Asher Siddiqui รีทวีตแล้ว

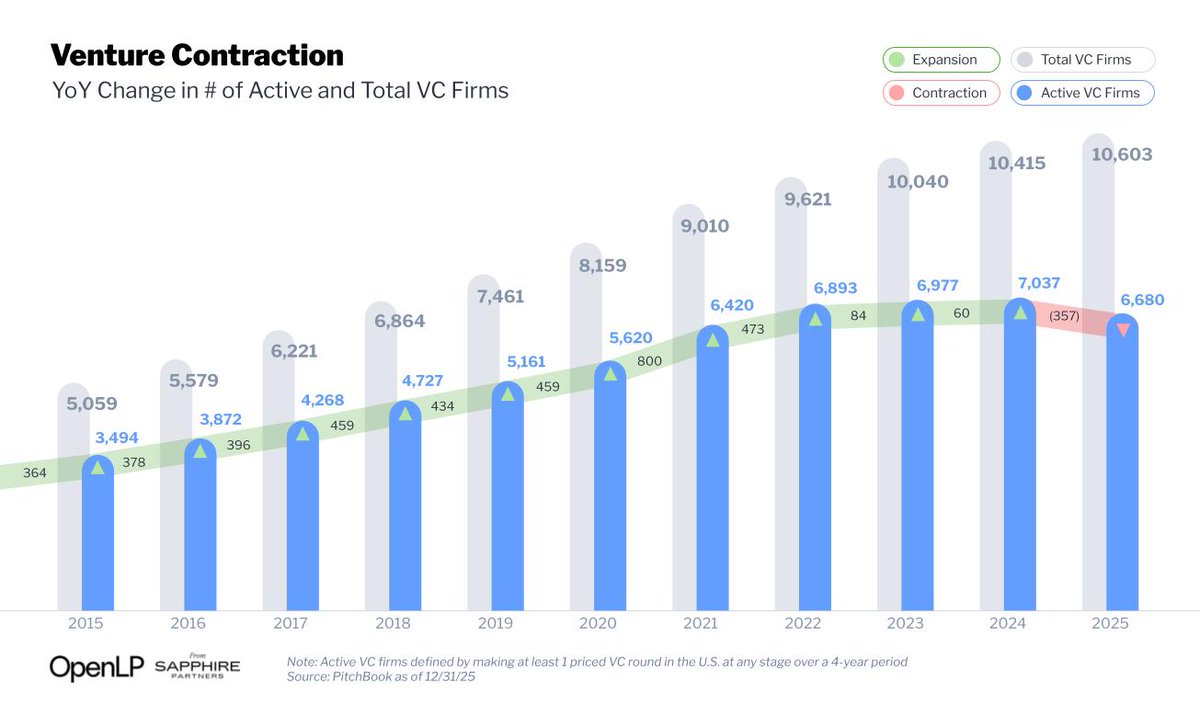

🧵1/ For decades, venture has expanded practically by default: more funds, more managers, more capital.

After 20+ years, we are now facing the first meaningful industry-wide contraction since the dot-com collapse, with the smallest active investor base in more than 25 years.

English