.

Cloud providers "the companies who help you manage your data" are in a very strong and natural position to offer solutions.

Obviously you want the company that helps you store and manage your data to be insanely competent in this area.

Israel DOMINATES in cybersecurity.

Nebius has a massive talent base in Israel (and beyond of course).

It's not just about their talent in Israel, but I have a feeling they will play a crucial role in this area.

They got all the ingredients. Now let them cook.

$NBIS x $CRWD

Daniel Koss@daniel_koss

Probably ~1-2 years too early, but know this: $NBIS will also be the hottest play in cybersecurity.

English

@JustusFult99485 @Agrippa_Inv I mean just refute one of his points with your “IQ points” then. We would love to be proven wrong. The problem is no $NBIS retail holder and accurately defend anything. Go play with your cat I’m sure it understands your iq points

English

@Agrippa_Inv I’m out performing you with these IQ points little buddy.

English

Tree รีทวีตแล้ว

Live in two hours!

Watch $IREN CCO @kentpdraper on stage at @NVIDIAGTC.

Topic: Vertically Integrated AI Cloud: Accelerating AI Development

When: Today | 4:00pm PDT

Where: Hilton Winchester (L1)

Add the session to your schedule here:

nvidia.com/gtc/session-ca…

English

$IREN Woah - a whole lot of people are about to to learn all about $IREN if they didn’t already. Pretty huge whether or not you love/hate @theallinpod personally I couldn’t be happier this happened.

IREN@IREN_Ltd

Attending @NVIDIAGTC? Don't miss @theallinpod @Jason's interview with $IREN Co-Founder and Co-CEO @danroberts0101. 🗓️When: Today, 1:15pm PDT 📍Where: Expo Hall (between the @nvidia Booth and Automotive area)

English

CRYPTO EXCHANGE KRAKEN FREEZES MULTIBILLION-DOLLAR IPO PLAN - COINDESK

English